Schedule E (Form 1040): Reporting Supplemental Income and Loss

- What Types of Income Does Schedule E Cover?

- How Is Schedule E Structured?

- What Expenses Can You Deduct on Schedule E?

- What Are the Passive Activity Loss Rules for Schedule E?

- How Do Expats Report Foreign Rental Income on Schedule E?

- What Other Forms Might You Need to File With Schedule E?

- How Does Schedule E Flow Into Your Tax Return?

- Schedule E Checklist: What to Gather Before You File

- Frequently Asked Questions About Schedule E

- Related Resources

Schedule E (Form 1040) is the IRS form you use to report supplemental income and loss, including rental real estate, royalties, partnerships, S corporations, estates, trusts, and REMICs. You attach it to your Form 1040 any time you receive income from these sources. If you report a rental loss, the IRS allows you to deduct up to $25,000 against your other income under the passive activity special allowance, though this phases out once your modified adjusted gross income (MAGI) exceeds $100,000 (IRS: Schedule E instructions).

You need to file Schedule E if any of the following apply:

- Rental real estate: you collect rent from residential or commercial property, whether located in the U.S. or abroad

- Royalties: you receive payments from natural resources, patents, copyrights, or other intellectual property

- Partnership or S corporation income: you receive a Schedule K-1 reporting your share of income or loss from a pass-through entity

- Estate or trust distributions: you are a beneficiary receiving allocated income from a fiduciary entity

Rental Income, Royalties, or K-1s? Schedule E Is Where They Go.

Below, you will find a breakdown of each income type, deductible expenses, passive activity loss rules, foreign rental reporting requirements, and the additional forms you may need to file alongside Schedule E.

What Types of Income Does Schedule E Cover?

Schedule E covers a broad range of supplemental income types that do not fall under wages, salaries, or self-employment income (which are reported on Schedule C instead). The key distinction is that Schedule E income is generally passive, meaning you are not materially participating in the day-to-day operations that generate it.

The main categories include:

- Rental real estate income: rent collected from tenants on properties you own, including single-family homes, apartments, condos, and commercial buildings

- Royalty income: payments from natural resource extraction (oil, gas, minerals) or licensing of intellectual property such as patents, copyrights, and trademarks

- Partnership income or loss: your distributive share from a general or limited partnership, reported to you on Schedule K-1 (Form 1065)

- S corporation income or loss: your pro-rata share of income from an S corporation, also reported on a Schedule K-1 (Form 1120-S)

- Estate and trust income: distributions or allocated income from estates or trusts, reported on Schedule K-1 (Form 1041)

- REMIC residual interests: income from residual interests in real estate mortgage investment conduits

Each of these income types has its own section on the form. The totals flow to Schedule 1 (Form 1040), line 5, and then to your Form 1040.

