Filing Form 2555 for the Foreign Earned Income Exclusion

If you are a US citizen living and working abroad, you can take advantage of the Foreign Earned Income Exclusion (FEIE). This tax benefit lets qualifying taxpayers exclude a certain amount of foreign-earned income from US taxation. Earned income includes salary, wages, and self-employment income. It does not include pensions or investment income.

This exclusion is not automatic. To claim the FEIE, you must complete Form 2555 and attach it to your US tax return.

Key Takeaways

- Form 2555 is a tax form that can be filed by US citizens and Green Card Holders who have earned income from outside the United States and Puerto Rico. It is used to claim the foreign earned income exclusion and/or the foreign housing exclusion.

- You can use this form if you plan on living outside of the country for an extended period of time (generally for 330 days or more.)

Use our simple excel calculator to get an estimate of how the foreign earned income exclusion will save you money. It will make your day!

What Information Do I Need to Complete Form 2555?

As with all tax-related matters, adequate record-keeping and advanced preparation make the process go smoothly. To complete Form 2555, you will need to have the following information readily available:

- Employer’s name and address (foreign and US, if applicable),

- International travel calendar, including days you might have worked in the US,

- Prior year Form 2555, if available, and

- Foreign income earnings information.

It’s important to remember that Form 2555 must be completed for each expat. If a husband and wife each live and work abroad, both are required complete a separate Form 2555 and attach the two forms to their joint US tax return.

Even though much of the above information will be the same if they live and travel together, the IRS will consider each FEIE claim separately.

Are You Eligible For Foreign Earned Income Exclusion?

To be eligible to claim the FEIE on your US expat taxes, you must meet one of the two tests: Bona Fide Residence or Physical Presence.

- The Bona Fide Residence Test requires that you live in a foreign country for at least one entire calendar year.

- The Physical Presence Test requires that you are physically present in a foreign country or countries for at least 330 days during any 12-month period. (The 12-month period can be flexible but must start or end within the tax year.

Your tax return due date can be extended through a regular extension on form 4868 or on a special extension form 2350 to meet the requirements of either test.

Completing Form 2555: A Step-by-Step Example

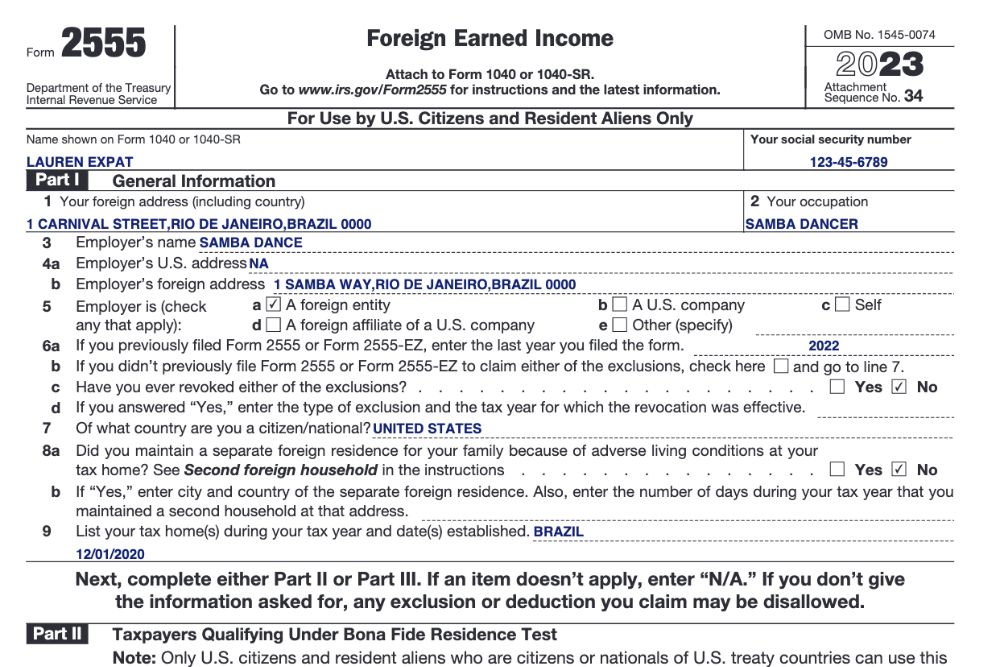

To help better understand how to file Form 2555, let’s take a look at an example: Lauren Expat.

In December 2020, Lauren left her hometown in Montana and moved to Brazil to pursue a career as a professional samba dancer. Because of her great skill, Lauren was immediately hired by a professional dance group and worked all through 2021, earning 5,125 Brazilian Real (REA) per week. During that same year, she traveled to the US to take part in a five-day performance with her dance group.

Because Lauren moved to Brazil in December 2020, she lived in Brazil for all of 2021 – she qualifies for the FEIE under the Bona Fide Residence Test.

Part I: General Information

This is usually the easiest part of Form 2555. Each question is straightforward and requests information you will know without referencing additional paperwork. Remember: there are no predefined answers. You will answer as applicable to your particular situation. In our example, Lauren could list herself as a professional dancer, a samba dancer, or just a dancer.

