2026 FIFA World Cup & Cross-Border Tax Compliance

This summer, the United States, Canada, and Mexico will co-host the largest FIFA World Cup in history: 48 nations and 104 matches across 16 cities. When the U.S. last hosted in 1994, the tournament featured only 24 teams. The 2026 edition is larger in every dimension, and the tax landscape is materially different this time, as the state “jock tax” infrastructure across host states like California, New Jersey, Massachusetts, and Missouri was far less developed 30 years ago.

Report Terminology

To navigate this report, it is helpful to understand three key pillars of international tax law:

- Article 17 (The “Artiste and Athlete” Provision): A treaty article allowing “host” countries to tax athletes from day one, rather than following the standard 183-day residency rule.

- Exemption Thresholds (De Minimis): The “floor” for taxation. If earnings are below this dollar amount, they are federally exempt; if they earn one dollar over, the entire amount is usually taxable.

- Duty Days: The formula used to “slice” a player’s salary based on the ratio of days spent working in a specific state versus their total work year.

Key Findings

1. Treaty status is the primary driver of federal tax exposure.

- Players from non-treaty nations such as Brazil, Senegal, Uruguay, and Saudi Arabia may be subject to U.S. federal withholding, often at 30 percent for independent personal services. The exact treatment depends on how the income is classified and paid, and final tax liability is calculated on a net basis when the player files Form 1040-NR.

- Players from treaty-protected countries may have their U.S. federal tax reduced or eliminated when treaty requirements are met. Separately, a Central Withholding Agreement with the IRS can align withholding with expected net income rather than gross receipts, which helps cash flow during the tournament.

- According to industry estimates, fixed cost of managing this multi-jurisdictional compliance can range from $5,000 to $15,000, which creates a regressive financial burden for mid-tier players

2. Federal treaties provide no protection against state jock taxes.

- Tax treaties cover only the federal income taxes imposed under the Internal Revenue Code and do not extend to state or local revenue departments.

- A player may be fully exempt from federal tax under a “public funds” clause but still owe New Jersey 10.75%, or California 13.3%, on income generated at those venues.

- In practice, treaty protection generally does not extend to state jock taxes, making venue assignment an important tax planning variable.

3. Small differences in treaty wording create significant financial disparities.

- Exemption thresholds vary by a six-to-one range, spanning from $3,000 in the Mexico treaty to $20,000 in the UK and Germany treaties.

- Public funds clauses can eliminate federal liability for national teams, but these are absent from the UK and Japan treaties.

- Even among treaty countries, the standard for exemption varies; Germany requires a visit to be “substantially” publicly funded, while France requires the higher “principally” standard.

4. South Korea and Curaçao face unique jurisdictional hurdles.

- South Korea’s 1976 treaty lacks a modern athlete-specific article, so federal tax analysis runs through the treaty’s general personal services provisions rather than a dedicated Article 17 framework.

- Although Curaçao is a constituent country of the Kingdom of the Netherlands, its players are excluded from the U.S.–Netherlands treaty and face a flat 30 percent federal withholding.

- This exclusion results from the U.S. terminating its treaty relationship with the Netherlands Antilles in 1987 to prevent treaty shopping.

5. Host city tax environments vary significantly across North America.

- Seattle remains effectively free of state-level athlete income tax for the 2026 tournament.

- Boston is a high-tax venue because Massachusetts’ 4 percent surtax pushes the top marginal rate at Gillette Stadium to 9 percent on income above the state’s millionaires’ threshold.

- Philadelphia requires complex income allocation because the city’s nonresident wage tax rate is scheduled to change on July 1, in the middle of the tournament.

- Mexico imposes a flat 25 percent tax on player compensation tied to matches in Mexico, even though it granted FIFA and its corporate affiliates a comprehensive tax exemption.

