Form 8843 for Visa Holders Explained: Exempt Individual Statement

- Who Must File Form 8843?

- What Is the Substantial Presence Test?

- Do I Need Form 8843 If I Had No Income?

- How Do I Fill Out Form 8843?

- What If I Have Dependents?

- When Is Form 8843 Due?

- How Do I File Form 8843?

- What Happens If I Don't File Form 8843?

- Can I File Form 8843 for Previous Years?

- What About Tax Treaties?

- Form 8843 and Dual-Status Filing

- Why Choose Greenback for Foreign National Tax Services?

- Related Resources

According to IRS regulations, all foreign nationals in F, J, M, or Q visa status must file Form 8843 annually to document their exempt individual status for the Substantial Presence Test, even if they earned no U.S. income during the year. This requirement applies to students, scholars, trainees, teachers, and their spouses and dependents who are nonresident aliens for U.S. tax purposes.

Form 8843 is not an income tax return. It’s an informational statement that explains why you can exclude days of U.S. presence from the Substantial Presence Test, allowing you to remain classified as a nonresident alien for tax purposes. This classification is crucial because it determines which tax forms you file and how your income is taxed.

The form must be filed by every nonresident individual in F, J, M, or Q status who was present in the U.S. at any point during the calendar year, including spouses and dependent children of any age. Each family member must file their own separate Form 8843, even infants and young children who cannot sign their own forms.

On an F, J, M, or Q Visa? You Likely Need Form 8843

Who Must File Form 8843?

You must file Form 8843 if all three conditions apply:

1. You were present in the U.S. under F, J, M, or Q visa status

- F-1 and F-2 visa holders: Students and their spouses/dependents

- J-1 and J-2 visa holders: Exchange visitors, scholars, researchers, teachers, trainees, and their spouses/dependents

- M-1 and M-2 visa holders: Vocational students and their spouses/dependents

- Q visa holders: Cultural exchange visitors

2. You are a nonresident alien for U.S. tax purposes

Generally, you’re a nonresident alien if:

- F or J students: Present in the U.S. for 5 years or less

- J scholars/teachers/researchers: Present in the U.S. for 2 out of the last 6 years or less

- You don’t pass the Substantial Presence Test

3. You were in the U.S. at any point during the calendar year

Even if you were only present for one day, you must file Form 8843 for that year.

This filing requirement exists whether or not you earned any U.S. income and regardless of whether you’re required to file a U.S. tax return.

What Is the Substantial Presence Test?

The Substantial Presence Test is the IRS formula for determining if a foreign national should be treated as a U.S. resident for tax purposes based on physical days present in the United States.

The Test Formula:

You’re considered a U.S. resident if:

- You were in the U.S. for at least 31 days during the current year, AND

- The sum of your weighted days over three years equals or exceeds 183 days:

- All days in the current year (100%)

- 1/3 of days in the year 1 before the current year

- 1/6 of days in year 2 before the current year

Why Form 8843 Matters:

Certain visa categories qualify as “exempt individuals” who can exclude their days of U.S. presence from this calculation. Form 8843 is your official statement claiming this exemption, which allows you to remain a nonresident alien even if you’ve been in the U.S. for multiple years.

Exempt Individual Categories:

- Students (F, J, M, Q): Exempt for up to 5 calendar years

- Teachers and trainees (J, Q): Exempt for up to 2 out of 6 calendar years

- Professional athletes: Temporarily in the U.S. for charitable sports events

- Individuals with medical conditions: Unable to leave due to medical issues

Without filing Form 8843, you cannot claim these exclusions, potentially making you a resident alien subject to different (and often more complex) tax requirements.

Do I Need Form 8843 If I Had No Income?

Yes, Form 8843 is required even if you had zero U.S. income during the year.

Many foreign nationals mistakenly believe they don’t need to file anything with the IRS if they didn’t earn money. This is incorrect. Form 8843 is not about reporting income—it’s about documenting your immigration status and days of presence to maintain your nonresident classification.

Common No-Income Scenarios Requiring Form 8843:

- International students supported entirely by foreign scholarships, family funds, or savings

- F-2 or J-2 spouses and dependents are not authorized to work in the U.S.

