Form 709 for U.S. Expats Explained: Gift Tax Rules, Thresholds, and Filing Requirements

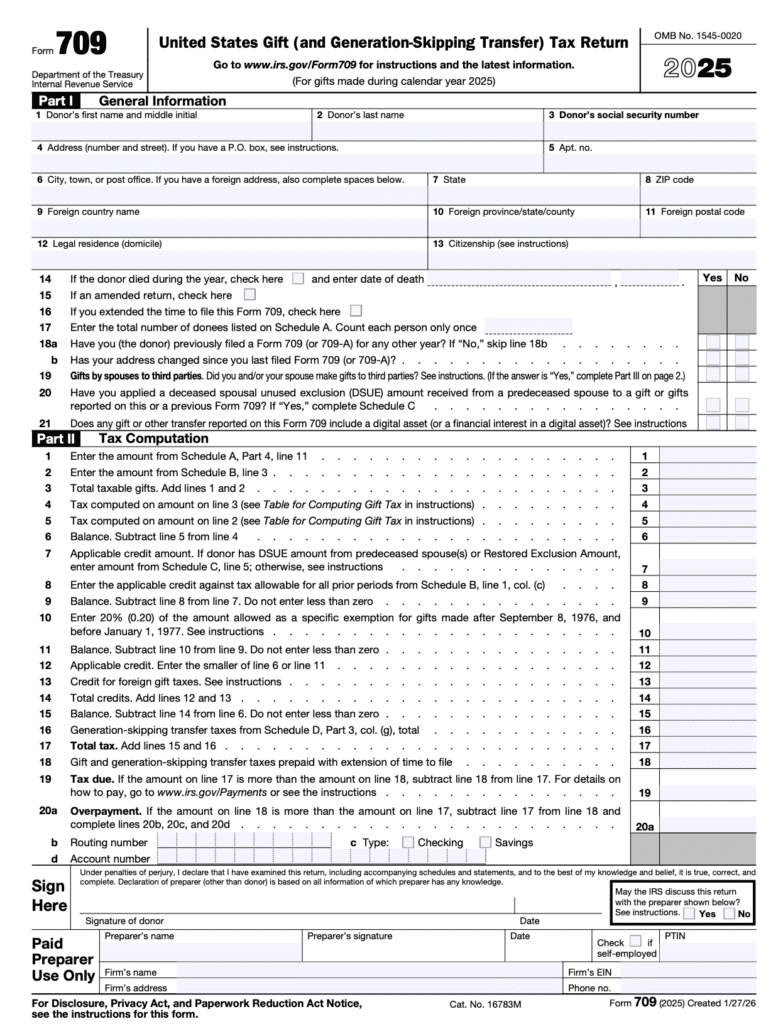

You must file Form 709 (United States Gift and Generation-Skipping Transfer Tax Return) if you gave more than $19,000 to any single person during the 2025 tax year. Filing the form does not mean you owe gift tax. Thanks to a lifetime exemption of $13.99 million per individual (2025), which the OBBB permanently increased to $15 million starting in 2026, most filers never owe a dollar in gift tax. Form 709 is primarily an informational return that tracks your use of this lifetime exemption.

According to the IRS, you must also file Form 709 when gift-splitting with your spouse (even if each share is under $19,000) or when making gifts to a non-citizen spouse exceeding $190,000 (the 2025 limit). For expats, the most common filing triggers include:

- Gifts to non-citizen spouses: The unlimited marital deduction does NOT apply; gifts over $190,000 require Form 709

- Property transfers abroad: Giving foreign real estate or business interests to family members

- Gift splitting: Electing to split gifts with your spouse requires filing even when under the $19,000 per-person limit

- Gifts from foreign persons: You don’t file Form 709, but you may need Form 3520 if receiving gifts over $100,000 from a foreign individual

Here’s when Form 709 is required, how the lifetime exemption works, what’s different for expats with non-citizen spouses, and the most common mistakes to avoid. For a broader overview of gift tax rules, see our gift tax guide for expats.

Not Sure If Your Gift Requires Form 709?

Here’s when Form 709 applies, what counts as a taxable gift, and why expats and cross-border gift-givers need to be especially careful.

What Counts as a Taxable Gift?

The IRS considers a gift to be any transfer of cash, property, or other value to someone without receiving equal value in return. This includes cash, stocks, real estate, vehicles, forgiven debts, and even interest-free loans.

Not every gift triggers Form 709, however. The $19,000 annual exclusion applies per recipient. If you give $15,000 each to five different people, no filing is needed. But if you give one person $20,000, you must report the full gift on Form 709, even though only $1,000 exceeds the exclusion.

For married couples, the combined annual exclusion is $38,000 per recipient when electing to split gifts. However, gift splitting requires both spouses to file Form 709, even if neither spouse individually exceeds the $19,000 threshold.

Which Gifts Are Exempt From Filing?