Part II: Taxpayers Qualifying Under Bona Fide Residence Test

If you are qualifying for the FEIE under the Physical Presence Test, leave Part II blank and complete Part III.

Things get tricky if you work in the United States for any time while residing abroad. Any income earned while in the United States is considered US-based income and not foreign earned. This reduces the amount of income eligible for the FEIE on your US expat taxes.

Dreading the last minute scramble pulling together your tax documents? Despair no more! This simple checklist lists the documents you need to have on hand when preparing to file.

In Lauren’s example, she worked as a dancer in the US for five days. During that time, she earned the equivalent of $950 USD (as she does every week). That week’s income is considered earned in the US and will be fully taxable at US tax rates. (We will discuss this more in Part VII, but it’s important to note that what you put in columns [c] and [d] are very important to your US expat taxes.)

If you earned money while in the US and listed these dollars in column (d), you are required to attach a statement supporting the calculation of your US expat taxes. Again, there is no predefined format, but always include your name and social security on every statement. The IRS wants to know how you calculated the amount earned in the US and will usually expect to see the exchange rate used, which can be obtained from the IRS website.

In 2023, the average conversion rate for REA to USD was 5.395. Thus, Lauren could attach a statement that looked like this:

| Brazilian Real (REA) | United States Dollar (USD) | |

| Weekly Salary | 5,125 | $950 |

| Annualized | 266,500 | $49,400 |

| Amount Earned in the US | 5,125 | $950 |

| Foreign Earned Income | 261,375 | $48,450 |

Part III

If you are qualifying for the FEIE under the Bona Fide Residence Test, leave Part III blank and complete Part II.

Part III requires you to first state the 12-month period that you qualify under for the physical presence test. This does not have to be from January 1st to December 31st. It could be, for example, from April 6th of one year through April 5th of the following year. You can choose the 12-month period that works best for your given situation.

You must also list the country you mostly worked in during the year as well as provide a list of all the countries you were in during the year and what dates you were in each country.

Part IV

This is the section where you list all the income that you are eligible to exclude. This includes salary and wages, minus any income earned while working in the US. It also includes other items most people may not necessarily think of as income such as if your employer provides an apartment for you to live in rent-free and if they pay for your children’s school tuition.

Part VII: Calculate Your Foreign Earned Income Exclusion

This section calculates the actual amount of eligible FEIE on your US expat taxes. The IRS has already been kind enough to complete Line 37 for you, which lists the year’s maximum FEIE. Each year, the maximum FEIE increases. This amount is $120,000 for the 2023 tax year.

Line 38 asks you to enter the number of days within your qualifying period. Because Lauren met the Bona Fide Residence Test, she can enter 365 days here because she was a resident of Brazil for the entire year.

However, IF she had qualified under the Physical Presence Test, things would be a little trickier. Your qualifying period begins when you take up residence in a foreign country. Let’s say you did this on May 1, 2023, and lived there through your filing date of June 15, 2023 (expats get an automatic two-month extension on their US expat taxes). In this case, your “qualifying period” would be May 1, 2023, through June 15, 2023. The number of days during your qualifying period that falls within 2023 would be 245 (May 1, 2023, through December 31, 2023).

Line 39 calculates the percentage of time you resided abroad. Because Lauren was in Brazil for the entire calendar year, her percentage is 1.000, which is 100%. Use this percentage to multiply against the maximum FEIE as shown on line 37, to calculate the amount of FEIE for which you’ll be eligible and enter this number on line 40. Again, Lauren resided abroad for the entire calendar year, so she will be eligible for the maximum FEIE on her US expat taxes.

On Line 41, enter the amount of income that was earned in a foreign country. If you have income earned in the US while maintaining a foreign residence, exclude this from the amount you enter on Line 41. Lauren earned $49,400 for the entire 2023 calendar year. However, the week that she worked in the US would not be considered “foreign earned” and that $950 will be excluded from Line 41.

Enter the lesser of Line 40 or Line 41 on Line 42, and you will have your final Foreign Earned Income Exclusion for the year. Enter the FEIE as a negative amount on Form 1040, Schedule 1, line 8d “Foreign Earned Income Exclusion from Form 2555,” and on Form 1040 line 8, “Other Income,” of your US expat taxes.

Lauren must still show her total salary on Line 1 of Form 1040 of her US expat taxes for total wages and salaries of $49,400. However, because she qualified for the FEIE and correctly claimed it on her Form 2555, she eliminated $48,450 of income from being taxed.

Completing Form 2555 may look complicated at first, but armed with a good example and all of your organized records, it should take you less than 45 minutes to complete. Better yet, let us help you file for this form seamlessly.

Still Have Questions on Form 2555? We Have Answers!

We hope this guide has helped you understand Form 2555 and the Foreign Earned Income Exclusion. If you have any more questions about Form 2555 or your US expat taxes, we can help.

Contact us, and one of our customer champions will be happy to help. If you need very specific advice on your specific tax situation, you can also click below to get a consultation with one of our expat tax experts.

Featured In