- Students who arrived late in the year and didn’t start working

- Visiting scholars whose salaries were paid by foreign institutions

- Infant or minor children of F-1 or J-1 visa holders

If you had U.S. income, you’ll file both Form 8843 AND a tax return (Form 1040-NR). If you had no income, you would only file Form 8843 by itself.

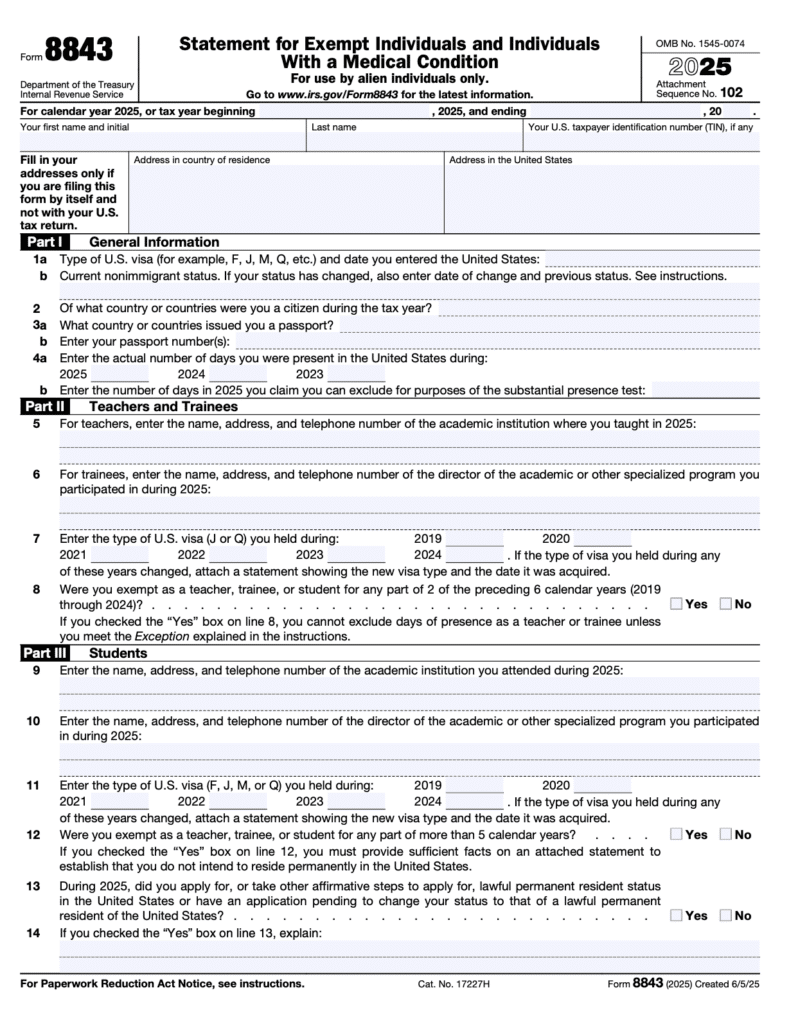

How Do I Fill Out Form 8843?

Form 8843 has multiple parts, but not all sections apply to every filer. Here’s your step-by-step guide:

Top Section: Personal Information

- Name: Your full name as it appears on your passport

- U.S. Taxpayer Identification Number: Your SSN or ITIN if you have one. If you don’t have either, leave this blank (you don’t need one just to file Form 8843)

- Address in Country of Residence: Your permanent home country address

- Address in the United States: Your current U.S. address

Part I: General Information (Lines 1-4)

- Line 1a: Enter your visa type (F-1, J-2, etc.) and the date you most recently entered the U.S. on that visa

- Line 1b: Your current nonimmigrant status as of December 31 of the tax year. Usually, this is the same as 1a unless you changed status while in the U.S.

- Line 2: Check “Yes” if you changed your non-immigrant status while in the U.S.; otherwise, check “No”

- Line 3: Number of days in the U.S. during the year that you’re claiming you can exclude

- Line 4a: Total days present in the U.S. during the calendar year (count every day, including arrival and departure days)

- Line 4b: Days present in the U.S., specifically in F, J, M, or Q status

Part II: Teachers and Trainees (J or Q visa only)

Complete this section only if you’re a J-1 or Q visa holder present in the U.S. as a teacher or trainee.