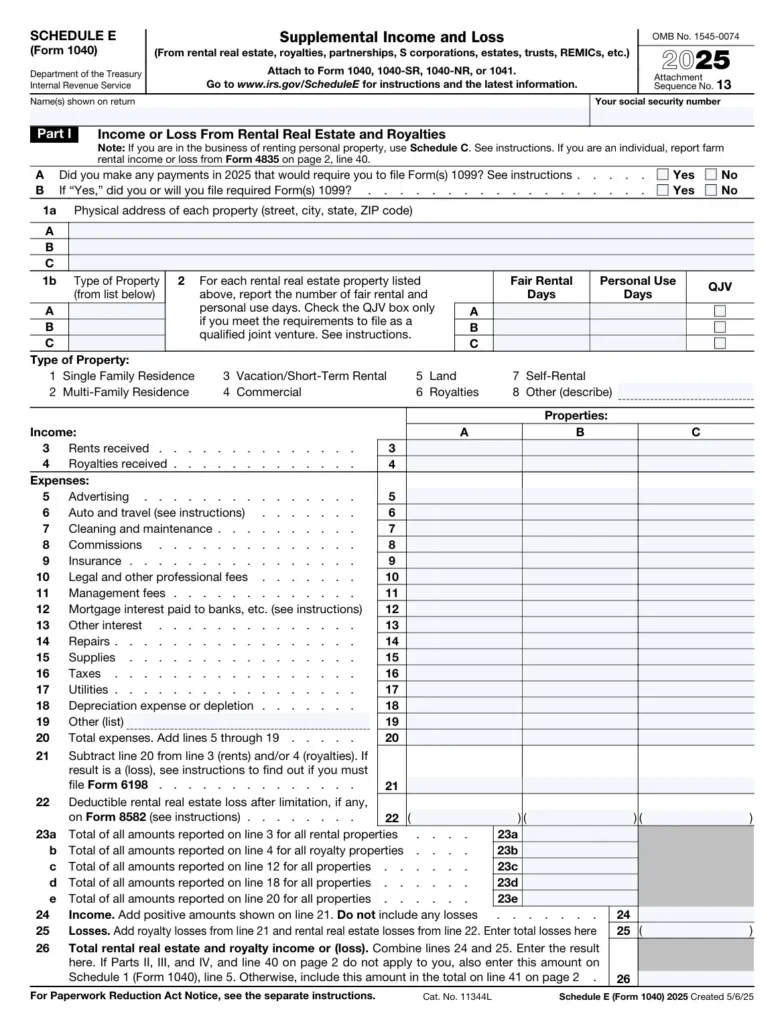

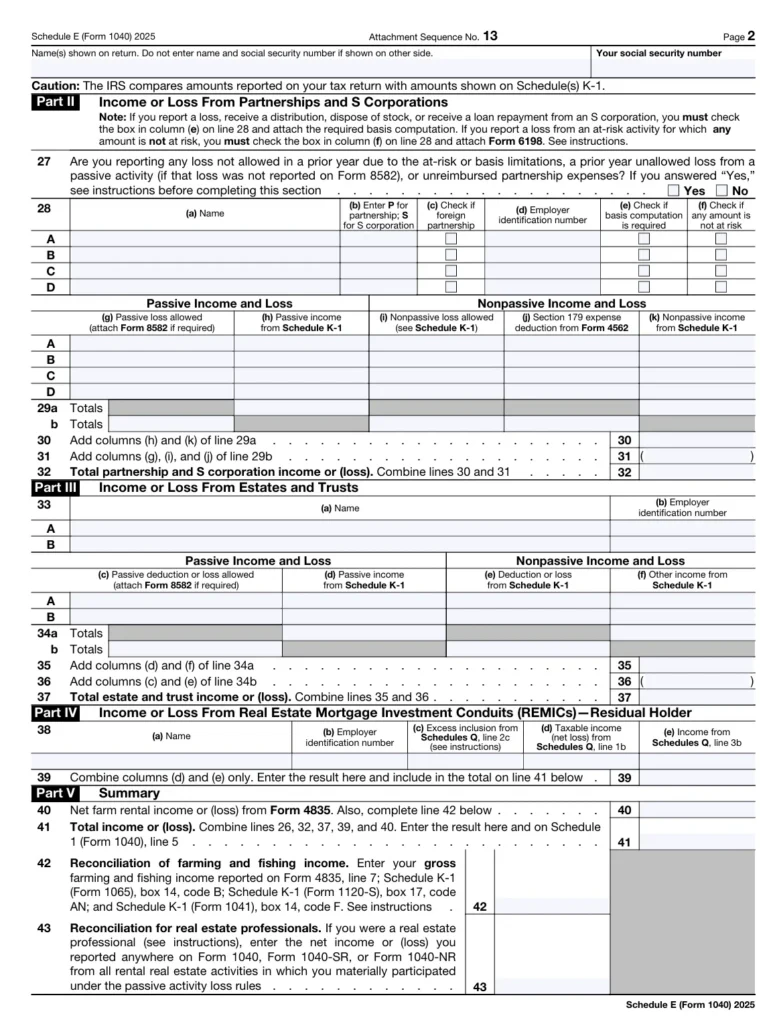

How Is Schedule E Structured?

Schedule E is divided into five parts, each covering a different type of income. Here is a quick overview of how the form is organized:

| Part | What It Covers | Key Details |

|---|---|---|

| Part I | Rental real estate and royalties | Report up to three properties per form; attach additional copies for more |

| Part II | Partnerships and S corporations | Report income/loss from K-1s (Form 1065 and Form 1120-S) |

| Part III | Estates and trusts | Report income/loss from K-1s (Form 1041) |

| Part IV | Real estate mortgage investment conduits (REMICs) | Report taxable income from residual interests |

| Part V | Summary | Combines totals from all parts and carries to Schedule 1 |

If you have more than three rental properties, you can attach as many copies of Part I as needed. Just make sure only one copy includes the Part V summary totals.

What Expenses Can You Deduct on Schedule E?

Part I of Schedule E includes a dedicated section for deducting expenses tied to your rental properties. These deductions reduce your taxable rental income dollar for dollar, so tracking them carefully can make a significant difference on your return.

