US Citizen with a Foreign Business: Tax Reporting Requirements

As more business is conducted internationally, more US citizens are involved with foreign businesses. Depending on the type of foreign business that is being conducted, there are different applicable reporting requirements for US tax purposes.

This article describes the significant US reporting requirements for US citizens with foreign businesses.

Key Takeaways

- US citizens involved with foreign businesses must file various reporting forms, including Form 5471 and Form 926 (foreign corporations), Form 8865 (foreign partnerships), Form 8858 (foreign limited liability companies), Form 3520 and Form 3520-A (foreign trusts), and FBAR.

- Form 8832 enables a foreign limited liability company to elect to be classified as a corporation, partnership, or disregarded entity for US tax purposes.

- Failure to timely file a required reporting form can subject a US citizen to significant civil and criminal penalties.

Foreign Corporations

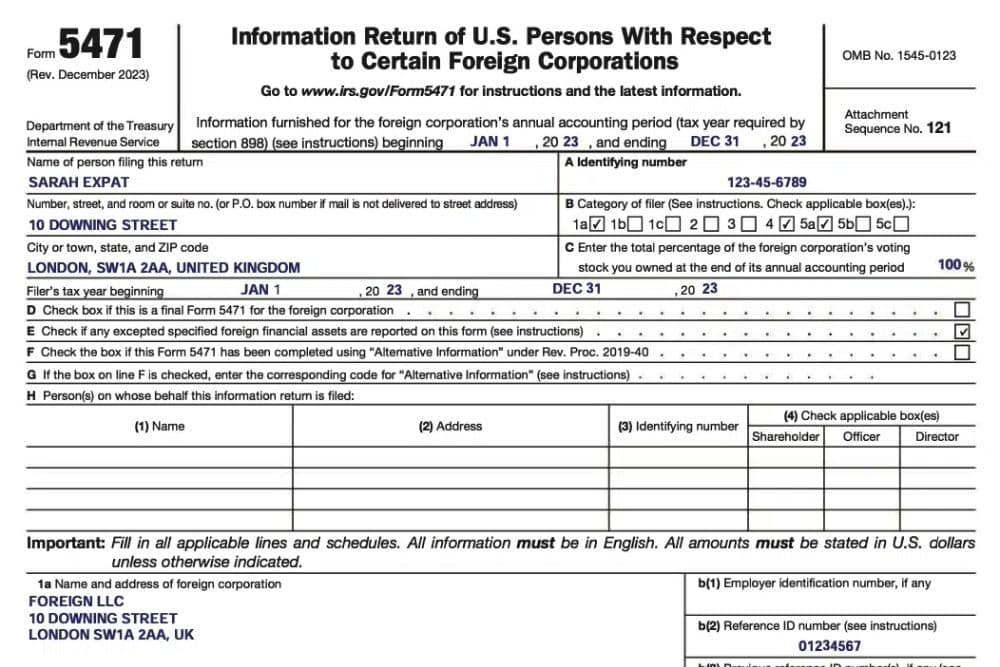

If a US citizen is involved with a foreign corporation, a key reporting requirement is Form 5471, “Information Return of US Persons With Respect to Certain Foreign Corporations.”

Form 5471

There are generally five categories of US citizens who are required to file Form 5471:

- A US citizen who owns (directly, indirectly, or constructively) 10% or more of the stock of a “section 965 specified foreign corporation” (SFC). An SFC is a “controlled foreign corporation” (CFC) (as described below) or any foreign corporation with respect to which one or more domestic corporations own (directly, indirectly, or constructively) 10% or more of the stock of an SFC;

- A US citizen who is an officer or director of a foreign corporation in which a “Category 2/Category 3 US person” has acquired 10% or more of the stock or an additional 10% or more of the stock. A “Category 2/Category 3 US person” is a US citizen or resident, a domestic partnership, a domestic corporation, and an estate or trust that is not a foreign estate or trust;

- A US citizen who (a) acquires stock in a foreign corporation and thereby owns 10% or more of the stock of such corporation, (b) is treated as a “United States shareholder” with respect to a foreign corporation under Internal Revenue Code Section 953(c), (c) becomes a “Category 2/Category 3 US person” while meeting the requirement of owning 10% or more of the stock of a foreign corporation, or (d) disposes of sufficient stock in a foreign corporation to own less than 10% of the stock of such corporation;

- A US citizen who owns more than 50% of the stock of a foreign corporation; and

- A US citizen who owns any stock of a CFC. A CFC is a foreign corporation with US shareholders that own (directly, indirectly, or constructively) more than 50% of the stock of such a corporation.