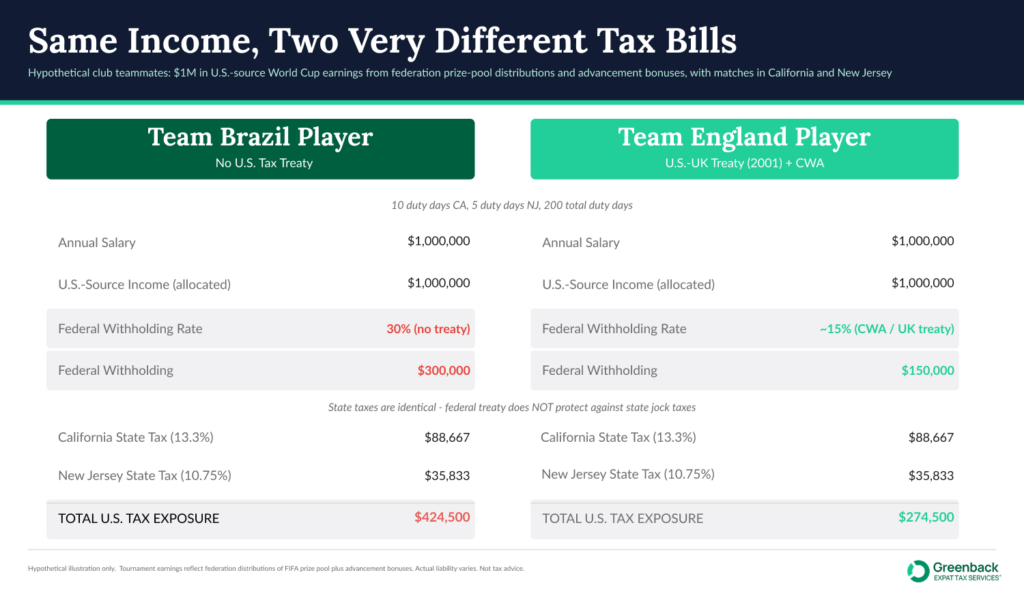

Same Tournament Earnings, Two Very Different Tax Bills

To see how these rules collide, consider two stars who each leave the 2026 World Cup with the same tournament earnings. Their pay is not a club salary. It is the share of FIFA prize money their federation distributes to players, plus performance and advancement bonuses tied to how far the team advances. For this illustration, assume each player walks away with $1,000,000 in U.S.-source tournament income from matches played in California and New Jersey.

The Brazilian player has no U.S. tax treaty to rely on. Income paid for independent personal services is generally subject to a 30 percent federal withholding on gross U.S.-source amounts, which would be roughly $300,000 before state taxes. After California and New Jersey jock taxes on the portion of income allocated to those venues, total U.S. exposure for this example lands near $424,500.

The England player can rely on the U.S.-U.K. income tax treaty, and the team can apply for a Central Withholding Agreement so that withholding is based on expected net income rather than gross receipts. The federal share of the bill drops meaningfully, while California and New Jersey jock taxes apply just the same. State protection ends at the federal line, so even with treaty relief, the U.K. player still owes the same state tax as the Brazil player.

Same prize-pool earnings. Same matches. Very different take-home pay.

How Article 17 Works and Where It Breaks Down

The United States maintains comprehensive income tax treaties with 68 countries. Modern agreements typically include a provision for athlete and entertainer income, usually found in Article 17 and titled “Artistes and Athletes.” Older treaties may use different numbering and titles, but the core objective remains the same.

The standard Article 17 structure consists of three parts. Paragraph 1 allows the U.S. to tax performance income earned on its soil while establishing a “de minimis” threshold for total earnings. Paragraph 2 addresses “star companies” by taxing income that flows to an entity controlled by the athlete. Finally, Paragraph 3 sometimes offers an exemption for visits funded by the athlete’s home government.

