FATCA Explained: Form 8938 Filing Requirements for Expats

- What Are the FATCA Filing Requirements?

- What Are the FATCA Filing Thresholds?

- What Foreign Assets Must I Report Under FATCA?

- How Do I File Form 8938 for FATCA?

- When Is FATCA Due?

- Is FATCA the Same as FBAR?

- What Are the Penalties for FATCA Non-Compliance?

- Will I Owe U.S. Tax on My Foreign Accounts?

- How Does FATCA Work With Foreign Banks?

- Why Does FATCA Exist?

- FATCA Reporting Services

- Frequently Asked Questions About FATCA

- Related Resources

FATCA (the Foreign Account Tax Compliance Act) is a U.S. law that requires Americans with foreign financial assets above $50,000 to report them to the IRS on Form 8938. It also requires foreign banks in over 110 partner countries to report U.S. account holders directly to the IRS, which means the IRS likely already knows about your accounts.

According to the IRS, you must file Form 8938 if your specified foreign financial assets exceed any of these thresholds:

- Single, U.S. resident: $50,000 year-end OR $75,000 anytime

- Married filing jointly, U.S. resident: $100,000 year-end OR $150,000 anytime

- Single, living abroad: $200,000 year-end OR $300,000 anytime

- Married filing jointly, living abroad: $400,000 year-end OR $600,000 anytime

Filing Form 8938 does not mean you owe additional U.S. tax. Most filers can reduce their U.S. tax bill to $0 using the Foreign Earned Income Exclusion or Foreign Tax Credit. Here’s exactly who needs to file, what assets count, and how to comply.

Not Sure If You Need to File FATCA?

What Are the FATCA Filing Requirements?

FATCA filing requirements apply to all U.S. persons, a tax term that includes:

- U.S. citizens living anywhere in the world, including dual citizens and “Accidental Americans.”

- Green card holders (lawful permanent residents), even those living outside the U.S.

- Tax residents who meet the substantial presence test

- Certain trusts and estates with U.S. beneficiaries

If you fall into any of these categories and hold foreign financial assets above the reporting thresholds, you have a FATCA filing obligation. This is true whether you live in the United States or abroad, whether you owe U.S. tax or not, and whether your foreign accounts generate income or sit dormant.

What Are the FATCA Filing Thresholds?

You must file Form 8938 when your specified foreign financial assets exceed certain thresholds. These amounts vary based on where you live and how you file your taxes.

| Your Situation | Reporting Required When Assets Exceed |

|---|---|

| Single, living in the U.S. | $50,000 on Dec 31 OR $75,000 anytime during the year |

| Married filing jointly, living in the U.S. | $100,000 on Dec 31 OR $150,000 anytime during the year |

| Single, living abroad | $200,000 on Dec 31 OR $300,000 anytime during the year |

| Married filing jointly, living abroad | $400,000 on Dec 31 OR $600,000 anytime during the year |

Notice that thresholds are significantly higher for Americans living outside the United States. Congress recognized that expats often need larger foreign account balances to cover living expenses in their country of residence.

You must apply BOTH the year-end test AND the any-time-during-year test. If you exceed either threshold, you have a reporting obligation.

For a step-by-step walkthrough of completing Form 8938 line by line, including how to value each asset and which Part of the form to use, see our Form 8938 filing guide.

What Foreign Assets Must I Report Under FATCA?

FATCA requires reporting of “specified foreign financial assets,” which include a wide range of holdings.

Foreign Financial Accounts

- Bank accounts (checking, savings, money market)

- Brokerage and securities accounts

- Mutual fund accounts held abroad

- Commodity and derivatives accounts

Foreign Investments and Interests

- Stock or securities issued by non-U.S. entities

- Partnership interests in foreign partnerships

- Beneficial interests in foreign trusts

- Foreign pension plans and deferred compensation

- Life insurance policies with cash value issued by foreign insurers

- Foreign hedge fund interests

What About Foreign Real Estate?

Direct ownership of foreign real estate (titled in your own name) is NOT a specified foreign financial asset under FATCA. Your vacation home in Portugal or rental property in Mexico doesn’t count toward the threshold.

However, if you own property through a foreign corporation or partnership, that entity’s ownership must be reported. The distinction matters: it’s not the real estate itself, but rather your ownership stake in the foreign entity holding the property.

When determining whether an asset qualifies, remember that there are no penalties for over-reporting, only for omitting required assets. If you’re unsure, it’s safer to include it.

Some taxpayers qualify for specific exemptions based on their circumstances. Learn more about FATCA exemptions to see if you can avoid unnecessary reporting.

