What is GILTI? Examples to Understand GILTI

One of the most important changes for American entrepreneurs was the new tax on global intangible low-taxed income (GILTI). To help you understand what this tax means for you, we’re going to take a deep dive into GILTI, including examples of ways expats can tackle GILTI and the benefits and disadvantages of each scenario below.

Key Takeaways

- Global intangible low-taxed income, or GILTI, is a tax that impacts US entrepreneurs that own a majority of a foreign created corporation on their foreign earnings.

- In general, “global intangible low-taxed income(GILTI)” is any net income, even if zero, that is earned either (1) in a foreign jurisdiction where the US company pays little or no income tax or (2) by a US company on its foreign-owned intangible assets.

What Is GILTI?

First things first: what exactly is GILTI? Technically, ‘global intangible low-taxed income’ refers to foreign income earned by controlled foreign corporations (CFCs) from intangible assets, such as intellectual property rights. A CFC is a foreign corporation in which American shareholders own a majority of the shares. However, in practice, GILTI covers all income earned by a CFC except:

- Subpart F income

- Income that is not Subpart F income because it is subject to an exception for income that is highly taxed

- Income that is effectively connected to a US trade or business

- Related-party dividends

- Income from certain foreign oil and gas extractions

Once these forms of income are excluded, the remaining income will generally be considered GILTI.

While GILTI excludes Subpart F income, Subpart F income is still taxed separately. The TCJA did not remove Subpart F taxation—it merely added GILTI alongside.

How Does the Tax Cut and Jobs Act Tax GILTI?

With the passage of the Tax Cut and Jobs Act (TCJA), US shareholders who own at least 10% of controlled foreign corporations (CFCs) are now taxed annually on CFC’s GILTI. This applies regardless of whether the US shareholder has actually received the CFC income as a dividend.

Dreading the last minute scramble pulling together your tax documents? Despair no more! This simple checklist lists the documents you need to have on hand when preparing to file.

The rate for this tax range depends on the details of the shareholder. For corporate shareholders, the GILTI tax rate is technically flat at 21%. In practice, however, it usually ranges from 10.5% to 13.125%. For individual shareholders, GILTI is taxed at their individual income tax rate. (This ranges from 10% to 37%, depending on your income level.)

In addition to possibly paying a higher tax rate, individual shareholders are also unable to claim the same deductions and credits as corporate shareholders. This means that the TCJA GILTI tax is applied more harshly to individual shareholders than corporate entities.

An easy way to know if you are obligated to pay GILTI is if you are required to file Form 5471 as a shareholder in a CFC. Just like with the GILTI tax, any US person with at least 10% ownership of a CFC is required to file Form 5471. The thresholds for both are identical.

How Does GILTI Affect American Expat Entrepreneurs?

GILTI applies to many expats who have formed (or are considering forming) a corporation in a foreign country. The tax law is complex, and not everyone will be impacted by GILTI. However, it is important for expats to understand how GILTI impacts them so they can make informed decisions about their business structure.

Following are four examples of how a US expat entrepreneur might be affected by the GILTI tax if he or she owns a foreign corporation.

Example #1: Individual Shareholder

For our first scenario, let’s say you are an individual shareholder in a foreign corporation. Because you are an individual shareholder, you will be taxed at your individual income rate.

Filing as a single person with an income of $100,000 per year, you would be in the 24% tax bracket for the 2023 tax year. That means that your CFC’s GILTI would also be taxed at 24%.

Once taxed, the GILTI will not be taxable again, so if you receive dividends at a later date, the GILTI portion of the dividend will be tax-free when received. There’s a catch though: foreign taxes paid. You could not claim the corporate taxes that the CFC paid on your individual tax return as a Foreign Tax Credit, and any foreign income taxes paid on your dividends later may not be eligible for carryback to offset the GILTI. Because of this, your foreign earnings may still be subject to double taxation.

Example #2: Section 962 Corporation

Another option is to make a Section 962 election to be taxed as a corporation. If you make this election, the GILTI will be taxed at the corporate tax rate of 21%.

There are certainly some advantages to this approach. The main advantage is that you can claim a Foreign Tax Credit of up to 80% of any foreign corporate taxes you pay. This allows you to offset the tax on your GILTI. (Depending on the corporate tax rate of the country you’re in, you may be able to erase your entire US GILTI tax debt.)

The downside to this option is that when you take dividends from the company, the dividends will be taxable on your personal tax return because they are not considered PTI (Previously Taxed Income). Therefore, you’re subject to two tiers of taxation: the GILTI tax at corporate rates (21%) under a Section 962 election (potentially offset by the Foreign Tax Credit) in addition to the tax on the qualified dividends (15% at the income level in this example, and generally at a 20% maximum for all other income levels).

