5 Things You Should Know About IRS Form 8865

If you own at least 10% of a controlled foreign partnership, you may be required to file Form 8865. Form 8865 is used to report the activities of a controlled foreign partnership and must be filed with your individual income tax return (Form 1040). Filing Form 8865 is imperative as it ensures compliance with IRS regulations on reporting foreign partnerships, thereby helping to avoid hefty penalties and legal repercussions associated with non-disclosure of international financial interests.

But what is Form 8865—and how does it work? We know there are a lot of expat tax forms, so here are the answers to all your questions.

Key Takeaways

- Any US person with at least 10% interest in a controlled foreign partnership must file Form 8865

- Form 8865 is due at the same time as your individual income tax return- In most cases April 15th of every year.

- Failing to file Form 8865 on time can have unfavorable consequences like heavy fines by the IRS

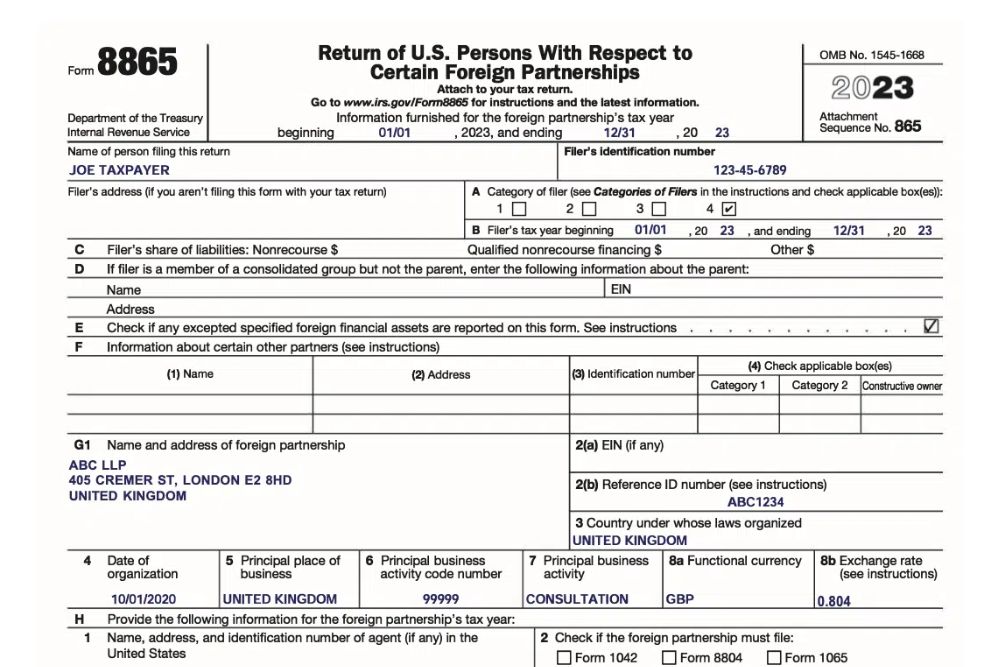

What Is Form 8865?

Form 8865, or the Return of US Persons With Respect to Certain Foreign Partnerships, is a tax form used by individuals and entities to report ownership of, transactions with, and certain other activities related to controlled foreign partnerships. It is known as an informational return, meaning that you are required to report additional information to the IRS, but the form itself will not result in any additional tax or fees due to the IRS.

Form 8865 lets US persons in a controlled foreign partnership report their tax information to the IRS as required by the following IRC sections:

- 6038 – Information Reporting With Respect to Certain Foreign Corporations and Partnerships

- 6038B – Notice of Certain Transfers to Foreign Persons

- 6046A – Returns as to Interests in Foreign Partnerships

This information will be similar to IRS forms 1065 and 5471.

Who Needs to File Form 8865?

Any US individual holding a minimum of 10% interest in a foreign partnership may be required to file Form 8865, particularly when this partnership qualifies as a “controlled foreign partnership.” This designation comes into play when more than 50% of the partnership’s ownership is held by one or more US persons.

To illustrate, consider a scenario where a US expatriate owns a 55% stake in a Costa Rican partnership. Given the majority ownership, this partnership falls under the “controlled foreign partnership” category, necessitating the filing of Form 8865.

On a different note, assume three US expatriates collectively run a business in Portugal, each owning a 20% stake. Together, they hold a 60% ownership in the business, thereby again categorizing it as a “controlled foreign partnership” and making Form 8865 filing a requirement.

This mandate isn’t exclusive to partnerships alone; it extends to other foreign business entities opting for partnership taxation, like a multi-member LLC. By adhering to this filing requirement, US individuals ensure compliance with the IRS, maintaining transparency in their international financial engagements.

How Do You File Form 8865?

There are several filing categories that US partners may fall under, and your category will determine what sections of IRS Form 8865 you’re required to complete.

Everyone will have to fill out their identifying information at the start of Form 8865. But beyond this, there are a number of “schedules” that you may or may not have to complete depending on your category. Some of these schedules are included within Form 8865 itself, while others are separate and will need to be attached to your finished form.

Below are the categories for US persons required to file Form 8865:

Category 1

If a single US person owns more than 50% of a controlled foreign partnership, they are a Category 1 filer.

Generally, Category 1 filers must complete these schedules:

- Schedule A: Constructive Ownership of Partnership Interest

- Schedule A-1: Certain Partners of Foreign Partnership

- Schedule A-3: Affiliation Schedule

- Schedule B: Income Statement—Trade or Business Income

- Schedule G: Statement of Application of the Gain Deferral Method Under Section 721

- Schedule H: Acceleration Events and Exceptions Reporting Relating to Gain Deferral Method Under Section 721

- Schedule K: Partners’ Distributive Share Items

- Schedule L: Balance Sheets per Books

- Schedule M: Balance Sheets for Interest Allocation

- Schedule M-1: Reconciliation of Income (Loss) per Books With Income (Loss) per Return

- Schedule M-2: Analysis of Partners’ Capital Accounts

- Schedule N: Transactions Between Controlled Foreign Partnership and Partners or Other Related Entities

- Schedule D: (Form 1065) Capital Gains and Losses

- Schedule K-1: Partner’s Share of Income, Deductions, Credits, etc.

