How Do I Fill Out IRS Form 56 Step by Step?

Form 56 is a one-page form, but filling it out wrong can delay your fiduciary recognition by weeks. The most common errors are incorrect identification numbers, incomplete addresses, and missing court documentation. Get it right the first time, and the IRS typically processes it within 4-6 weeks.

If you’re not sure whether you need Form 56 or want to know what it does, see our complete Form 56 overview first. This guide is purely the how-to: what to enter on each line, what documents to attach, and where to mail it.

Need Help Filing Form 56 Correctly?

What Do I Need Before Starting?

Gather everything before you begin. Missing a single item means stopping mid-form and risking errors.

For the Person You’re Representing

| Item | Details |

|---|---|

| Full legal name | Exactly as it appears on their Social Security card or most recent tax return. No nicknames. |

| SSN or ITIN | Nine digits, no dashes. Double-check this. One wrong digit causes weeks of delay. |

| Last known address | Their most recent address on file with the IRS (use the address from their last tax return). |

| Date of death | If deceased. MM/DD/YYYY format. |

| EIN | If the estate or trust has been assigned one. |

For Yourself (the Fiduciary)

| Item | Details |

|---|---|

| Your full legal name | As it appears on your Social Security card. |

| Your SSN or ITIN | Or EIN if you’re acting through an entity. |

| Your current mailing address | This is where the IRS will send all future correspondence about the taxpayer. Use the address where you reliably receive mail. |

| Court appointment documents | Certified copies of letters testamentary, letters of administration, court order, or trust instrument. |

| Date of appointment | The exact date your fiduciary role became effective. |

Expat tip: If you live abroad, use your current international address. The IRS will mail correspondence there. Consider whether a U.S.-based mailing address (e.g., a trusted family member or registered agent) might be more reliable for receiving time-sensitive notices.

Line-by-Line Instructions

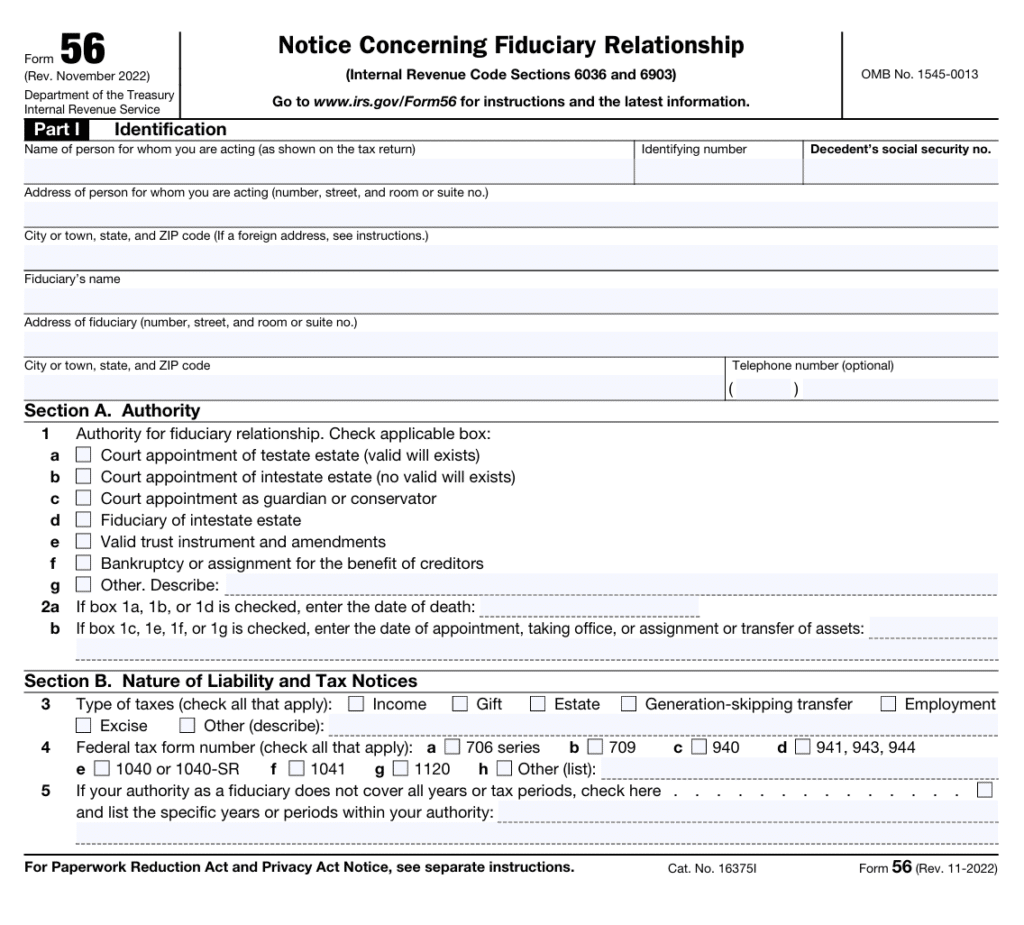

Top Section: Identifying the Taxpayer

- Name of person for whom you are acting: Enter the taxpayer’s full legal name. If deceased, this is the decedent’s name. If you’re acting for a trust, enter the trust name.

