Form 5471: Filing Requirements with Your Expat Taxes

Living abroad as a US expat is the adventure of a lifetime, especially when you can live out your professional dreams of becoming an entrepreneur.

While this lifestyle typically affords you the flexibility you desire, it does bring specific expat tax requirements that you should be aware of. This article will highlight the top questions expats have about filing Form 5471, as an overseas business owner, alongside your US taxes.

Key Takeaways

- The purpose of Form 5471 is to ensure that the IRS has access to the information it needs to enforce tax laws concerning the varied activities of foreign corporations and their owners.

- Form 5471 is required when a foreign corporation has US shareholders, officers, or directors and certain stock ownership thresholds are reached.

What is Form 5471?

Officially known as Form 5471, Information Return of US Persons with Respect to Certain Foreign Corporations, this form is required to be filed along with your income tax return for US citizens and US resident aliens who are officers, directors, or shareholders in certain foreign corporations.

Who Must File Form 5471?

The filing requirement for IRS Form 5471 is much broader than many US expat taxpayers realize. Not everyone needs to include Form 5471 each year as part of their tax return – they might need to file it every few years or so. There are also filing requirements for people who become Directors or Officers of a foreign corporation that has stock owned by US shareholders, even if they are not direct shareholders. To add to the complexity, foreign persons who later become US citizens or Green Card Holders will need to disclose any ownership they have in a foreign corporation.

Who must file Form 5471, and how often do they need to file it? A comprehensive answer to that is too complex for this article, but we are going to cover the most common situations when it is required.

- Any US taxpayer who owns more than 50% of a foreign corporation needs to file Form 5471 annually. This includes US citizens, Green Card holders, and US-based companies.

- Family members may have to file Form 5471 because of the shares you own, and vice versa.

- Setting up other companies to own shares in the foreign corporation to avoid filing Form 5471 generally does not work. Any shares held by companies you own are generally deemed owned by you for purposes of filing form 5471.

- US citizens who are officers or directors of foreign corporations may have to file form 5471 if any US taxpayer’s ownership of the foreign corporation changes by 10% or more.

More information about the categories of filers can be found on the IRS website. Correctly understanding which category filer you are is essential because Form 5471 schedules and reporting requirements vary by category.

How Do I Determine My Company Structure?

Even if your foreign business is not considered a corporation in your resident country, it is not safe to assume you do not have a Form 5471 filing requirement. The IRS has expanded the term “corporation” when deciding who must file Form 5471.

For example, if the structure provides the owner(s) with limited or no liability, it will likely be considered a corporation by IRS standards. Some foreign companies may have the option to elect “disregarded entity” status by filing Form 8832 within 75 days of the company’s formation to avoid the Form 5471 annual filing requirement. However, it is important to know that other informational reporting will be required instead, such as Form 8865 or Form 8858. These forms are less complex than Form 5471 but will likely still require the input of a tax professional to complete properly. No matter which forms you file, it is important to make sure the forms are correct in order to avoid the hefty foreign reporting penalties, which start at $10,000.

Click here to learn more about reporting requirements for different company structures.

Will Form 5471 Impact My US Tax Liability?

Possibly. Shareholders of a corporation are generally not taxed on the corporation’s profits. Shareholders are typically only taxed when they receive dividends or when they sell their shares.

However, the IRS has many complex tax laws to prevent a US citizen from setting up an offshore company to avoid US tax. These rules may require the shareholder to include some or all of the corporation’s profits as their taxable income, even if they have not received a dividend. These “income inclusion” rules are commonly known as GILTI (guilty), Sub Part F, and effectively connected income (EFI).

When you live in the US, tax day is simple: April 15th! When you move abroad, it’s not so straightforward! Learn about all the expat deadlines and extensions you need to know to file.

What is the Deadline?

If you meet the requirements above, you’ll need to file Form 5471 with your US income taxes. The US expatriate tax deadline is June 15th, as the IRS grants an automatic two-month extension for those living abroad on Tax Day (April 15th every year). You may also request an additional extension until October 15th. Keeping track of the deadlines and filing on time is essential to avoid penalties and interest!

