FBAR: Requirements, Deadlines, and How to File

- What Is the FBAR (Foreign Bank Account Report)?

- Who Needs to File the FBAR?

- How to File the FBAR

- FBAR Deadline for Expats

- What Are the FBAR Penalties for Not Filing?

- What Should I Do If I Haven't Filed an FBAR?

- Common Misconceptions While Filing for FBAR

- Other Foreign Financial Reporting Requirements for Expats

- Filing FBAR Doesn't Have to be Complicated

Governed by the IRS, the Foreign Bank Account Report (FBAR) necessitates the reporting of foreign financial accounts when the aggregate value exceeds $10,000 at any point during the calendar year. The importance of this regulatory requirement is paramount, as failure to comply can lead to substantial penalties and increased IRS scrutiny. Understanding and complying with the Foreign Bank Account Report (FBAR) is a critical but often overlooked aspect of tax responsibilities for Americans living abroad.

Key Takeaways

- FBAR or FinCen 114 must be filed if you had more than $10,000 at any time during the year in all of your combined foreign accounts, even if your total balance was less than $10,000 in each of the accounts individually.

- If you and your spouse only hold Joint Accounts, you can file FinCen 114a to cover both individuals; otherwise, each spouse must file an FBAR.

- The FBAR is currently on an automatic extension to October 15th every year

- If you have not been filing your FBAR, the best way to get caught up is via the Streamlined Filing Procedure.

What Is the FBAR (Foreign Bank Account Report)?

The Foreign Bank Account Report (FBAR) is an annual report that all US citizens, residents, and certain other persons must file with the United States Treasury Department in which the person has a financial interest in, or signature authority over, a financial account in a foreign country with an aggregate value of more than $10,000 at any time during the calendar year.

Keep in mind that those filing FBAR aren’t taxed on the balance of the accounts or anything of the sort. This is a reporting requirement, so the IRS knows what money lies overseas.

If you’re an expat with foreign financial accounts, ignoring your requirements can result in penalties starting at about $12,500 and legal consequences. The United States government has stepped up efforts to investigate and prosecute expats who fail to report their foreign-held financial assets. This means that the risk of non-compliance with FBAR regulation is more significant than ever.

Thankfully, there are plenty of easy ways to comply with your requirements. This guide will explain everything you need to know about the FBAR, including:

- Who needs to file the FBAR

- How to file your foreign bank account report

- FBAR deadlines and when to file

- Related topics like the Foreign Account Tax Compliance Act (FATCA)

Dreading the last minute scramble pulling together your tax documents? Despair no more! This simple checklist lists the documents you need to have on hand when preparing to file.

Who Needs to File the FBAR?

Any US person (that is, any person considered a US tax resident) with a foreign account balance of $10,000 or more at any point during the tax year will need to file the FBAR. This requirement is triggered even if the balance hits $10,000 for just one day (or one minute)!

The FBAR filing threshold is also an aggregate amount—meaning if you have multiple accounts, the total balance of all of your accounts is what would trigger a filing requirement. So, if you think that keeping $4,000 in one account and $7,000 in another will enable you to avoid filing, this isn’t the case.

Report Joint Accounts and All Others You Can Access

FBAR filing requirements apply to all foreign financial accounts in which you have a financial interest or signature authority.

- Financial interest is determined based on who the real owner of the funds is. This rule is meant to require the reporting of funds that someone owns but holds in an account that is not in their name but under the name of, for example, their business partner, friend, or attorney.

- Signature authority means that you have some level of control over the disposition of assets through direct communication with the institution. One common example of this is when an elderly parent adds their child to their bank account to allow their child to help them with their finances.

If you were a signatory on one of your employer’s bank accounts, this account should be reported on your FBAR. You should also report joint accounts with your spouse.

FBAR Applies to All US Persons, Not Just Citizens

The IRS says that the FBAR is required for “United States persons” who meet the reporting threshold. The term “US persons” refers to:

- Citizens

- Resident aliens

- Trusts

- Estates

- US based companies

There are some exceptions to the foreign bank account reporting requirements. For example, US citizens living abroad who own certain types of foreign financial accounts including those maintained by a government or international financial institution are not required to report them on an FBAR. Consult with an expert CPA to know if you qualify.