- Identifying number: Enter the taxpayer’s SSN, ITIN, or EIN. For a deceased individual, use their SSN. For an estate that has received its own EIN, enter the EIN.

- Decedent’s social security number: If the taxpayer is deceased and you entered an estate EIN above, also enter the decedent’s SSN here.

- Address: Enter the taxpayer’s last known address (street, city, state, ZIP). For foreign addresses, include the country name and postal code in the spaces provided.

- Fiduciary’s name: Your full legal name.

- Fiduciary’s address: Your current mailing address for IRS correspondence. For international addresses, the form has specific fields for city, province/state, country, and postal code.

Section A: Authority

This section establishes what type of fiduciary you are.

| Line | Check if | What to enter on Line 2 |

|---|---|---|

| 1a | You are the executor of a testate estate (the person had a will) | Line 2a: Date of death |

| 1b | You are the administrator of an intestate estate (no will), court-appointed | Line 2a: Date of death |

| 1c | You are a guardian or conservator | Line 2b: Date of appointment |

| 1d | You are the administrator of an intestate estate, with no court appointment | Line 2a: Date of death |

| 1e | You are a trustee | Line 2b: Date of appointment or asset transfer |

| 1f | You are a receiver, bankruptcy trustee, or assignee | Line 2b: Date of appointment |

| 1g | Other (describe your authority in the space provided) | Line 2b: Date of appointment |

Check only one box. If your situation doesn’t fit 1a-1f, use 1g and write a brief description of your authority.

Section B: Nature of Liability and Tax Notices

- Line 3: Check all boxes for the types of taxes you’ll handle on behalf of the taxpayer:

- Income (most common)

- Estate

- Gift

- Employment

- Excise

- Other (specify)

- Line 4: Enter the specific form numbers you’ll be filing (e.g., 1040, 1041, 706, 709) and the tax years or periods covered.

- Line 5: If your authority doesn’t cover all years, check the box and list the specific years or periods.

Be thorough here. If you only check “income” but the estate also has employment tax obligations, the IRS won’t route employment tax correspondence to you. When in doubt, check all applicable boxes.