The tax filing requirements for expat business owners are complex, so consulting with a tax professional is always a recommended step.

What Happens If I Don’t File Form 5471?

The IRS has recently been cracking down on US persons who fail to file US tax returns. In addition to penalties for failing to file an individual return, the IRS reserves the right to assess an additional penalty for failing to file Form 5471. For each year that this form is not filed, the IRS can assess a penalty of $10,000.

If the IRS has specifically requested the US person to file this form and the US person has not complied, the IRS can assess an additional $10,000 per month (after the first 90 days), up to a total of $50,000. The IRS describes the potential penalties and their assessments in more detail on its website.

The IRS normally has three years to audit you under the statute of limitations, but this is not the case with Form 5471. For any year you have not filed a Form 5471 when required, the IRS can go back and audit your entire tax return no matter how much time has passed.

The IRS has put a lot of focus on US citizens living abroad who are not in compliance with their US expat tax filing obligations. They have recently entered into agreements with numerous foreign countries to exchange information regarding foreign activities, and noncompliance is more likely to be discovered.

If you believe you might be subject to Form 5471 filing requirements, it is recommended to become compliant sooner rather than later to avoid the potential $10,000 penalty for failing to file this form.

Can I File Form 5471 Myself?

Yes, you can file Form 5471 by yourself. Instructions, forms, and schedules can be found on the IRS’s website.

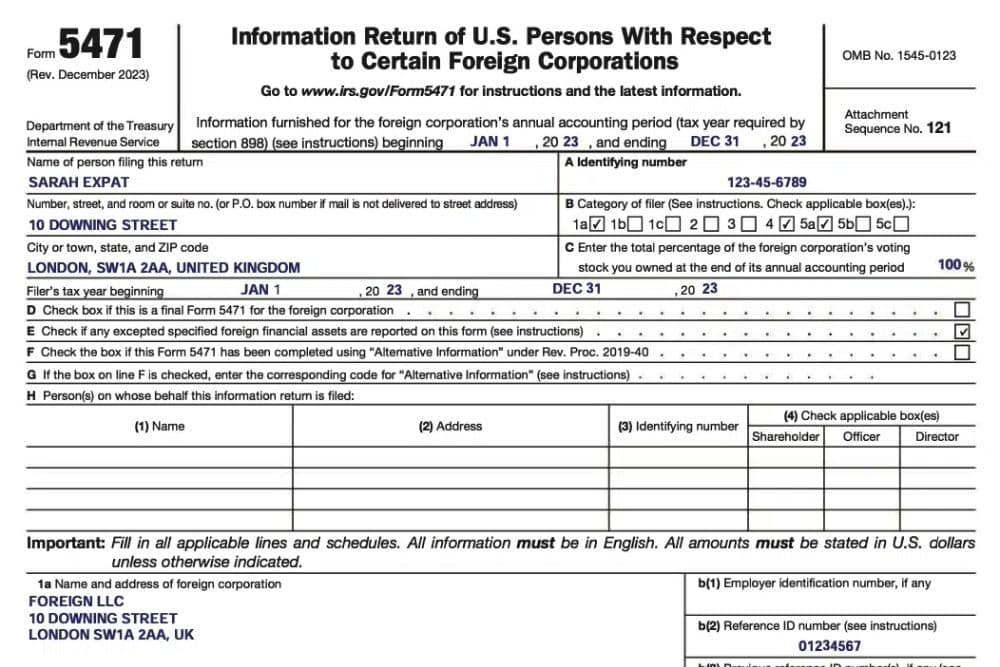

An example of Page 1 of the form is seen below, but for specific Form 5471 instructions, it’s usually best to work with a seasoned expat tax professional service like Greenback to avoid any mistakes and navigate the nuances. You can also visit the official IRS website for more information.

Need Help Filing Form 5471 for Your Foreign Business? We Can Help!

Our team of expert accountants has particular expertise in helping Americans abroad file their expat taxes with a hassle-free experience, including Form 5471.

Contact us, and one of our customer champions will gladly help. If you need very specific advice on your specific tax situation, you can also click below to get a consultation with one of our expat tax experts.

Featured In