Certain transfers are excluded from gift tax regardless of amount, and you generally do not need to file Form 709 for them:

| Exempt Gift Type | Key Condition |

|---|---|

| Tuition payments | Must be paid directly to the educational institution |

| Medical expenses | Must be paid directly to the medical provider |

| Gifts to your U.S. citizen spouse | Unlimited marital deduction applies |

| Gifts to political organizations | For the organization’s use |

| Charitable donations | Deductible if you itemize; may still require Form 709 reporting |

The unlimited marital deduction only applies if your spouse is a U.S. citizen. If your spouse is not a U.S. citizen, the annual exclusion for spousal gifts is capped at $190,000 for the 2025 tax year. Exceeding this amount requires filing Form 709, and the excess counts against your lifetime exemption. This is a common surprise for expat couples with a non-citizen spouse.

Will I Owe Gift Tax?

For the vast majority of filers, the answer is no. Form 709 is primarily an informational return that tracks your use of the lifetime gift and estate tax exemption.

Here’s how it works: the $13.99 million lifetime exemption (for 2025) covers all taxable gifts that exceed the annual exclusion. Each time you file Form 709, the excess above $19,000 is subtracted from your lifetime exemption. You will not owe gift tax until your cumulative lifetime gifts exceed that $13.99 million threshold. Once you surpass it, additional gifts are taxed at rates up to 40%.

For context, if you gave one child $50,000 in 2025, you would report the full gift on Form 709. The first $19,000 is covered by the annual exclusion. The remaining $31,000 would reduce your lifetime exemption from $13.99 million to $13,959,000. No tax would be owed.

The One Big Beautiful Bill Act, signed into law on July 4, 2025, increased the lifetime exemption to $15 million per individual starting in 2026, with inflation adjustments going forward. This replaced the previously planned reduction that would have cut the exemption roughly in half. If you have been delaying large gifts out of concern about the exemption dropping, the law now provides more certainty for long-term planning.

How Do Gift Tax Rules Apply to Expats and Cross-Border Situations?

Gift tax rules become significantly more complex when a foreign person is involved in the transaction. The rules depend on who is giving the gift:

- U.S. person gives a gift: If you are a U.S. citizen or resident and you make a taxable gift to anyone, whether the recipient is in the U.S. or abroad, you must file Form 709. The recipient’s citizenship or location does not matter.

- Foreign person gives a gift to a U.S. person: The foreign donor generally does not need to file Form 709 (unless the gift is tangible property located in the U.S.). However, the U.S. recipient may need to report the gift on Form 3520 if the total gifts from foreign individuals exceed $100,000 in a year, or approximately $20,559 for gifts from foreign corporations or partnerships.

Failing to file Form 3520 when required can result in penalties of up to 25% of the gift amount. This catches many expats off guard, particularly those receiving large gifts or inheritances from foreign family members.

For Americans living abroad, cross-border gift situations can also intersect with local gift or inheritance tax rules in your country of residence, creating potential dual-reporting obligations that require careful coordination.

When Is Form 709 Due?

Form 709 is due on the same date as your individual income tax return: April 15, 2026, for the 2025 tax year. Americans living abroad receive an automatic extension to June 15, 2026, and can request a further extension to October 15, 2026, by filing Form 4868 (which extends both your income tax return and Form 709).

Form 709 can now be e-filed through the IRS Modernized e-File system starting with the 2024 tax year. Previously, it could only be filed on paper.

Why Gift Tax Filing Is More Complex Than It Looks

Form 709 may seem straightforward when you are reporting a simple cash gift above the annual exclusion. But the form becomes significantly more complicated in situations involving gift splitting between spouses, gifts of partial interests in property, transfers to trusts, gifts of hard-to-value assets (private business interests, art, real estate), cross-border gifts involving non-citizen spouses, and generation-skipping transfers. In these cases, improper reporting can result in penalties, unintended use of your lifetime exemption, or missed planning opportunities.

Let Greenback Handle Your Gift Tax Filing

Between gift splitting elections, non-citizen spouse rules, cross-border reporting, and lifetime exemption tracking, Form 709 involves more nuance than most taxpayers expect. A mistake does not just affect this year’s return; it permanently reduces your lifetime exemption and can trigger penalties.

Greenback’s CPAs and Enrolled Agents handle gift tax returns alongside your expat tax filing, ensuring Form 709 is filed correctly and coordinated with Form 3520 and any other cross-border reporting requirements.

No matter how late, messy, or complex your return may be, we can help. You’ll have peace of mind, knowing that your taxes were done right.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on taxes or working with Greenback, contact us, and one of our Customer Champions will happily address all your concerns.

Form 709 Is Often Required Even If No Tax Is Owed

This article is intended for informational purposes only and does not constitute legal or tax advice. While Greenback makes every effort to ensure the information is accurate and up-to-date, every tax situation is unique. For advice tailored to your specific situation, consult one of our expat tax professionals.

Related Resources