Form 926

As an additional key reporting requirement for a US citizen involved with a foreign corporation, a US citizen who transfers certain property to a foreign corporation is required to file Form 926, “Return by a U.S. Transferor of Property to a Foreign Corporation.” Transfers of cash to a foreign corporation that result in a US citizen holding, directly or indirectly, at least 10% of the stock of the corporation or that aggregate more than $100,000 over a 12-month period are examples of property transfers that can require the filing of Form 926.

Filing of Form 5471 and Form 926

Form 5471 and Form 926 are filed with the US citizen’s income tax return.

Foreign Partnerships

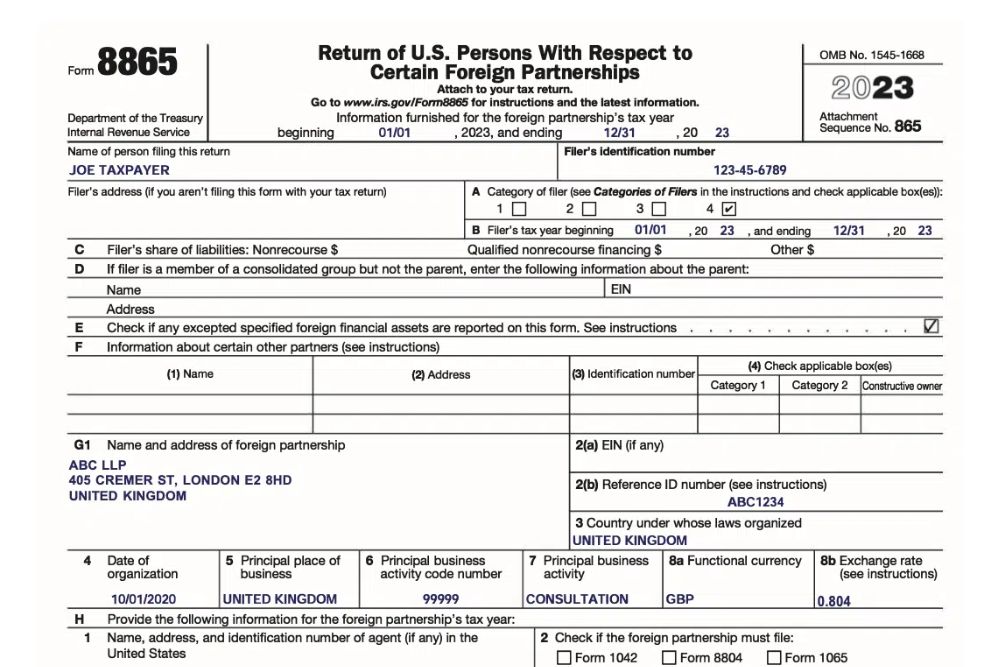

If a US citizen is involved with a foreign partnership, a key reporting requirement is Form 8865, “Return of U.S. Persons With Respect to Certain Foreign Partnerships.”

There are generally four categories of US citizens who are required to file Form 8865:

- A US citizen who “controls” a foreign partnership. Control of a foreign partnership for purposes of Form 8865 is ownership of more than a 50% interest in the partnership;

- A US citizen who owns a 10% or greater interest in a foreign partnership while the partnership was “controlled” (as described above) by US persons, each owning at least a 10% interest;

- A US citizen who contributes property to a foreign partnership in exchange for an interest in such partnership, if either (a) the US citizen owns directly or constructively at least a 10% interest in the partnership immediately after the contribution, or (b) the value of such contributed property (when added to the value of any other property contributed to the partnership by the US citizen) exceeds $100,000 over a 12-month period; and

- A US citizen who has a reportable event under Internal Revenue Code Section 6046A (certain acquisitions, dispositions, and changes in proportional interests with respect to a foreign partnership).

Form 8865 is filed with the US citizen’s income tax return.

Schedule K-2 and K-3 for International Partnership Tax Reporting

If you’re a partner in an international partnership, you need to be aware of Schedule K-2 and K-3 forms. These forms are essential for accurately reporting international partnership tax information, especially foreign income, on K-1s.

The IRS introduced Schedule K-2 and K-3 in 2021 as part of their efforts to improve foreign income reporting on K-1s. All partnerships reported on Form 8865 are considered foreign and have foreign income on the K-1 by default. Therefore, every time you file Form 8865, you must include Schedule K-2 and K-3.

