Form 8880 for Expats Explained: The Retirement Saver’s Credit

- What Is Form 8880?

- Why Does This Matter for Me as an Expat?

- Do I Qualify for the Saver's Credit?

- How Much Credit Can I Get?

- What Retirement Accounts Qualify?

- Will Past Withdrawals Affect My Credit?

- How Do I Complete Form 8880?

- How Does the FEIE Affect My Saver's Credit?

- Can I Use Both U.S. and Foreign Retirement Plans?

- What If I'm Behind on Filing?

- What Mistakes Should I Avoid?

- How Can I Maximize My Benefit?

- What's Changing in 2027?

- What Are My Next Steps?

- Related Resources

The IRS announced that income limits for the Saver’s Credit increased to $79,000 for married couples filing jointly and $39,500 for singles, meaning more American expats can now claim up to $1,000 ($2,000 if married filing jointly) in tax credits simply for contributing to retirement accounts. Form 8880 lets you claim this Retirement Savings Contributions Credit, and as an American living abroad, you can still qualify even while overseas.

The bottom line: If your adjusted gross income falls below these thresholds, contributing to retirement accounts could earn you a direct dollar-for-dollar tax credit while building your future financial security. Most expats who use the Foreign Earned Income Exclusion will likely qualify because your excluded income doesn’t count toward these AGI limits.

What Is Form 8880?

Form 8880 is used by individuals to figure the amount, if any, of their retirement savings contributions credit (also known as the Saver’s Credit). This IRS form calculates a tax credit designed to encourage low- and moderate-income taxpayers to save for retirement.

Unlike a tax deduction that reduces your taxable income, this credit directly reduces your tax bill. It’s free money from the government for doing something you should already be doing: saving for retirement.

See If You Qualify For The Saver’s Credit As An Expat

Why Does This Matter for Me as an Expat?

As an American living abroad, you’re already dealing with complex tax obligations. The Saver’s Credit provides a bright spot: you can reduce your U.S. tax liability while building retirement savings, regardless of which country you call home.

Many expats assume they can’t benefit from U.S. retirement incentives while living overseas. That’s simply not true. Whether you’re contributing to an IRA, participating in your overseas employer’s 401(k), or managing both U.S. and foreign retirement accounts, the Saver’s Credit could apply to your eligible U.S. contributions.

Do I Qualify for the Saver’s Credit?

To be eligible for the Saver’s Credit, you must be at least 18 years old, not a full-time student, and not claimed as a dependent on someone else’s tax return. Additionally, your adjusted gross income must fall below specific thresholds.

Age and Status Requirements

You must meet all three of these requirements:

- Age: You must be 18 years old or older by December 31st of the tax year

- Student status: You cannot be a full-time student for five or more months during the year

- Dependency: You cannot be claimed as a dependent on anyone else’s tax return

A school includes technical, trade, and mechanical schools. It doesn’t include on-the-job training courses, correspondence schools, or schools offering courses only through the Internet.

What Are the Income Limits?

Your AGI determines whether you qualify and what percentage credit you can claim. The income limits are:

- Single or Married Filing Separately: $39,500

- Head of Household: $59,250

- Married Filing Jointly: $79,000

Traditional IRA or 401(k) contributions reduce your AGI, potentially moving you into a higher credit bracket. This creates a double benefit: the deduction lowers your taxable income AND might qualify you for a larger credit.

How Much Credit Can I Get?

The credit is 50%, 20% or 10% of the first $2,000 ($4,000 if married filing jointly) that you contribute to eligible retirement accounts, making the maximum credit $1,000 ($2,000 if married filing jointly).

Credit Rate Thresholds

Your credit percentage depends on your AGI and filing status:

| Filing Status | 50% Credit | 20% Credit | 10% Credit | No Credit |

|---|---|---|---|---|

| Single, Married Filing Separately, Qualifying Surviving Spouse | AGI up to $23,750 | $23,751-$25,500 | $25,501-$39,500 | Over $39,500 |

| Head of Household | AGI up to $35,625 | $35,626-$38,250 | $38,251-$59,250 | Over $59,250 |

| Married Filing Jointly | AGI up to $47,500 | $47,501-$51,000 | $51,001-$79,000 | Over $79,000 |

How This Works for Expats: Real Examples

Example 1: Digital Nomad in Singapore

Sarah, a single filer working in Singapore, has an AGI of $24,000 after taking the Foreign Earned Income Exclusion. She contributes $3,000 to her traditional IRA:

- Eligible contribution: $2,000 (maximum)

- Credit rate: 20% (based on her AGI of $24,000)

- Saver’s Credit: $400

Example 2: Entrepreneur Couple in Portugal

Mike and Lisa file jointly with a combined AGI of $45,000. They each contribute $2,000 to their IRAs ($4,000 total):

- Eligible contribution: $4,000 (maximum for joint filers)

- Credit rate: 50% (based on their AGI)

- Saver’s Credit: $2,000

Example 3: Corporate Expat Using FEIE

John excludes $120,000 in foreign earned income using the FEIE but has $26,000 in U.S. investment income. His AGI is $26,000. He contributes $2,000 to his IRA:

- Eligible contribution: $2,000

- Credit rate: 10% (based on his AGI of $26,000)

- Saver’s Credit: $200

This example shows how expats who use the FEIE often qualify for the credit because excluded income doesn’t count toward AGI limits.