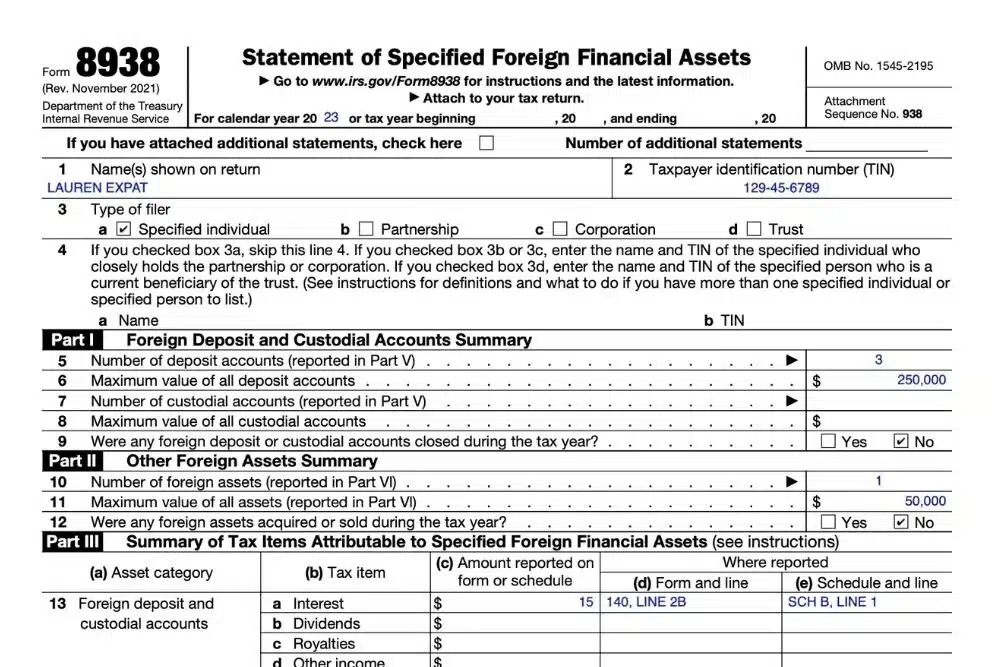

How Do I File Form 8938 for FATCA?

Form 8938 is officially called a Statement of Specified Foreign Financial Assets. You file this form alongside your regular tax return (Form 1040).

For each reportable asset, you provide:

- Asset description and identifying information

- Maximum value during the tax year

- Whether the asset generated taxable income

- Name and address of the financial institution (for accounts)

The form itself is relatively straightforward once you’ve gathered the necessary information. The challenge typically lies in determining which assets to include and accurately calculating their maximum values in U.S. dollars using the Treasury’s official year-end exchange rates.

When Is FATCA Due?

Form 8938 is due with your federal income tax return. For most filers, that’s April 15. Americans living abroad get an automatic two-month extension to June 15, and anyone can request a further extension to October 15 by filing Form 4868.

| Your Situation | Form 8938 Deadline | Extension Available |

|---|---|---|

| U.S. resident | April 15 | October 15 (file Form 4868) |

| Living abroad | June 15 (automatic) | October 15 (file Form 4868) |

| Active military in combat zone | 180 days after leaving combat zone | Varies |

FATCA does not have a separate filing system. Form 8938 is attached to your Form 1040 and submitted together. This is different from the FBAR, which is filed separately through FinCEN’s BSA E-Filing System.

Is FATCA the Same as FBAR?

No. Many people confuse FATCA with FBAR (Foreign Bank Account Report) filing, but they have different requirements and different rules.

FBAR (FinCEN Form 114):

- Lower $10,000 threshold

- Covers only foreign financial accounts

- Filed separately with the Financial Crimes Enforcement Network (FinCEN)

- Due April 15 with automatic extension to October 15

FATCA (Form 8938):

- Higher thresholds ($50,000 to $600,000, depending on filing status and residency)

- Covers accounts PLUS other foreign assets like stocks and partnerships

- Filed with your income tax return (Form 1040)

- Due when your tax return is due, including extensions

You may need to file both forms if you meet the respective thresholds. The forms go to different agencies through different systems, so filing one does not satisfy the other. If your foreign accounts exceed $10,000, you’ll likely need to file FBAR in addition to Form 8938.

What Are the Penalties for FATCA Non-Compliance?

The IRS imposes substantial penalties for FATCA violations:

- $10,000 for each year you fail to file Form 8938

- An additional $10,000 per month (up to $50,000 maximum) if you continue not filing after IRS notification

- 40% penalty on any tax understatement related to undisclosed foreign assets

These penalties apply on a per-tax-year basis, so multiple years of non-compliance can result in significant financial consequences. The good news? These penalties are completely avoidable by filing correctly and on time.

Most penalty situations stem from incomplete or incorrect Form 8938 filings rather than complete non-filing. Review the Form 8938 instructions and common mistakes before filing.

Will I Owe U.S. Tax on My Foreign Accounts?

Here’s the good news: filing FATCA doesn’t mean you’ll owe U.S. tax. FATCA is an information reporting requirement, not a tax itself.