Common deductible expenses include:

- Mortgage interest: interest paid on loans used to purchase or improve the rental property

- Property taxes: state, local, and (for properties abroad) foreign property taxes paid

- Repairs and maintenance: routine upkeep like fixing a leaky roof, repainting, or replacing broken fixtures

- Insurance: premiums for property, liability, and landlord insurance policies

- Depreciation: the IRS allows you to recover the cost of your rental property over time (27.5 years for U.S. residential property, or 30 years for foreign residential property)

- Property management fees: amounts paid to a property manager or management company

- Utilities and advertising: costs you pay for tenant-occupied utilities or to advertise vacancies

- Travel expenses: travel to your rental property for maintenance or management, using the standard mileage rate of $0.70 per mile for 2025

For partnership, S corporation, and trust income reported in Parts II through IV, your deductions are typically already factored into the K-1 figures you receive. You generally report the net amounts from your K-1 rather than listing individual expenses.

What Are the Passive Activity Loss Rules for Schedule E?

One of the most important rules affecting Schedule E filers is the passive activity loss limitation. Under IRS Publication 925, rental activities are generally treated as passive, meaning losses from rental properties can only offset other passive income, not wages or investment earnings.

There is an important exception. If you actively participated in a rental real estate activity, you may be able to deduct up to $25,000 in rental losses against your nonpassive income. This $25,000 special allowance phases out as your modified adjusted gross income (MAGI) rises:

| Filing Status | Allowance Starts | Phaseout Begins | Allowance Eliminated |

|---|---|---|---|

| Single or Head of Household | $25,000 | MAGI over $100,000 | MAGI of $150,000 |

| Married Filing Jointly | $25,000 | MAGI over $100,000 | MAGI of $150,000 |

| Married Filing Separately (lived apart all year) | $12,500 | MAGI over $50,000 | MAGI of $75,000 |

The phaseout reduces the allowance by $0.50 for every $1 of MAGI above the threshold. If you and your spouse lived together at any point during the year and file separately, you cannot use this allowance at all.

Real estate professional exception: If you qualify as a real estate professional, your rental activities are not subject to passive activity loss rules. To qualify, you must perform more than 750 hours of services in real property trades or businesses during the year, and more than half of your total personal services must be in those real estate activities. If you meet both tests, you can deduct rental losses without limitation against your other income.

Losses you cannot deduct in the current year are not lost. They carry forward to future years and can offset passive income or be fully deducted when you dispose of the property in a taxable transaction.

How Do Expats Report Foreign Rental Income on Schedule E?

If you own rental property outside the United States, you report that income on Schedule E, Part I, just as you would for a U.S. property. The IRS requires all U.S. citizens and Green Card holders to report worldwide income, including foreign rental income. You will need to convert all amounts to U.S. dollars, use a longer depreciation timeline (30 years instead of 27.5), and keep in mind that the Foreign Earned Income Exclusion does not apply to rental income because it is passive, not earned. If you pay taxes on that rental income to a foreign government, the Foreign Tax Credit may help reduce your U.S. tax bill.

For a full walkthrough of deductions, depreciation rules, and currency conversion for foreign properties, see our foreign rental income guide.

What Other Forms Might You Need to File With Schedule E?

Depending on your situation, you may need to attach or reference several additional forms when filing Schedule E:

- Form 8582 (Passive Activity Loss Limitations): required if you have passive activity losses that exceed your passive income for the year

- Form 4562 (Depreciation and Amortization): required if you are claiming depreciation on a rental property for the first time or claiming amortization

- Form 461 (Limitation on Business Losses): required if your total business losses exceed the threshold ($313,000 for single filers or $626,000 for joint filers for the 2025 tax year), which limits the excess business loss you can claim

- Schedule K-1: You do not file this form yourself, but you need the K-1s issued by your partnerships, S corporations, or trusts to complete Parts II and III of Schedule E

- Form 8865 (Return of U.S. Persons With Respect to Certain Foreign Partnerships): required if you hold interests in a foreign partnership

If you are claiming the S corporation basis limitation, you must check the box in column (e) on line 28 and attach your basis computation to your return.

How Does Schedule E Flow Into Your Tax Return?

Schedule E does not stand on its own. The net income or loss from all five parts combines on the Part V summary line and then flows to Schedule 1 (Form 1040), line 5. From there, it is included in your total income on Form 1040, line 8.

Here is a simplified example of how this works:

Suppose you own a rental property that generated $18,000 in gross rental income and had $12,500 in deductible expenses (including $5,000 in depreciation). Your net rental income on Schedule E, Part I, would be $5,500. That $5,500 flows to Schedule 1, then to your Form 1040, where it is taxed at your ordinary income tax rates.