- Schedule K-2 reports international tax information relevant to a partnership’s operations, such as foreign taxes paid, income from foreign sources, and other deductions or credits related to foreign activities.

- Schedule K-3, on the other hand, is used to report partners’ shares of the items reported on Schedule K-2. Partners must also include the information reported on Schedule K-3 on their tax or information returns, if applicable.

Failing to include Schedule K-2 and K-3 with Form 8865 can result in penalties and fines. Therefore, it’s crucial to understand and comply with these requirements to avoid any issues with the IRS.

Foreign Limited Liability Companies

Form 8832

Under Form 8832, “Entity Classification Election”, a foreign limited liability company can elect to be classified as:

- An association taxable as a corporation;

- A partnership; or

- A disregarded entity, generally requires a single owner of the foreign limited liability company.

If electing to be classified as an association taxable as a corporation, the foreign limited liability company will be subject to foreign corporation reporting requirements (including Form 5471 and Form 926 as described above). If electing to be classified as a partnership, the foreign limited liability company will be subject to foreign partnership reporting requirements (including Form 8865 as described above).

But, If electing to be classified as a disregarded entity, the foreign limited liability company does not file a separate tax return; instead, the tax attributes of the limited liability company flow through to the US income tax return of the single owner of such limited liability company.

Form 8858

A US citizen who is the single owner of a “disregarded entity” foreign limited liability company generally is required to file Form 8858, “Information Return of U.S. Persons With Respect to Foreign Disregarded Entities (FDEs) and Foreign Branches (FBs)

Foreign Trusts

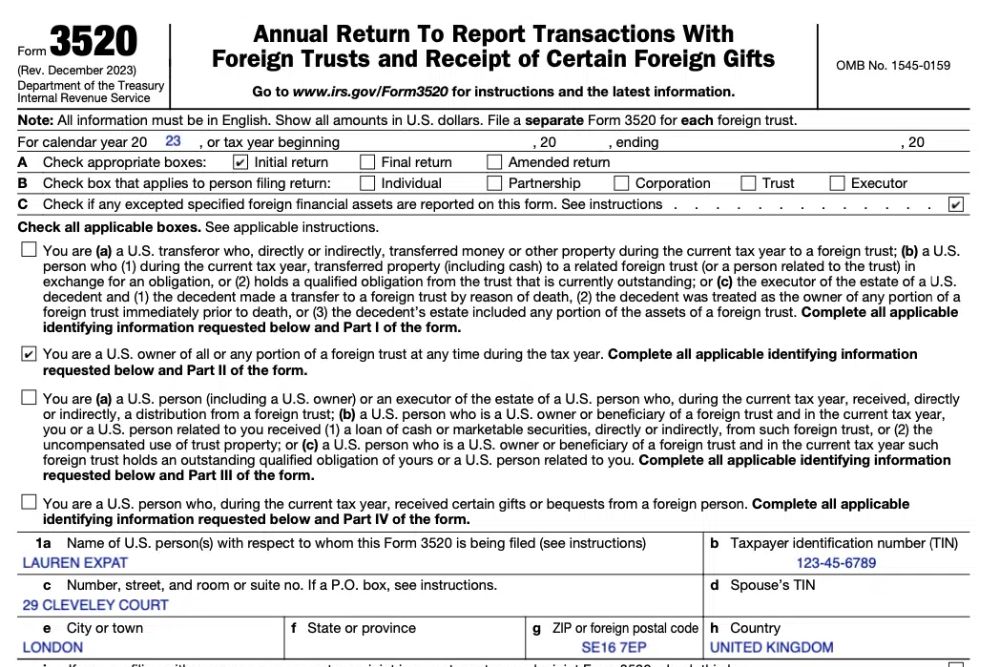

Form 3520

If a US citizen is involved with a foreign trust, a key reporting requirement is Form 3520, “Annual Return to Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts.”

A US citizen generally is required to file Form 3520 when:

- A US citizen is the grantor of a foreign inter vivos trust that is created;

- A US citizen transfers money or property, directly or indirectly, to a foreign trust; and

- A US citizen is treated as the owner of any part of the assets of a foreign trust under Internal Revenue Code Sections 671 through 679 (the “grantor trust” rules).

Form 3520 is due on the 15th day of the fourth month following the end of the US citizen’s tax year.