- Line 5: Name, address, and phone number of the academic institution or program

- Line 6: Name, address, and phone number of the program director or academic supervisor

- Line 7: Indicate which years you held J or Q status (current year, last 6 years)

- Line 8: Indicate if you were exempt as a teacher, trainee, or student for any part of 2 of the preceding 6 calendar years

Students (F-1, M-1) and student dependents (F-2, J-2): Skip Part II entirely.

Part III: Students (F, J, M, Q visa)

Complete this section if you’re a student (F-1, M-1, J-1 student) or student dependent (F-2, J-2).

- Line 9: Name and address of your U.S. educational institution

- Line 10: Name of the school official or program director to contact

Teachers, trainees, and researchers: Skip Part III.

Part IV: Professional Athletes

Leave blank unless you’re a professional athlete temporarily in the U.S. for a charitable sports event. This section rarely applies to F, J, M, or Q visa holders.

Signature and Date

Sign and date the form at the bottom. If a dependent child is too young to sign, a parent or guardian signs the child’s name followed by “By [parent signature], parent for minor child.”

Form 8843 Helps Preserve Your Nonresident Status

What If I Have Dependents?

Each family member must file their own separate Form 8843.

This means:

- Your F-2 or J-2 spouse files their own Form 8843

- Each F-2 or J-2 dependent child files their own Form 8843, regardless of age

- Each form must be mailed in a separate envelope—do not combine multiple family members’ forms

For Dependent Forms:

When filling out Form 8843 for a dependent (spouse or child), most sections are completed the same way, except:

Part III (Students) – Dependent Modifications:

Instead of listing your own school, dependents should write:

- Line 9: “Spouse/Dependent of student attending [University Name], [Address]”

- Line 10: “Spouse/Dependent of student whose program director is [Name], [Office]”

For very young children: Parents or guardians sign the form for them using the notation: “[Child’s name], by [Parent signature], parent for minor child.”

When Is Form 8843 Due?

The filing deadline depends on whether you have U.S. income:

If you’re filing Form 8843 WITH a tax return (Form 1040-NR):

- April 15, 2026 (for 2025 tax year)

- Form 8843 is attached to your tax return

If you’re filing Form 8843 ALONE (no U.S. income, no tax return):

- June 15, 2026 (for 2025 tax year)

- You have an automatic two-month extension

Extensions: If you need more time, you can request an extension to October 15, 2026, using Form 4868, but this applies only if you’re also filing a tax return. The June 15 deadline for standalone Form 8843 filers is already an automatic extension.

Filing Late: If you missed previous years, file those Form 8843s as soon as possible. Attach one Form 8843 for each year you were present in the U.S. Mail them all together to the IRS.

How Do I File Form 8843?

Form 8843 must be filed by mail—the IRS does not accept electronic filing.

If filing Form 8843 with a tax return (Form 1040-NR):

Attach Form 8843 to the back of your tax return and mail both together to the address shown in the Form 1040-NR instructions for your state.

If filing Form 8843 alone (no income, no tax return):

Mail to: Department of the Treasury Internal Revenue Service Center Austin, TX 73301-0215

Mailing Tips:

- Use certified mail with tracking and delivery confirmation

- Keep a copy of your completed form for your records (retain for at least 4 years)

- If filing for multiple family members, each person’s Form 8843 must be in a separate envelope

- The IRS does not send confirmation of receipt, so your mailing receipt is your only proof

Do I Need an SSN or ITIN?

No, you generally don’t need a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) just to file Form 8843. If you’ve been assigned one previously, you must include it on the form. If not, leave that field blank.

Exception: If you’re claimed as a dependent on someone else’s U.S. tax return, you must have an SSN or ITIN.

What Happens If I Don’t File Form 8843?