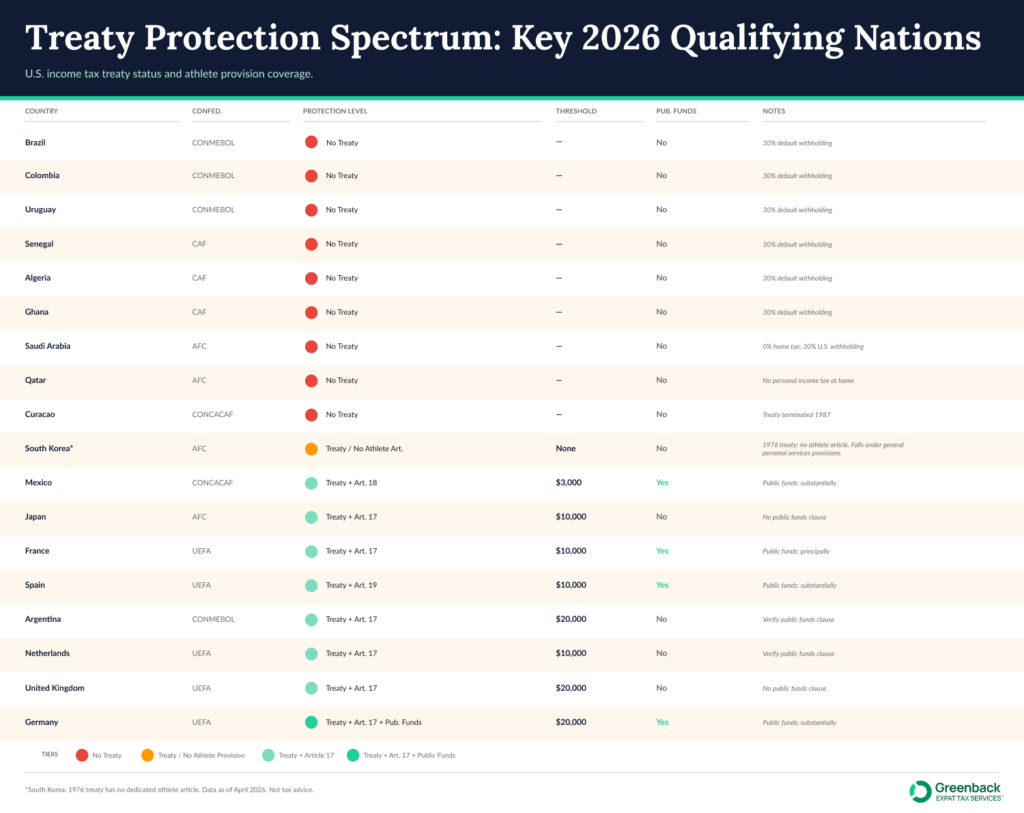

For the 2026 World Cup, we reviewed these provisions for eleven key nations. The variation in protection is far wider than most advisors would expect to encounter in a single tournament.

It also helps to keep two tools separate. A treaty determines whether the U.S. has the right to tax a player’s income at all and at what rate. A Central Withholding Agreement is a separate administrative contract with the IRS that adjusts how withholding is calculated during the tournament. Treaties shape the substantive tax bill. Central Withholding Agreements shape the cash-flow timing.

Exemption thresholds span a six-to-one range across the field

Exemption thresholds span a six-to-one range across the field. Mexico’s 1992 treaty sets the floor at just $3,000, which is functionally irrelevant for professional players whose match-day fees easily clear that amount. France, Spain, and Japan sit at $10,000, while Germany and the UK provide the highest protection at $20,000. While these exemptions are meaningful for mid-tier staff, they are merely a footnote for the stars generating the most revenue.

South Korea and Curaçao lack modern athlete protections

South Korea sits outside this standard spectrum. The 1976 treaty predates modern professional sports compensation and does not include a dedicated article for athletes. Instead, performance income falls under the treaty’s general independent and dependent personal services articles. That creates a less straightforward analysis than countries with a modern athlete article, because the question becomes whether the player has a U.S. “fixed base” or exceeds the day count in the treaty’s personal services provisions. The result is structural complexity rather than weaker protection.

Curaçaoan players face a similarly misunderstood situation. Although Curaçao is part of the Kingdom of the Netherlands, it is excluded from the 1992 U.S.–Netherlands treaty, which explicitly covers only the European Netherlands. This is a legacy of the 1987 termination of the treaty relationship with the Netherlands Antilles, aimed at preventing treaty shopping. Consequently, a Dutch player from Amsterdam can access treaty protections while their Curaçaoan teammate faces a flat 30 percent federal withholding.

Public funds standards vary based on specific qualifying language

The most significant variation in the treaty framework is the public funds exemption. Present in treaties with Germany, France, Spain, and Mexico, this clause can eliminate federal liability if the national team’s visit is supported by their home government.

However, the wording of these clauses creates different hurdles. The U.S.–Germany treaty requires the visit to be “substantially supported” by public funds, a standard that requires specific documentation rather than an automatic exemption. The French treaty uses the word “principally,” which implies a majority threshold and sets a higher bar for the same benefit. All else equal, a German player has a marginally easier path to this exemption than a French one.

Federal treaties provide no relief from state and local tax obligations

It is important to remember that U.S. income tax treaties are written to cover only federal taxes imposed under the Internal Revenue Code. They generally do not extend to state or local income taxes. Even if a German player successfully invokes a public funds exemption to pay zero federal tax, they can still owe New Jersey 10.75 percent at MetLife Stadium and California 13.3 percent at SoFi Stadium. The treaty acts as a shield against the IRS, but the protection ends at the state line.