Most Americans living abroad can use the Foreign Earned Income Exclusion (which excludes up to $130,000 of earned income for the 2025 tax year, rising to $132,900 for 2026) or Foreign Tax Credit to reduce or eliminate their U.S. tax liability. Even if you’re required to report substantial foreign assets, you’ll likely owe little to nothing in actual U.S. taxes.

How Does FATCA Work With Foreign Banks?

FATCA’s reach extends beyond individual reporting. The law requires foreign financial institutions (FFIs), foreign banks, investment funds, and insurance companies to identify U.S. account holders and report them to the IRS. This is enforced through intergovernmental agreements (IGAs) between the U.S. and partner countries.

There are two types of IGAs:

- Model 1 IGA: Foreign banks report U.S. account holder information to their own government, which then shares it with the IRS. Most countries use this model.

- Model 2 IGA: Foreign banks report directly to the IRS with the consent of their account holders. Switzerland, Japan, and a handful of others use this model.

As of 2026, more than 110 countries have signed IGAs with the United States, including every major financial center. This means that if you have a foreign bank account in the UK, Germany, Canada, Australia, Singapore, the UAE, or virtually anywhere else with a developed banking sector, the IRS is already receiving information about your account directly from your bank.

What this means for you: Hiding foreign accounts is no longer realistic. The penalty for an unfiled Form 8938 is far worse than the cost of filing it correctly. If you’ve been non-compliant, the Streamlined Filing Procedures let you catch up before the IRS contacts you first.

Why Does FATCA Exist?

Congress passed FATCA in 2010 to combat tax evasion by Americans hiding money in offshore accounts. Before FATCA, the IRS had limited visibility into foreign financial assets, making it easier for some taxpayers to conceal income from U.S. taxation.

FATCA creates transparency in two ways. First, it requires foreign banks and financial institutions to report information about U.S. account holders directly to the IRS. Second, it requires individual Americans to disclose their foreign assets when the value exceeds specific dollar amounts.

While FATCA filing requirements target intentional tax evaders, they affect millions of honest Americans living abroad who maintain legitimate foreign accounts for everyday expenses, retirement savings, and regular financial planning.

FATCA Reporting Services

FATCA compliance is one of the more technical areas of expat taxation. Calculating the maximum value of foreign accounts in fluctuating currencies, distinguishing reportable assets from exempt ones, and coordinating Form 8938 with related forms (5471, 8865, 3520, 8621) takes meaningful expertise.

Greenback’s FATCA reporting services handle Form 8938 preparation as part of your federal tax return. Our CPAs and IRS Enrolled Agents have deep experience with expat and international tax situations, and every return is prepared from start to finish by a credentialed accountant, never outsourced.

Our FATCA service includes:

- Form 8938 preparation and filing with your federal return

- Asset valuation and currency conversion using Treasury exchange rates

- Coordination with related foreign asset forms

- Streamlined Filing support for catching up on missed years

- Year-round access to your accountant for follow-up questions

If you’re unsure whether you need to file Form 8938, contact our Customer Champions, and we’ll help you determine your obligation. If you’re ready to be matched with an accountant, click the get started button below.

Stay Compliant With FATCA Reporting

Frequently Asked Questions About FATCA

U.S. residents must file Form 8938 if their specified foreign financial assets exceed $50,000 on the last day of the year or $75,000 at any point during the year (for single filers). Married filing jointly residents have a $100,000 year-end and $150,000 anytime threshold. These thresholds are significantly lower than for Americans living abroad.

Yes. If you are a U.S. citizen, FATCA applies to you regardless of whether you also hold citizenship in another country, where you live, or whether you have ever lived in the United States. This includes “accidental Americans” who acquired U.S. citizenship at birth but have spent their entire lives abroad.

No. FATCA reporting applies only to assets held with foreign financial institutions. If you own foreign stocks through a U.S. brokerage like Fidelity or Schwab, those assets do not count toward your FATCA threshold and do not need to be reported on Form 8938.

A FATCA letter (often a W-9 or self-certification request) is what your foreign bank sends you to confirm your U.S. status so they can report your account information to the IRS under their IGA obligations. FATCA reporting is what you do on Form 8938 with your tax return. Receiving a FATCA letter does not satisfy your personal Form 8938 filing requirement; they are separate obligations.

Closing accounts does not erase prior-year reporting obligations. If your foreign assets exceeded the threshold during any prior year, you still owe a Form 8938 for that year. The Streamlined Filing Procedures are the safest way to catch up on past years before the IRS contacts you.

This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Tax laws, thresholds, deadlines, and IRS guidance change frequently, and the rules that apply to your situation depend on your specific facts and circumstances.

Related Resources

- Form 8938 for U.S. Expats

- FATCA Exemptions: Who Qualifies

- FBAR vs. Form 8938

- FBAR Filing Requirements

- Streamlined Filing for U.S. Expats

- Foreign Earned Income Exclusion

- Foreign Tax Credit Guide

- Buying and Selling Real Estate Abroad

- Common U.S. Tax Forms for Expats

- U.S. Expat Taxes: The Complete Guide

Featured In