Form 3520-A

As an additional key reporting requirement for a foreign trust, a foreign trust with a US person (including a US citizen) that is an owner of any portion of the foreign trust under the “grantor trust” rules is required to file Form 3520-A, “Annual Information Return of Foreign Trust With a U.S. Owner.” While Form 3520-A is filed by a foreign trust, the US person (including US citizen) “owner” of the foreign trust is responsible for ensuring that the foreign trust files Form 3520-A.

Form 3520-A is due by the 15th day of the third month following the end of the foreign trust’s tax year.

FBAR

While, as described above, there are different reporting requirements for foreign corporations, foreign partnerships, foreign limited liability companies, and foreign trusts, there is one reporting requirement applicable to each of these entities – Report of Foreign Bank and Financial Accounts (FBAR).

A US citizen must file an FBAR form to report a financial interest in or signature or other authority over at least one financial account located outside the United States if the aggregate value of those foreign financial accounts exceeded $10,000 at any time during the calendar year reported. Thus, a US citizen who has a signature or other authority over at least one foreign financial account of a foreign corporation, foreign partnership, foreign limited liability company, or foreign trust with an aggregate value of more than $10,000 is required to file an FBAR form.

The FBAR form (also known as FinCEN Form 114) is due on April 15 (with an automatic extension to October 15) for the prior calendar year.

Know Your Form of Business Entity

The terms “foreign corporation,” “foreign partnership,” “foreign limited liability company,” and “foreign trust” used above are all US terms. Many foreign countries use their own language and terminology to define business entities in their countries. It is important for a US citizen with a foreign business to know how the Internal Revenue Service classifies such business.

For example, on Form 8832, certain foreign entities are classified as corporations for US tax purposes. These include a Public Limited Company in Australia, a Sociedade Anonima in Brazil, an Aktiengesellschaft in Germany, a Kabushiki Kaisha in Japan, and an Anonim Sirket in Turkey.

Penalties

Failure to file any of the reporting forms described above is not a minor matter. A US citizen can be subject to significant penalties if these reporting forms are not filed in a timely manner.

Penalties – Form 5471, Form 8865, and Form 8858

Failure to timely file Form 5471, Form 8865, or Form 8858 can subject a US citizen to civil penalties of at least $10,000 and loss of 10% of foreign tax credits, as well as criminal penalties.

Penalties – Form 926

For failure to file Form 926 in a timely manner, a US citizen can be subject to a civil penalty equal to 10% of the fair market value of the subject transferred property at the time of transfer.

Penalties – Form 3520

If Form 3520 is not timely filed, a US citizen can be subject to a civil penalty generally equal to at least the greater of $10,000, 35% of the gross value of any property transferred to the foreign trust, 35% of the gross value of any distributions received from a foreign trust, or 5% of the gross value of the portion of the foreign trust’s assets treated as owned by the US citizen under the “grantor trust” rules.

Penalties – Form 3520-A

If Form 3520-A is not timely filed, a US citizen can be subject to a civil penalty equal to at least the greater of $10,000 or 5% of the gross value of the portion of the foreign trust’s assets treated as owned by the US citizen under the “grantor trust” rules.

Penalties – FBAR

Failure to timely file an FBAR form can subject a US citizen to (i) a “non-willful” failure, civil penalties of at least $14,489 (to be adjusted annually for inflation), and (ii) for a “willful” failure, civil penalties of at least the greater of $144,886 (to be adjusted annually for inflation) or 50% of the balance in the foreign financial account and criminal penalties.

Other Considerations

- The reporting requirements described above only relate to providing information to the Internal Revenue Service. Please note that if the foreign entity has income that is taxable in the United States (generally gross income effectively connected with the conduct of a trade or business within the United States or gross income derived from sources in the United States), the foreign entity also can be required to report this income, file an income tax return, and directly or indirectly pay US taxes; and

- This article only describes the significant US reporting requirements for US citizens with foreign businesses. Please note that there are many other reporting requirements for US citizens with foreign businesses that, due to space limitations, were unable to be included in this article.

Need Help with US Reporting Requirements for Foreign Businesses? We Can Help!

At Greenback Expat Tax Services, we specialize in helping expats manage their US tax obligations. As part of our services, we have the necessary experience to aid expats with the numerous US reporting requirements for foreign businesses (including those not included in this article).

Contact us, and one of our customer champions will gladly help. If you need very specific advice on your specific tax situation, you can also click below to get a consultation with one of our expat tax experts.

Featured In