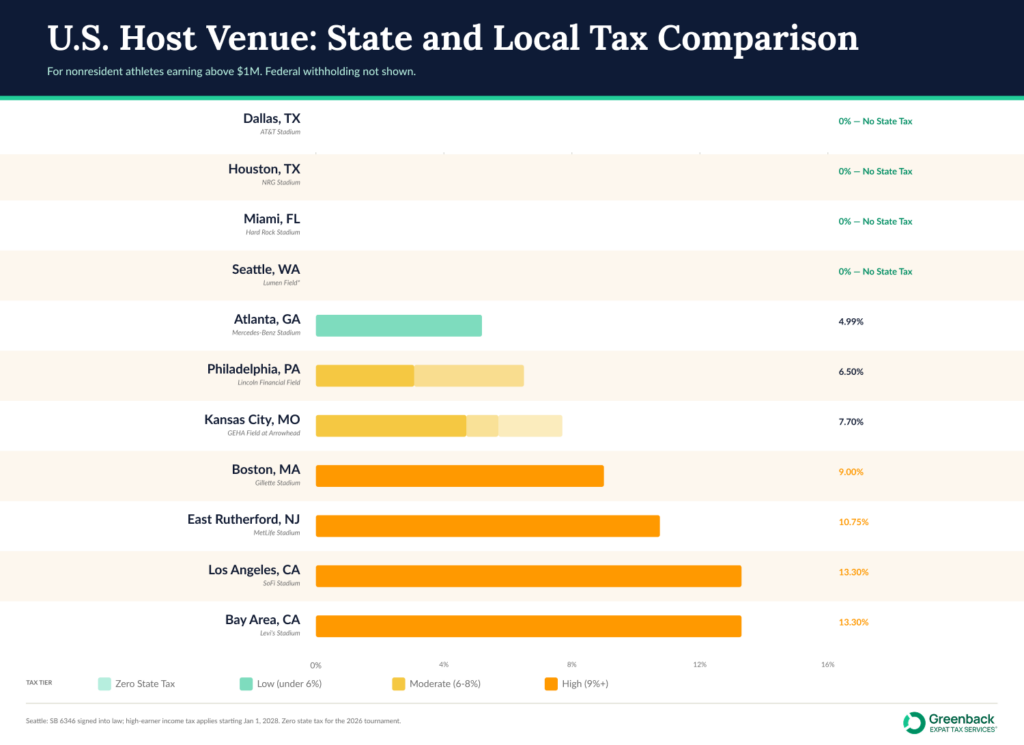

U.S. Host Venues: State and Local Tax Jurisdictions

The eleven U.S. host stadiums are divided into five distinct tax environments. For players and their advisors, venue assignment is as much a tax-planning variable as a scheduling detail.

Non-Taxing Jurisdictions (Texas and Florida)

AT&T Stadium in Dallas, NRG Stadium in Houston, and Hard Rock Stadium in Miami are located in states that do not have a broad personal income tax. Players at these venues face only federal withholding. For those from non-treaty countries, this still means a 30 percent hit, but there is no additional state or local tax layer and no state filing requirement.

Georgia Statutory Rates

Georgia’s 2026 individual income tax rate is 4.99 percent, retroactive to January 1, 2026, following Governor Kemp’s May 11, 2026, signing of House Bill 463. The legislation also sets a path for further annual rate reductions tied to state revenue triggers, but the 4.99 percent rate is the only rate that applies to the 2026 World Cup matches at Mercedes-Benz Stadium in Atlanta. Georgia does not impose local income taxes.

High-Tax Jurisdictions (CA, NJ, and MA)

Venues in California and New Jersey require the most intensive planning due to their high marginal rates on high earners.

- California: Matches at SoFi Stadium and Levi’s Stadium fall under a top marginal rate of 13.3 percent for income above $1 million.

- New Jersey: MetLife Stadium matches are subject to a 10.75 percent rate on income over $1 million.

- Massachusetts: Massachusetts now applies a 4 percent surtax on taxable income above the state’s millionaires’ threshold ($1,107,750 for 2026), in addition to its 5 percent flat rate. That brings the top marginal Massachusetts rate to 9 percent on income above the threshold, which places Gillette Stadium in the same high-tax category as Los Angeles and East Rutherford for star players.

Multi-Layered Tax Obligations (Missouri)

GEHA Field at Arrowhead has the most complex tax structure of any host venue. Missouri imposes a 4.7 percent flat income tax and a separate 2 percent gross withholding on nonresident athletes. Additionally, Kansas City levies its own 1 percent city earnings tax, which was recently renewed by voters in April 2026. Players here face three separate taxing authorities with a combined effective burden approaching 7 percent.

Philadelphia Fiscal Year Adjustments

Pennsylvania imposes a 3.07 percent flat tax, while Philadelphia adds a nonresident wage tax that is currently published at 3.43 percent. The local rate updates each July 1 as part of the city’s fiscal year. The July 4 Round of 16 match falls on the day Philadelphia publishes its new rate, so teams allocating income across late June and early July should plan against the 3.43 percent baseline and adjust once the city formally publishes the July 1, 2026, update.

Washington Legislative Status (Seattle)

In March 2026, Washington enacted SB 6346, a 9.9 percent tax on high-income individuals (including nonresident athletes) with Washington-source income above $1 million. Although SB 6346 is now law, the high-earner income tax applies starting January 1, 2028, so it does not affect 2026 World Cup matches in Seattle. Lumen Field remains a zero-state-tax venue for the tournament, although ongoing constitutional litigation and a potential referendum challenge could shape what happens in 2028 and beyond.