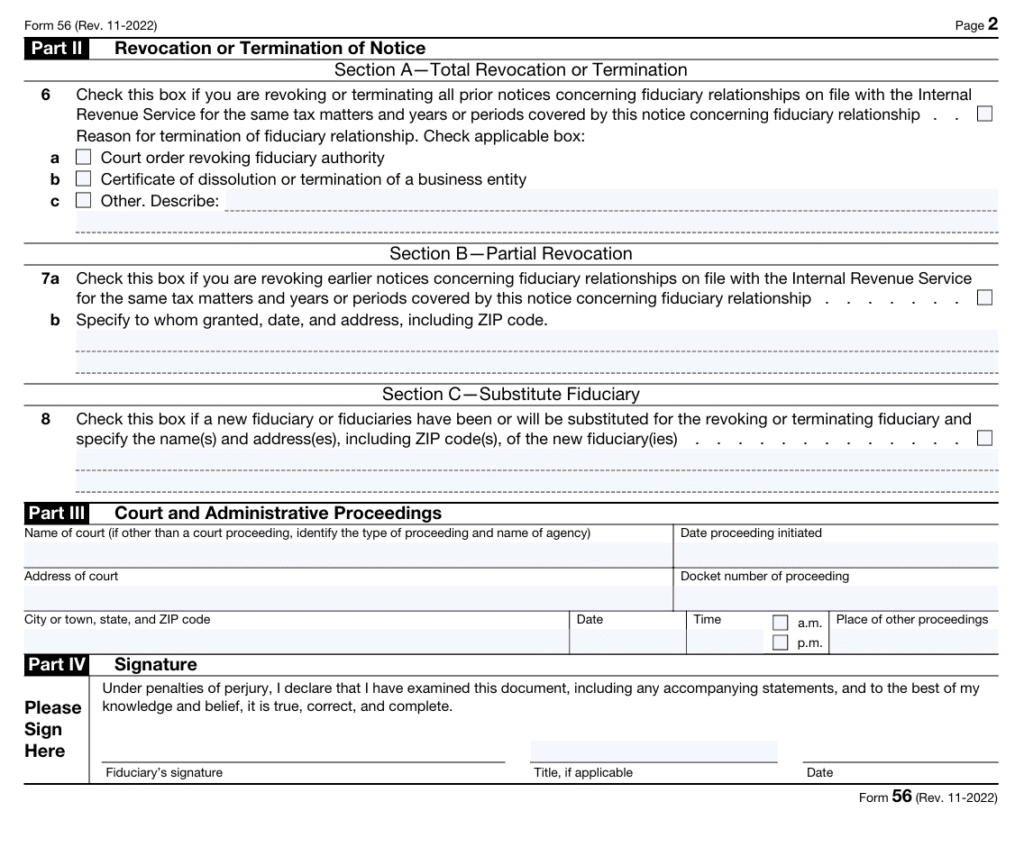

Part II: Revocation or Termination of Notice

Skip this section when you first file. Part II is only used when the fiduciary relationship ends.

When the time comes to terminate:

- Line 6: Check this box to revoke all prior fiduciary notices for the same taxpayer and tax matters.

- Line 7a: Enter the date the fiduciary relationship terminated.

- Line 7b: Check the reason for termination:

- Assets distributed and estate closed

- Fiduciary discharged by court order

- Other (describe)

Signature

You must sign the form by hand. Electronic signatures and stamps are not accepted. Print your name, enter your title (Executor, Trustee, Guardian, etc.), and date the form.

You can download the current form from the IRS website.

What Documents Do I Attach?

Attach certified copies of the document that establishes your authority:

| Fiduciary Type | Attach |

|---|---|

| Executor (testate) | Letters testamentary + death certificate |

| Administrator (intestate) | Letters of administration + death certificate |

| Trustee | Trust instrument (or relevant pages showing your appointment) |

| Guardian/Conservator | Court order of appointment |

| Receiver | Court order of appointment |

Expat tip: If your original court documents are in a foreign language (e.g., you were appointed by a foreign court for a trust with U.S. assets), include a certified English translation.

Where Do I Mail Form 56?

Form 56 cannot be filed electronically. Mail it to the IRS service center where the person you’re representing is required to file their tax returns.

- For most individuals: The correct address depends on the taxpayer’s state of residence. Check the current IRS filing addresses.

- For receivers and assignees: Mail to the Advisory Group Manager of the appropriate IRS area office within 10 days of appointment. See IRS Publication 4235 for contact information.

- Filing from abroad: Use an international express service (FedEx, DHL, UPS) with tracking. Standard international mail can take 2-4 weeks and doesn’t provide delivery confirmation. Keep your tracking receipt as proof of filing.

What Happens After I Submit?

- Processing time: 4-6 weeks in normal periods, potentially longer during tax season (January through April).

- No confirmation letter: The IRS does not send a receipt or acknowledgment that Form 56 was processed. You’ll know it worked when tax correspondence for the taxpayer starts arriving at your address.

- Immediate authority: Your fiduciary responsibilities begin on the date of your appointment, not the date Form 56 is processed. You’re legally responsible from day one, even while the form is in transit.

- Keep copies: Retain a copy of the completed Form 56, all attachments, and your proof of mailing for as long as the fiduciary relationship lasts, plus at least three years after termination.

Frequently Asked Questions

Typically 4-6 weeks. During peak tax season (January through April), processing may take longer. There is no way to expedite processing.

No. The IRS does not send an acknowledgment. You’ll know it’s been processed when taxpayer correspondence starts arriving at your address.

No. Form 56 must be printed, signed by hand, and mailed. Electronic filing is not available for this form.

File a new Form 56 with the correct information. There is no amendment process. The new form supersedes the previous one for the same taxpayer and fiduciary.

Yes. Complete Part II of a new Form 56 to notify the IRS that the fiduciary relationship has terminated. If you skip this step, the IRS will continue treating you as the responsible party and sending correspondence to you.

Yes. The form has specific fields for foreign addresses. Use the address where you reliably receive mail. All IRS notices about the taxpayer will be sent to the address you provide.

Managing fiduciary tax obligations from abroad requires precision. At Greenback, our CPAs and Enrolled Agents prepare Form 56 alongside estate returns, trust filings, and your personal expat tax return, so everything is filed correctly and coordinated.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on fiduciary tax obligations or working with Greenback, contact our Customer Champions.

Get Form 56 Filed the Right Way

This article is for informational purposes only and does not constitute legal or tax advice. For the latest guidance, see the IRS Form 56 instructions. Always consult with qualified legal and tax professionals regarding your specific situation.

Related Resources