If your property produced a loss instead, the passive activity rules described above determine how much of that loss you can deduct in the current year.

Schedule E Checklist: What to Gather Before You File

Before sitting down to complete Schedule E, make sure you have:

- Rental income records (lease agreements, bank statements showing rent deposits)

- Expense receipts for all deductible items (mortgage statements, repair invoices, insurance bills)

- Depreciation schedules for each property

- All Schedule K-1 forms from partnerships, S corporations, estates, and trusts

- Foreign property records converted to U.S. dollars, if applicable

- Records of personal use days vs. rental days for each property

Ready to Get Your Supplemental Income Reported Correctly?

Frequently Asked Questions About Schedule E

No, rental income reported on Schedule E is generally not subject to self-employment tax. This is one of the key differences between Schedule E and Schedule C. Self-employment tax (15.3% for Social Security and Medicare) applies to income from a trade or business reported on Schedule C, but passive rental income on Schedule E is exempt from it. Partnership income reported on Schedule E may include self-employment earnings, depending on the type of partnership and your level of involvement. Your Schedule K-1 will indicate which portion, if any, is subject to self-employment tax.

Schedule E is for passive rental income where you are not providing substantial services to your tenants. Schedule C is for rental activity that qualifies as a trade or business, typically because you provide hotel-like services such as daily cleaning, fresh linens, meals, or concierge-type amenities. Most traditional landlords file Schedule E. If you operate a short-term rental or vacation property and offer services that go beyond basic maintenance, utilities, and trash collection, the IRS may require you to report that income on Schedule C instead. The distinction matters because Schedule C income is subject to self-employment tax, while Schedule E income typically is not.

It depends on the services you provide. If you rent out a vacation property but do not offer substantial services to guests, you report the income on Schedule E. You will need to track the number of days the property was rented at fair market value, as well as the number of days you or your family personally used it. If personal use exceeds the greater of 14 days or 10% of the rental days, the IRS considers it a personal residence and limits the deductions you can claim. If you provide substantial services (similar to those of a hotel), you report them on Schedule C rather than Schedule E.

If you own rental property through a single-member LLC, you are treated as a disregarded entity for federal tax purposes. That means you report the rental income and expenses directly on Schedule E, Part I of your personal Form 1040, just as if you owned the property individually. If the LLC has multiple members, it is treated as a partnership and must file Form 1065. You would then receive a Schedule K-1 and report your share of the income on Schedule E, Part II.

Yes, you should still file Schedule E if you had deductible expenses during a period when the property was available for rent but not occupied. The IRS allows you to deduct expenses such as mortgage interest, property taxes, insurance, and maintenance for the time the property was actively listed and available, even if you had no rental income during that period. However, if the property was not available for rent (for example, undergoing major renovation or held for personal use), those expenses may not be deductible as rental expenses.

Disallowed passive activity losses are not lost permanently. They are suspended and carried forward to future tax years. You can use them to offset passive income in later years, or deduct the full accumulated loss when you dispose of the property in a fully taxable transaction to an unrelated party. The at-risk rules may further limit your losses to the amount you have financially at risk in the activity, so it is important to track both your passive loss carryforward and your at-risk basis each year.

Yes, depreciation is one of the largest deductions available to rental property owners on Schedule E. The IRS requires you to depreciate the cost of the building (not the land) over its useful life: 27.5 years for U.S. residential rental property, 39 years for U.S. commercial property, and 30 years for foreign residential rental property. You must use Form 4562 to report depreciation in the first year you place the property in service. In subsequent years, you can report it directly on Schedule E, provided no changes have been made to the depreciation method.

Tax rules are complex and change frequently. This article provides general information and is not a substitute for professional tax advice. For guidance specific to your situation, consult a qualified tax professional.

Related Resources

- Foreign Rental Income Tax: How to Report and Reduce Your U.S. Tax Bill

- Schedule K-1 (Form 1065) for Expats Explained

- Foreign Tax Credit Guide: How to Reduce U.S. Expat Taxes

- Form 1116 for Expats: How to Claim the Foreign Tax Credit

- Foreign Earned Income Exclusion (FEIE) Explained

- Schedule C for Expats: Self-Employment and Business Income

- Schedule 1 (Form 1040) for U.S. Expats

- U.S. Expat Tax Deductions and Credits

- Form 8865 for Expats: Reporting Foreign Partnerships

- U.S. Tax Filing Deadlines for Americans Living Abroad