The North American Tax Stack: Canada and Mexico

While the U.S. framework is the most intricate part of the 2026 World Cup tax landscape, it is not the only one. Players with matches in Toronto, Vancouver, Guadalajara, Mexico City, or Monterrey face source-country tax obligations that differ structurally from U.S. jock-tax enforcement and from each other.

Canada: Source-Based Taxation with a Waiver Framework

Canada applies source-based withholding on income earned by nonresidents for services performed in the country, which includes athlete performance income. Under Regulation 105 of the Income Tax Act, payers must withhold 15 percent from amounts paid to nonresident athletes unless a waiver is obtained in advance

The Canada Revenue Agency (CRA) published a World Cup 2026 resource page outlining these obligations. Athletes from treaty-protected nations have two primary routes to relief: the Regulation 105 waiver (Form R105) for self-employed individuals, and the Regulation 102 waiver (Form R102-R) for employees.

Unlike the U.S. system, Canada’s framework is relatively navigable due to this clear, published waiver process. Players who apply on time can potentially eliminate or substantially reduce their withholding. Those who fail to apply, or who come from non-treaty countries, face a flat 15 percent withholding on gross Canadian income and a subsequent filing obligation to reconcile their actual tax debt.

Mexico: Gross Taxation and the FIFA Exemption Gap

Mexico’s approach is notable for the disparity between how it treats the tournament organizers versus the athletes. The 2026 Federal Revenue Law granted FIFA and its corporate affiliates a comprehensive exemption from Mexican federal taxes, creating a tax-free environment for the tournament’s corporate ecosystem.

Current Mexican guidance indicates the tournament exemption does not extend to remuneration and prizes received by players. Rule 9.4.3 of the 2026 Miscellaneous Tax Resolution clarifies that the FIFA exemption does not flow through to player compensation for participating in the competition.

Foreign players generally face a 25 percent tax on gross Mexican-source income with no permitted deductions. Mexico uses a proportional match approach for income attribution. For instance, if a player earns $1 million in total World Cup compensation and plays one of eight total tournament matches in Mexico, the country taxes one-eighth of that income ($125,000) at 25 percent.

The primary avenue for relief is Mexico’s treaty network, which may allow for reduced or eliminated tax burdens if specific formal requirements are met. While legal analysts have noted that excluding players from the broader FIFA exemption may exceed what Congress originally authorized, most advisors suggest complying and seeking treaty relief rather than relying on a legal challenge.

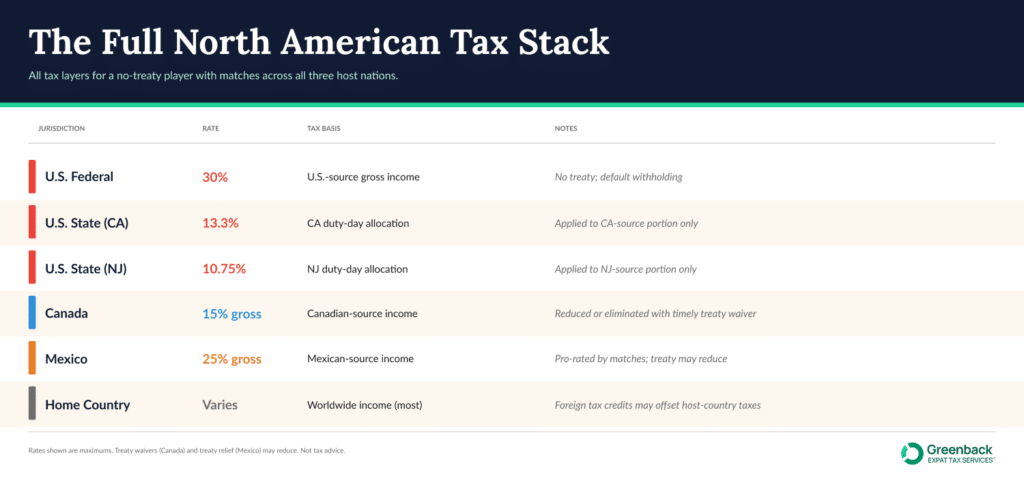

The Full Stack: Four Jurisdictions, One Tournament

For a player with matches in all three host nations, the cumulative tax burden and compliance requirements are significant. This “stack” involves separate filings and withholding mechanics for the home country, the U.S. federal government, U.S. states, and the source tax in either Canada or Mexico. In Canada, managing this requires proactive waiver applications submitted months before the opening match.