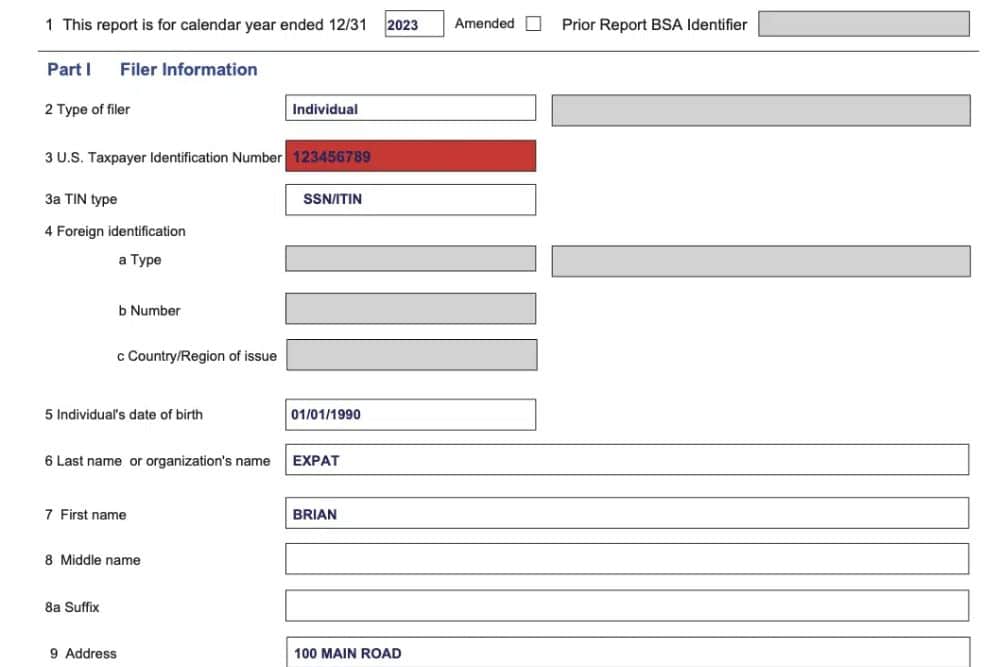

How to File the FBAR

The FBAR is a separate filing from your federal tax return. It must be submitted separately to the Financial Crimes Enforcement Network (FinCEN), which is a different branch of the Department of the Treasury. It is not filed with the IRS. To file the FBAR, you’ll use FinCEN 114 and submit it electronically through the BSA e-filing site.

The process is straightforward and requires you to gather all pertinent account information and enter it into the online system. You can have a third party prepare it for you (i.e., a certified tax preparer), All you have to do is sign or e-sign FinCEN 114a to give the party authority.

Information to Include on the FBAR

Most filers will just be reporting their foreign bank account balances. However, you must also report any of the following that apply:

- Foreign investment accounts (the account itself must be reported, but the contents of the account do not need to be reported separately)

- Many different types of retirement and pension accounts

- Financial account held at a foreign branch of a US bank

- Foreign mutual funds

- Foreign-issued life insurance or annuity contract with a cash surrender value

How to Report Joint Accounts on the FBAR

If you and your partner only hold joint accounts, have your spouse sign FinCEN Form 114a to allow you to file the FBAR on their behalf.

If your spouse has other accounts that you are not on (i.e., individual foreign financial accounts), they must file their FBAR separately. When filing separately, you must both include your joint accounts on each of your individual forms.

Good Records Are the Key to Simplified FBAR Filing

Recordkeeping is essential to keeping up with how you file the FBAR. Submitted forms must contain the following information:

- The maximum value (converted to USD using a specific end-of-year exchange rate) of each account during the reporting period

- The name on the account(s)

- The number/other designation of the account

- The type of account

- The name and address of the institution or other person with whom the account is maintained

Many expats also find that they have to file one year and not the next. For this reason, it is essential to make good record-keeping a habit.

FBAR Deadline for Expats

The FBAR must be filed by April 15, 2024. If you miss this deadline, there is an automatic extension to October 17, 2024 (as the 15th falls on a Saturday)

When you live in the US, tax day is simple: April 15th! When you move abroad, it’s not so straightforward! Learn about all the expat deadlines and extensions you need to know to file.

What Are the FBAR Penalties for Not Filing?

Severity of Penalties for Failing to File FBAR: Failing to file the required Foreign Bank and Financial Accounts Report (FBAR) can result in severe penalties. The nature of these penalties depends on whether the failure to file was willful or non-willful.