What Retirement Accounts Qualify?

The Saver’s Credit applies to contributions you make to:

- Traditional and Roth IRAs

- 401(k), 403(b), and 457(b) plans

- SIMPLE IRAs and SARSEPs

- Federal Thrift Savings Plan (TSP)

- ABLE accounts (for designated beneficiaries)

What Doesn’t Count

Rollover contributions do not qualify for the credit. Only new money going into retirement accounts counts toward the Saver’s Credit.

Will Past Withdrawals Affect My Credit?

Here’s where it gets tricky: your eligible contributions may be reduced by any recent distributions you received from a retirement plan or IRA, or from an ABLE account.

The IRS looks at distributions you received during:

- The tax year you’re claiming the credit

- The two preceding tax years

- The period after the tax year ends until your return’s due date (including extensions)

This means if you took a $1,000 distribution from your 401(k) in 2023, 2024, or early in the current year (before filing), and you contributed $2,000 to your IRA, your eligible contribution for the credit would be reduced to $1,000.

This rule can completely eliminate your credit if recent distributions equal or exceed your current contributions.

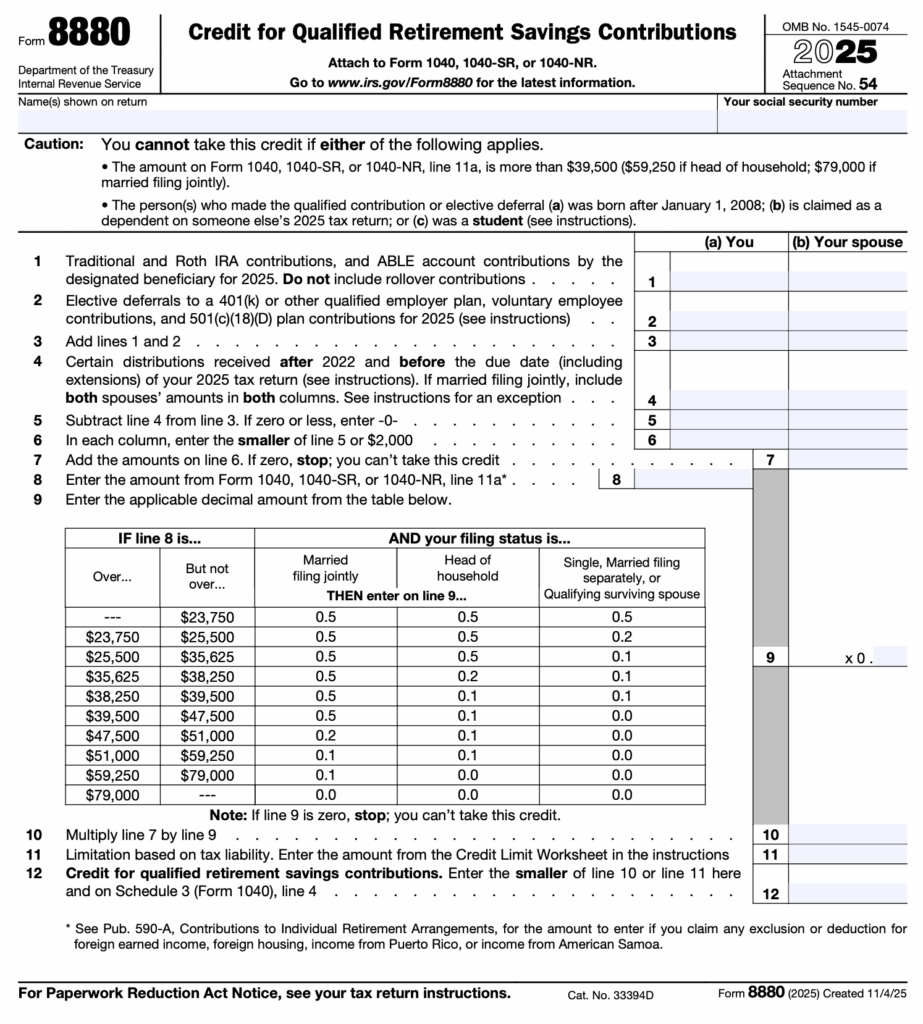

How Do I Complete Form 8880?