The following table illustrates the full tax stack for a hypothetical player earning $10 million annually, with match allocations across all three host countries and no treaty protections:

The interaction between these layers is where planning becomes vital. While foreign tax credits theoretically prevent double taxation, the mechanics are complex and require advisors to be engaged well in advance of the tournament.

The Regressive Nature of Tax Compliance

A mid-tier player from a non-treaty nation like Senegal, earning a relatively modest $400,000 annually, faces a clear tax calculation but a difficult execution process. If their team plays in California, New Jersey, and Texas, they owe a 30 percent federal withholding on U.S.-source income alongside California state taxes.

The difficulty lies in the mandatory compliance steps required to finalize these obligations:

- Obtaining an Individual Taxpayer Identification Number (ITIN).

- Filing IRS Form 1040-NR and various state nonresident returns.

- Potentially negotiating a Central Withholding Agreement.

- Assembling detailed documentation to support duty-day allocations.

At professional rates, this process typically costs between $5,000 and $15,000. For a player at this income level, whose actual state tax liability might only be $8,000 to $12,000, the cost of compliance can nearly equal the tax itself. While elite stars have the professional infrastructure to manage these hurdles, many mid-tier players and support staff from smaller nations do not, leaving them with a compliance burden that is disproportionately high relative to their earnings.

The Legal Limits on Jock Taxation

The compliance burden carries a constitutional dimension that advisors must consider. In February 2026, the Pennsylvania Supreme Court struck down Pittsburgh’s nonresident sports facility usage fee. This 3 percent levy, which applied specifically to visiting professional athletes, was ruled unconstitutional under the state’s Uniformity Clause. The court determined that a tax applying only to nonresidents, without a parallel burden on residents, cannot survive legal scrutiny in Pennsylvania.

This ruling draws a clear distinction for the 2026 tournament. Philadelphia’s nonresident wage tax remains defensible because it applies uniformly: residents pay 3.74 percent while nonresidents pay 3.43 percent. An ad hoc, nonresident-only levy does not meet this standard. For World Cup planning, players will only encounter jock taxes that have already survived such legal challenges.

The U.S. Citizen on a Foreign Squad

One category of player operates under entirely different logic: the U.S. citizen competing for a foreign national team. The United States taxes its citizens on worldwide income, regardless of where they reside or work. A dual national who lives in Spain and plays for the Spanish national team owes U.S. federal income tax on their entire global earnings, not just their World Cup income. The matches held on U.S. soil are merely the most visible portion of a tax obligation that exists year-round.

Foreign tax credits often mitigate double taxation, as taxes paid to Spain can reduce U.S. liability on that same income. However, these credits are often imperfect, and the compliance requirements are substantial. A dual national playing in a high tax venue like California or New Jersey may face a combination of state jock taxes and federal worldwide income tax that standard expatriate planning does not fully address. This situation is an acute version of the tax obligations millions of American expats navigate every day.

U.S. Athlete Tax Policy: Structural Revelations

The 2026 World Cup is the first major international tournament hosted under the current, large-scale jock tax infrastructure. The frictions emerging during this event are structural rather than incidental.

The de minimis thresholds in most Article 17 provisions were set during original negotiations and have not been adjusted for inflation. Mexico’s $3,000 threshold, established in 1992, represents only a fraction of its original purchasing power. Similarly, the South Korean treaty predates modern athlete compensation and has never been updated to include specific protections. While courts are beginning to impose constitutional limits on aggressive nonresident taxes, and states like Washington are moving toward sophisticated apportionment machinery, the federal treaty framework remains largely static.

These policy shifts do not change the immediate requirements for players arriving this summer. The relevant thresholds and venue rules are already on the books, and the window for Central Withholding Agreement applications and ITIN filings is narrowing. For players and advisors, the time to address these complexities is well before the opening match.

Tax Exemptions: Historical Precedents and 2026 Reality

A common question regarding the World Cup tax burden is whether host states could simply waive jock taxes for the tournament. While this is possible in principle, no such waivers are being granted in practice. In fact, some jurisdictions are moving in the opposite direction.

- Rather than easing obligations, New Jersey is considering additional revenue measures through bill S4111, which proposes a temporary tax increase during the tournament weeks at MetLife Stadium. The existing 10.75 percent income tax on athletes remains a fixed part of the state’s financial plan. California maintains a similar stance, with no pending legislation to exempt athletes from its 13.3 percent top marginal rate.

- Historical patterns show that tax exemptions almost exclusively benefit organizing bodies rather than individual athletes. For the 2026 tournament, Mexico has granted FIFA and its corporate affiliates a total income tax exemption, yet explicitly excludes foreign players from this benefit.