- Schedule K-2: Partnership’s operations, such as foreign taxes paid, income from foreign sources, and other deductions or credits related to foreign activities.

- Schedule K-3: extension of Schedule K-1; reports the share of the items reported on Schedule K-2.

Category 2

If a US person owns at least 10% of a controlled foreign partnership, they are a Category 2 filer. (However, if any partner qualifies as a Category 1 filer during the tax year in question, no one will be considered a Category 2 filer.)

Generally, Category 2 filers must complete these schedules:

- Schedule A: Constructive Ownership of Partnership Interest

- Schedule A-3: Affiliation Schedule

- Schedule N: Transactions Between Controlled Foreign Partnership and Partners or Other Related Entities

- Schedule K-1: Partner’s Share of Income, Deductions, Credits, etc.

- Schedule K-2: Partnership’s operations, such as foreign taxes paid, income from foreign sources, and other deductions or credits related to foreign activities.

- Schedule K-3: extension of Schedule K-1; reports the share of the items reported on Schedule K-2.

Category 3

If a US person contributes at least $100,000 to a controlled foreign partnership—or if they own at least 10% of the partnership after their contribution—they are a Category 3 filer.

Generally, Category 3 filers must complete these schedules:

- Schedule A: Constructive Ownership of Partnership Interest

- Schedule A-1: Certain Partners of Foreign Partnership

- Schedule A-3: Affiliation Schedule

- Schedule G: Statement of Application of the Gain Deferral Method Under Section 721

- Schedule H: Acceleration Events and Exceptions Reporting Relating to Gain Deferral Method Under Section 721

- Schedule O: Transfer of Property to a Foreign Partnership

Category 4 Filer

If a US person had a reportable transaction under IRC Section 6046A during a calendar year, they are a Category 4 filer. These reportable transactions may be acquisitions, dispositions, or changes in proportional interest.

Acquisition

An acquisition means that you owned less than 10% of the partnership previously, then raised your interest to 10% or higher through a purchase or inheritance. For example, if you had 7% interest in a controlled foreign partnership, then purchased 4% more interest, leaving you with 11% interest, that would qualify as an acquisition.

Disposition

A disposition means that you owned at least 10% of the partnership, then disposed of some portion of your interest, bringing your total ownership below 10%. For example, if you owned 13% of a controlled foreign partnership, then sold 5%, leaving you with 8% total, that would qualify as a disposition.

Change in Proportional Interest

A change in proportional interest means that compared to your last reported interest in the partnership, your ownership went up or down by at least 10% of the total interest. For example, if you previously owned 25% of the controlled foreign partnership, then sold 14%, leaving you with 11% ownership, that would qualify as a change in proportional interest. Alternatively, if you purchased 14% interest, bringing you to 39% ownership, that would also qualify.

In any of these cases, you would be considered a Category 4 filer.

Generally, Category 4 filers must complete these schedules:

- Schedule A: Constructive Ownership of Partnership Interest

- Schedule A-3: Affiliation Schedule

- Schedule G: Statement of Application of the Gain Deferral Method Under Section 721

- Schedule H: Acceleration Events and Exceptions Reporting Relating to Gain Deferral Method Under Section 721

- Schedule P: Acquisitions, Dispositions, and Changes of Interests in a Foreign Partnership

This is only a general overview of the categories and requirements involved in filing Form 8865. For more information, please see the Form 8865 instructions provided by the IRS.

When Is Form 8865 Due?

Form 8865 is due at the same time as your individual income tax return. For most taxpayers, this will be April 15th of every year. However, if your tax filing deadline is extended for any reason, the deadline for Form 8865 will also be extended.

Once you’ve prepared your Form 8865, attach it to your individual income tax return and any necessary schedules. (Or, if applicable, attach it to your partnership or exempt organization return.)

If you aren’t required to file an individual tax return (or partnership or exempt organization return), you’ll still have to file Form 8865 by the due date for that return.

What Happens If You Don’t File Form 8865 on Time?

Failing to file Form 8865 on time can have dire consequences. The severity will depend on which filing category you’re in.

Categories 1 and 2

If you’re a Category 1 or 2 filer, the IRS may impose a $10,000 fine for every tax year you fail to file Form 8865 on time. Once they’ve mailed you a notice of the failure, you’ll have 90 days to file the requisite forms. If you miss that deadline, the IRS will charge an additional $10,000 for every 30 days after the 90 days have expired, up to a maximum amount of $50,000 in additional penalties.

There may also be reductions in the foreign taxes available for credit, and in the case of false or fraudulent information, you could be subject to criminal penalties.

For more details, see the IRS instructions for Form 8865.

Category 3

If you’re a Category 3 filer and fail to file on time, the IRS may impose a fine up to 10% of the value of your contribution to the controlled foreign partnership, up to a maximum amount of $100,000. (Though if the failure to report is due to intentional disregard, this limit will not apply.)

For more, see the IRS instructions for Form 8865.

Category 4

If you’re a Category 4 filer, the penalties will largely be the same as those for a Category 1 or 2 filer.

For more, see the IRS instructions for Form 8865.

Get Expert Help With Form 8865

Hopefully, this article has given you a better understanding of IRS Form 8865. If you’d like some more help, we’d be happy to lend a hand.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

Featured In