Non-Willful Violations:

- For non-willful violations (where there is no intent to evade tax laws), the penalties start at approximately $10,000 per violation.

- The penalty amount may vary based on the account balances at the time of the violation.

- Notably, in a Supreme Court case known as the Bittner case, the IRS’s maximum penalty for non-willful violations was capped at $50,000, a significant reduction from the original assessment of $2.72 million in this case.

Willful Violations:

- Willful failure to file an FBAR, indicating a deliberate attempt to avoid tax obligations, carries more severe penalties.

- Penalties can exceed $100,000 or amount to 50% of the account balance at the time of the violation.

- In addition to financial penalties, willful violations may lead to criminal charges, including potential prison sentences.

Cumulative Impact of Penalties:

- If you are multiple years behind in FBAR filing, the penalties can accumulate rapidly, posing a significant financial risk.

What Should I Do If I Haven’t Filed an FBAR?

First off, don’t panic! Millions of Americans have FBAR forms that are past due, and the IRS has created two amnesty programs to help you get caught up:

- The Streamlined Compliance Procedures

- The Delinquent FBAR Submission Procedures

Both tax amnesty programs let expats comply with US tax law without paying any penalties. Let’s take a closer look at each.

If you’re behind on your US taxes, you may qualify for a special compliance program to get back on track without penalties. Download our Streamlined Filing Eligibility guide to understand if you qualify.

Streamlined Compliance Procedures

The Streamlined Compliance Procedures are meant for US expats who have failed to file an annual income tax return as well as any required FBARs. To use the Streamlined Compliance Procedures, all you have to do is:

- Self-certify that your failure to file was accidental, not willful

- File your last three delinquent income tax returns and pay any taxes you owed on those returns

- File FBARs for the previous six years

Delinquent FBAR Submission Procedures

If you’re only behind on filing FBARs while being up to date on your annual tax returns, you can use the Delinquent FBAR Submission Procedures instead. To do this, you must simply:

- Self-certify that your failure to file was not willful

- File all delinquent FBARs

In most cases, this should be sufficient to bring you into compliance with IRS standards as long as you have reported all income earned from these accounts.

These tax amnesty options are generally only available if you initiate the process yourself. If the IRS discovers your delinquency and contacts you first, you may be ineligible for these programs and thus subject to penalties.

Common Misconceptions While Filing for FBAR

- It’s a common misconception that an overseas account with less than $10,000 doesn’t need to be reported. However, if the combined highest value of all foreign accounts on any day in the tax year exceeds $10,000, then all accounts must be reported on the FBAR.

- Another mistake is assuming that a nominee doesn’t need to report an account on the FBAR. Even if the account belongs to another person, the nominee must still file the FBAR if it meets the dollar threshold.

- It’s also important to understand what needs to be disclosed on the FBAR. Foreign mutual funds and foreign life insurance/annuity policies with a cash surrender value must be reported.

- Lastly, filing an extension for your US income tax return does not extend the FBAR filing deadline. The FBAR is a separate requirement with a different due date, so it’s crucial to file it on time to avoid penalties.

Other Foreign Financial Reporting Requirements for Expats

Years ago, some expats got comfortable evading the FBAR because it was hard for the IRS to track down violators. The FBAR is required for US citizens because foreign banks don’t have the exact reporting requirements as institutions in the US, making it harder for the US to investigate potential non-compliance cases.

The Foreign Account Tax Compliance Act (FATCA) changed all of that. FATCA requires individuals or businesses with foreign accounts meeting the reporting threshold of $50,000 to file Form 8938 with the IRS.

FATCA is different from FBAR on multiple levels:

- FATCA is filed with the IRS as part of your tax return

- FATCA reporting thresholds are higher

- Most importantly, FATCA requires foreign financial institutions to report directly to the IRS on financial accounts held by US taxpayers.

This last point is critical. Because foreign financial institutions report directly to the IRS, the government can easily find out about your unreported foreign assets. This dramatically increases the chances that the IRS will catch you if you fail to file an FBAR when required.

While foreign financial accounts containing stock and securities must be reported, the contents within them do not have to be reported separately.

Filing FBAR Doesn’t Have to be Complicated

We hope this guide has helped you understand what the FBAR means for Americans living abroad. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

If you’re ready to be matched with a Greenback accountant, click the get started button below.

Featured In