- Because FIFA did not secure a blanket U.S. federal exemption for the 48 participating nations, teams playing on American soil face a full stack of federal, state, and city taxes on their tournament income.

These policy shifts do not change the immediate requirements for players arriving this summer. The relevant thresholds and venue rules are already on the books, and the window for Central Withholding Agreement applications and ITIN filings is narrowing. For players and advisors, the time to address these complexities is well before the opening match.

Data Reference

Status current as of May 19, 2026

| Venue | City | State Tax | Top Rate | Local Tax | Notes |

| AT&T Stadium | Dallas, TX | None | 0% | None | Zero-tax venue |

| NRG Stadium | Houston, TX | None | 0% | None | Zero-tax venue |

| Hard Rock Stadium | Miami, FL | None | 0% | None | Zero-tax venue |

| Mercedes-Benz Stadium | Atlanta, GA | Yes | 4.99% | None | HB 463 signed May 11, 2026; rate retroactive to Jan 1, 2026 |

| SoFi Stadium | Los Angeles, CA | Yes | 13.3% (>$1M) | None | High-tax venue |

| Levi’s Stadium | Santa Clara, CA | Yes | 13.3% (>$1M) | None | High-tax venue |

| MetLife Stadium | East Rutherford, NJ | Yes | 10.75% (>$1M) | None | No NYC local tax applies |

| Gillette Stadium | Foxborough, MA | Yes | 9% top marginal (>$1,107,750) | None | 5% flat rate + 4% surtax on income above the millionaires’ threshold |

| GEHA Field | Kansas City, MO | Yes | 4.7% state | 1% city + 2% withholding | Three separate taxing layers |

| Lincoln Financial Field | Philadelphia, PA | Yes | 3.07% state | 3.43% nonresident (current); July 1, 2026 rate update pending official publication | July 4 Round of 16 falls on Philadelphia’s annual July 1 rate update |

| Lumen Field | Seattle, WA | None for 2026 | 0% for 2026 | None | SB 6346 signed into law; high-earner tax applies starting Jan 1, 2028 |

Treaty Status: Key Participating Nations

| Country | Treaty | Athlete Article | De Minimis Threshold | Public Funds Clause | Qualifying Language |

| Brazil | None | — | — | — | — |

| Senegal | None | — | — | — | — |

| Uruguay | None | — | — | — | — |

| Saudi Arabia | None | — | — | — | — |

| Mexico | 1992 | Art. 18 | $3,000 | Yes | “substantially supported” |

| France | 1994 | Art. 17 | $10,000 | Yes | “principally supported” |

| Spain | 1990 | Art. 19 | $10,000 | Yes | “substantially supported” |

| Japan | 2003 | Art. 17 | $10,000 | No | — |

| Germany | 1989 | Art. 17 | $20,000 | Yes | “substantially supported” |

| United Kingdom | 2001 | Art. 17 | $20,000 | No | — |

| South Korea | 1976 | None (Arts. 18/19) | None | No | — |

Sources and Methodology

Research conducted in May 2026. All URLs confirmed active at the time of publication.

U.S. Federal Tax — Treaties and Withholding

- IRS United States Income Tax Treaties A-to-Z — Primary source for confirming treaty existence or absence for all nations reviewed. irs.gov/businesses/international-businesses/united-states-income-tax-treaties-a-to-z

- U.S.–Germany Tax Convention (1989) — Article 17 (Artistes and Athletes), paragraphs 1–3; Article 2 (Taxes Covered). Treaty PDF via the IRS treaty documents page. Signed Bonn, August 29, 1989; effective January 1, 1990.

- U.S.–United Kingdom Tax Convention (2001) — Article 17. Treaty PDF via the IRS treaty documents page.

- U.S.–France Tax Convention (1994) — Article 17. Treaty PDF via the IRS treaty documents page.

- U.S.–Spain Tax Convention (1990) — Article 19. Treaty PDF via the IRS treaty documents page.

- U.S.–Japan Tax Convention (2003) — Article 17. Treaty PDF via the IRS treaty documents page.

- U.S.–Mexico Tax Convention (1992) — Article 18. Treaty PDF via the IRS treaty documents page.

- IRS Publication 515 — Withholding of Tax on Nonresident Aliens and Foreign Entities. irs.gov/publications/p515

- U.S.–Netherlands Tax Convention (1992) — Definition of “The Netherlands” as the European part only (Article 3). Treaty PDF via the IRS treaty documents page. Background on Netherlands Antilles treaty termination (1987).