Form 8880 is a straightforward one-page form, but accuracy is crucial. Here’s the step-by-step process:

Step 1: Gather Your Information

You’ll need:

- Total retirement contributions for the tax year

- Any distributions from retirement accounts in the current and two preceding years

- Your adjusted gross income from Form 1040

Step 2: Complete the Form

- Lines 1-3: Enter your contributions to different types of retirement accounts

- Line 4: Subtract any distributions from the testing period

- Lines 5-7: Calculate your net eligible contributions (maximum $2,000 per person)

- Line 8: Enter your AGI from Form 1040

- Line 9: Use the form’s table to find your credit percentage

- Lines 10-12: Calculate your final credit amount

Step 3: Apply Credit Limitations

The credit cannot exceed your total tax liability. You’ll need to complete the Credit Limit Worksheet if other credits apply to your return.

How Does the FEIE Affect My Saver’s Credit?

If you claim the Foreign Earned Income Exclusion (FEIE), your excluded income doesn’t count toward AGI limits for the Saver’s Credit. This often puts you in lower income brackets, making you eligible for higher credit percentages—even if you earn significant income abroad.

Many of our CPAs and Enrolled Agents are expats themselves, and because they live in 14 timezones, they experience firsthand the challenges of living abroad. They have the knowledge and patience to help you leverage these benefits.

Can I Use Both U.S. and Foreign Retirement Plans?

Many expats contribute to both U.S. and foreign retirement plans. Only contributions to U.S.-qualified plans count for the Saver’s Credit. However, you can often make IRA contributions based on foreign earned income, creating opportunities to claim the credit.

What If I’m Behind on Filing?

If you’re catching up on unfiled returns, you can still claim the Saver’s Credit for years when you made eligible contributions. The credit can help reduce tax liability on past-due returns, though you cannot receive a refund if the credit exceeds your tax owed (it’s non-refundable).

No matter how late, messy, or complex your return may be, we can help. We’ve helped over 23,000 expats get current with the IRS through our Streamlined Filing procedures.

What Mistakes Should I Avoid?

Exceeding the AGI Limits

Track your income carefully throughout the year. If you’re close to the AGI threshold, consider maximizing traditional IRA or 401(k) contributions to lower your AGI.

Forgetting About Distributions

The two-year lookback rule catches many taxpayers off guard. Before claiming the credit, review all retirement account activity from the current and two preceding years.

Missing the Filing Deadline

The tax filing deadline is April 15. Expats get an automatic extension to June 15. Unlike most retirement contributions, you cannot claim the Saver’s Credit on an amended return if you miss the original deadline.

Not Claiming When Eligible

Many low- and moderate-income taxpayers don’t realize they qualify. The credit is particularly valuable because it’s dollar-for-dollar tax reduction, not just a deduction.

How Can I Maximize My Benefit?

Timing Your Contributions

For IRAs, you have until the tax filing deadline to make contributions for the previous year. This gives you flexibility to optimize both your AGI and credit eligibility after seeing your full year’s income.

Considering Roth vs. Traditional

Traditional IRA contributions reduce your AGI (potentially increasing your credit rate), while Roth contributions don’t. However, Roth contributions still qualify for the credit itself.

Using Spousal Contributions

If you’re married, each spouse can qualify for up to $1,000 in credits ($2,000 total) based on contributions of up to $2,000 each. This works even if only one spouse has earned income.

What’s Changing in 2027?

Beginning in 2027, the Saver’s Credit will be replaced by the Saver’s Match. By making annual contributions of up to $2,000 to a 401(k)-type plan or an Individual Retirement Account (IRA), you can receive as much as an annual $1,000 Saver’s Match contribution from the Treasury. Unlike the current credit, this will be a direct government contribution to your retirement account.

This means 2026 is the last year to claim the current Saver’s Credit structure for retirement contributions, making it even more important to take advantage of this benefit while it’s available. Starting with 2027 tax returns, Form 8880 will only be used to claim the saver’s credit for ABLE account contributions. A new separate form will be used to claim the Saver’s Match.

What Are My Next Steps?

If you think you might qualify for the Saver’s Credit:

- Calculate your AGI including any exclusions or deductions

- Review your retirement contributions for the year

- Check for any distributions in the past three years

- Complete Form 8880 when filing your return

- Plan ahead to maximize this benefit before the transition to the Saver’s Match

The Saver’s Credit represents one of the most valuable tax benefits available to Americans with moderate incomes. As an expat, you’re already dealing with complex tax rules—don’t miss out on this opportunity to reduce your tax bill while building financial security.

Have questions about the Saver’s Credit or other expat tax matters? If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

Need Help Filing Form 8880 With Your Expat Return?

This article provides general information and should not be considered personalized tax advice. Tax laws change frequently, and individual circumstances vary. Always consult with a qualified tax professional for advice specific to your situation.

Related Resources

- Foreign Earned Income Exclusion: How to Claim It

- IRAs for Expats: Contribution Rules and Tax Benefits

- Expat Retirement Planning Guide

- Streamlined Filing Procedures for Late Filers

- How to File Late Taxes as a U.S. Expat

- Form 1040: U.S. Tax Return Guide for Expats

- US Expat State Tax Guide

- Foreign Tax Credit: How It Works for Expats

- U.S. Expat Tax Guide