Failing to file Form 8843 has serious consequences:

You Cannot Exclude Your Days:

Without Form 8843, you cannot exclude your days of U.S. presence from the Substantial Presence Test. This means:

- You may be classified as a U.S. resident alien

- You’ll be subject to resident alien tax rules

- You’ll need to report worldwide income on Form 1040 instead of Form 1040-NR

- You may owe significantly more in U.S. taxes

Immigration Consequences:

The IRS shares information with U.S. Citizenship and Immigration Services (USCIS). Non-compliance with tax filing requirements can:

- Affect future visa applications or renewals

- Create issues when applying for Optional Practical Training (OPT) or Curricular Practical Training (CPT)

- Impact applications for change of status or adjustment of status to permanent residence

- Cause complications during visa interviews at U.S. embassies abroad

No Direct Penalty, But…

While there’s no specific monetary penalty for not filing Form 8843, the consequences of being incorrectly classified as a resident alien can be far more expensive than any penalty would be. Residents pay tax on worldwide income and cannot claim many treaty benefits available to nonresidents.

Can I File Form 8843 for Previous Years?

Yes. If you missed filing Form 8843 in prior years, you should file delinquent forms as soon as possible.

How to File Late Form 8843s:

- Download Form 8843 for each year you missed from the IRS Prior Year Forms page

- Complete one form for each year you were in the U.S.

- Mail all forms together to the Austin, TX address listed above

- Consider including a brief cover letter explaining that you were unaware of the filing requirement

Filing late is better than not filing at all. The IRS allows nonresidents to correct prior-year filings, and proactivity demonstrates good-faith compliance.

What About Tax Treaties?

The U.S. has tax treaties with over 60 countries that may provide additional benefits to foreign nationals. Common treaty benefits include:

- Exemptions or reduced tax rates on scholarship income

- Teacher and researcher income exemptions (typically for 2 years)

- Specific exemptions for students from treaty countries

- Reduced withholding rates on certain types of income

If you’re claiming treaty benefits, you may need to file Form 8833 in addition to Form 8843 and your tax return (if applicable).

Treaty benefits do not eliminate the Form 8843 requirement. You must still file Form 8843 to document your exempt individual status, even if a treaty provides additional tax relief.

Form 8843 and Dual-Status Filing

Some foreign nationals transition from nonresident to resident alien status during the year (or vice versa). This creates a “dual-status” filing year where you’re a nonresident for part of the year and a resident for the rest.

Dual-status situations occur when:

- You exceed the 5-year exemption as an F or J student

- You obtain a green card during the year

- You pass the Substantial Presence Test mid-year

If you’re dual-status, you may need to file both:

- Statement for nonresident portion: Form 8843 documenting your exempt period

- Tax return for the resident portion: Form 1040 for the resident period

Filing a dual-status return for the first time? If you moved to the U.S. midyear and need help determining your residency start date, splitting income correctly between periods, or deciding whether to make the nonresident spouse election, our team specializes in tax filing for foreign nationals and dual-status filers. We’ll handle the complex allocation rules and ensure you’re positioned correctly from day one.

Why Choose Greenback for Foreign National Tax Services?

Greenback is an American company founded in 2009 by U.S. expats for expats. While we’re best known for helping Americans abroad, we also help foreign nationals with their U.S. tax obligations, including Form 8843, Form 1040-NR, and dual-status situations.

Our team of CPAs and Enrolled Agents understands the unique challenges international students, scholars, and their families face. We have the knowledge and patience to help you handle the complicated U.S. tax system correctly.

No matter how late, messy, or complex your situation may be, we can help. You’ll have peace of mind knowing that your tax filings were done right.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on tax filing for foreign nationals or working with Greenback, contact our Customer Champions.

Make Sure Form 8843 Is Filed Correctly

This article provides general information about Form 8843 for foreign nationals in F, J, M, and Q visa status. Tax laws and immigration regulations change frequently, and individual circumstances vary. Please consult with a qualified tax professional for advice specific to your situation.

Related Resources

- Form 1040-NR: Nonresident Alien Tax Return Guide

- Substantial Presence Test: Complete Guide

- Resident vs. Nonresident Alien: Tax Status Explained

- Form 8833: U.S. Tax Treaties Explained

- Dual-Status Tax Filing for Foreign Nationals

- Tax Services for Foreign Nationals

- U.S. Taxes for Foreigners: Complete Guide

- Visa Taxation Chart: Which Forms Do You Need?