U.S. State Tax Rates and Legislation

- California Franchise Tax Board — 2026 individual income tax rates. ftb.ca.gov

- New Jersey Division of Taxation — 2026 individual income tax rate schedule. nj.gov/treasury/taxation

- Massachusetts Department of Revenue — 2026 individual income tax rates; millionaire surtax (4%) on income above $1,107,750; Circular M withholding tables effective January 1, 2026. mass.gov/dor

- Georgia Department of Revenue — 2026 flat income tax rate (5.19%); HB 463 status. dor.georgia.gov/taxes/important-tax-updates

- Missouri Department of Revenue — 2026 flat income tax rate (4.7%); nonresident entertainer withholding (2%). dor.mo.gov

- Kansas City Revenue Division — City earnings tax rate (1%); voter renewal April 7, 2026; Form RD-109NR for nonresidents. kcmo.gov/city-hall/departments/finance/revenue-division

- Philadelphia Department of Revenue — Nonresident wage tax rate (3.43%, effective July 1, 2025–June 30, 2026); resident rate (3.74%). phila.gov/departments/department-of-revenue

- Washington State Legislature — SB 6346 — High-earner income tax (9.9% on income above $1M); effective January 1, 2028; athlete duty-day apportionment rules (§404). Signed March 30, 2026. leg.wa.gov

- Tax Foundation — “State Individual Income Tax Rates and Brackets, 2026.” taxfoundation.org/data/all/state/state-income-tax-rates-2026

- New Jersey Monitor — “Gov. Sherrill backs sales tax hike during World Cup matches as ‘tourism fee.'” April 16, 2026. newjerseymonitor.com/2026/04/16/governor-sales-tax-world-cup

- Morocco World News — “Morocco Among Few Nations Shielded From U.S. World Cup Tax Burden.” April 2026. moroccoworldnews.com/2026/04/287113/morocco-among-few-nations-shielded-from-us-world-cup-tax-burden

Legal Precedents

- NHLPA v. City of Pittsburgh — Pennsylvania Supreme Court, February 2026. The ruling struck down Pittsburgh’s nonresident sports facility usage fee as unconstitutional under Pennsylvania’s Uniformity Clause. The Tax Adviser, February 2026.

- Petter v. Washington — Klickitat County Superior Court. Constitutional challenge to SB 6346 filed April 9, 2026, by Citizen Action Defense Fund. No injunction granted as of April 2026.

- Heywood v. Hobbs — Washington Supreme Court granted accelerated review April 13, 2026, on whether voters can challenge SB 6346 via November 2026 ballot referendum.

Canada

- Canada Revenue Agency — Tax Resources for the FIFA World Cup 2026 — Primary source for Regulation 105 and 102 waiver framework, Form R105 and Form R102-R guidance, and filing timeline recommendations. canada.ca/en/revenue-agency/campaigns/tax-resources-fifa-world-cup-26.html

Mexico

- Basham, Ringe y Correa, S.C. — “Tax Implications in Mexico for Players of the 2026 World Cup, the Host Broadcaster and FIFA Service Providers.” January 22, 2026. Primary source for Rule 9.4.3 of the Miscellaneous Tax Resolution for 2026 and the 25% gross income tax rate for foreign players. basham.com.mx/en/tax-implications-in-mexico-for-players-of-the-2026-world-cup

- Mexico News Daily — “Did Mexico Grant FIFA a Full Tax Break for the World Cup?” November 12, 2025. mexiconewsdaily.com/sports/did-mexico-grant-fifa-a-full-tax-break-for-the-world-cup

World Cup Qualification and Match Schedule

- FIFA — 2026 World Cup Qualified Teams — Confirmed 48-team field. fifa.com/en/tournaments/mens/worldcup/canadamexicousa2026/teams

- ESPN — “2026 World Cup: How Every Nation Qualified” — Comprehensive qualification results including CAF playoff outcomes confirming Nigeria did not qualify; DR Congo and Iraq as final qualifiers. espn.com/soccer/story/_/id/40297462

- Wikipedia — 2026 FIFA World Cup Qualification (CAF) — CAF group results confirming Senegal as Group B winner; South Africa as Group C winner. en.wikipedia.org/wiki/2026_FIFA_World_Cup_qualification_(CAF)

- 2026 World Cup Match Schedule — Lincoln Financial Field — Official match dates used for Philadelphia fiscal year analysis. Via FIFA/official tournament sources.

Methodology Note

Tax rates, treaty provisions, and legislative status were verified directly from primary sources (government websites, official legislative records, and treaty texts) between February and May 2026. Where rates were pending legislative action at the time of publication (Georgia HB 463), the confirmed statutory floor is used with the pending change noted. Player tax scenarios are hypothetical illustrations using published rates and simplified duty-day calculations; they are not intended as tax advice for any specific individual.

Greenback Expat Tax Services specializes in U.S. tax preparation and advisory services for American citizens and nonresidents with cross-border income.