However, when you receive dividends from a foreign entity, you will likely pay foreign taxes in the foreign country on that dividend income. You can then use the Foreign Tax Credit to offset the US tax on the dividend income (potentially offsetting the full amount of US tax on the dividends depending on the foreign tax rate).

Because of the lowered tax rate on GILTI and the ability to utilize both corporate and personal foreign taxes paid for the Foreign Tax Credit, this is generally seen as a preferable option for many taxpayers. However, the ultimate amount of tax you may pay in the future will depend on several things, such as the amount of income the corporation is expected to earn in the future, the amount of dividends expected to be paid in the future, and you intend on selling any shares in the future. Although making a 962 election seems like it is a good idea, careful planning needs to be done.

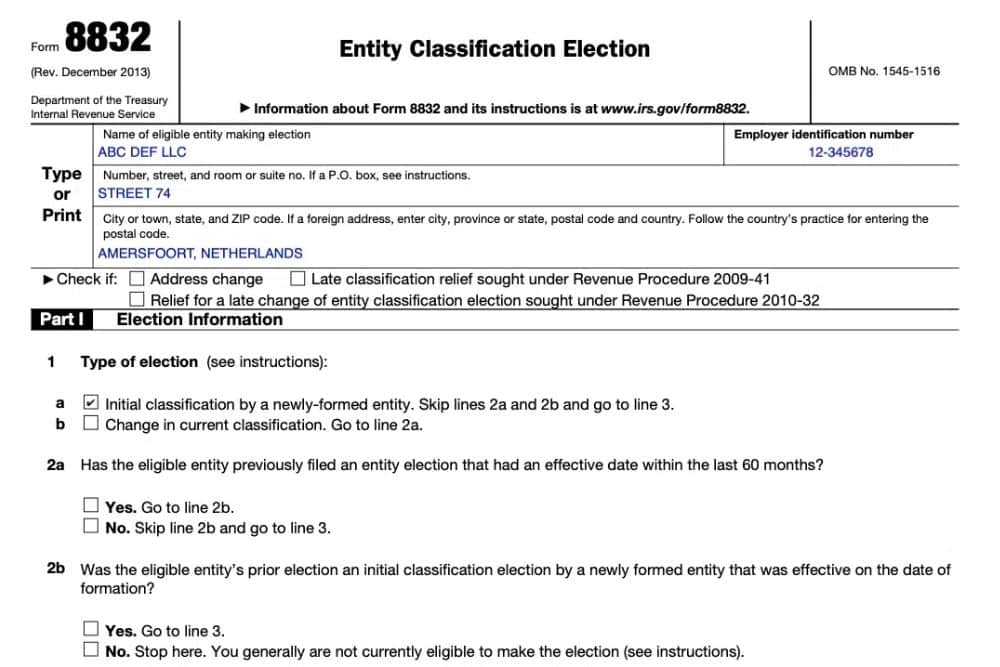

Example #3: Disregarded Entity

Some expat entrepreneurs can also choose to be taxed as a disregarded entity by filing Form 8832. This option is only available when a CFC is owned entirely by one US shareholder or qualifies as a joint venture between US spouses. The IRS also does not allow this election for specific types of corporations formed in specific countries, these corporations being known as “Per Se” corporations.

When you elect to be taxed as a disregarded entity, your CFC will have pass-through income like a sole proprietorship, but the business itself will be considered a separate entity for liability purposes.

If you make this election, you will have to report your CFC’s information on Form 8858. Your income would then be reported as self-employment income on Schedule C, which is taxed first at individual tax rates and again at self-employment tax rates (15.3%).

The primary benefit of this option is that you can use the Foreign Earned Income Exclusion (FEIE) to reduce or erase your taxable income. Or, you can use the Foreign Tax Credit to offset your US taxes based on any foreign taxes you’ve paid for that same income.

On the other hand, the potential self-employment tax of 15.3% is a major downside. The good news is that if you live in a country that has a totalization agreement with the US, you may be able to claim an exemption from the US self-employment tax.

Example #4: US Corporation

Finally, you could also form a US C-corporation to hold your CFC shares. In this case, your US corporation would also be subject to the GILTI tax at a minimum rate of 15%, but you could use a Section 250 deduction to reduce your GILTI tax by 50%. This method would also allow you to use the Foreign Tax Credit to cover up to 80% of any foreign corporate taxes you paid. (Once again, depending on the tax rate in the foreign country, this might offset the GILTI tax entirely.)

The downside is that you have to form a US C-corporation and incur the legal fees and formation costs in addition to the annual tax reporting requirements involved with a corporation. Additionally, when you want to issue dividends from the foreign corporation, those would need to be paid to the US parent corporation and then distributed to you personally from there, incurring multiple layers of taxation.

The added effort of this approach may be worthwhile for foreign companies with millions of dollars in revenue. However, for smaller foreign entities owned by one US expat, utilizing the Section 962 election or the disregarded entity election option is generally preferable.

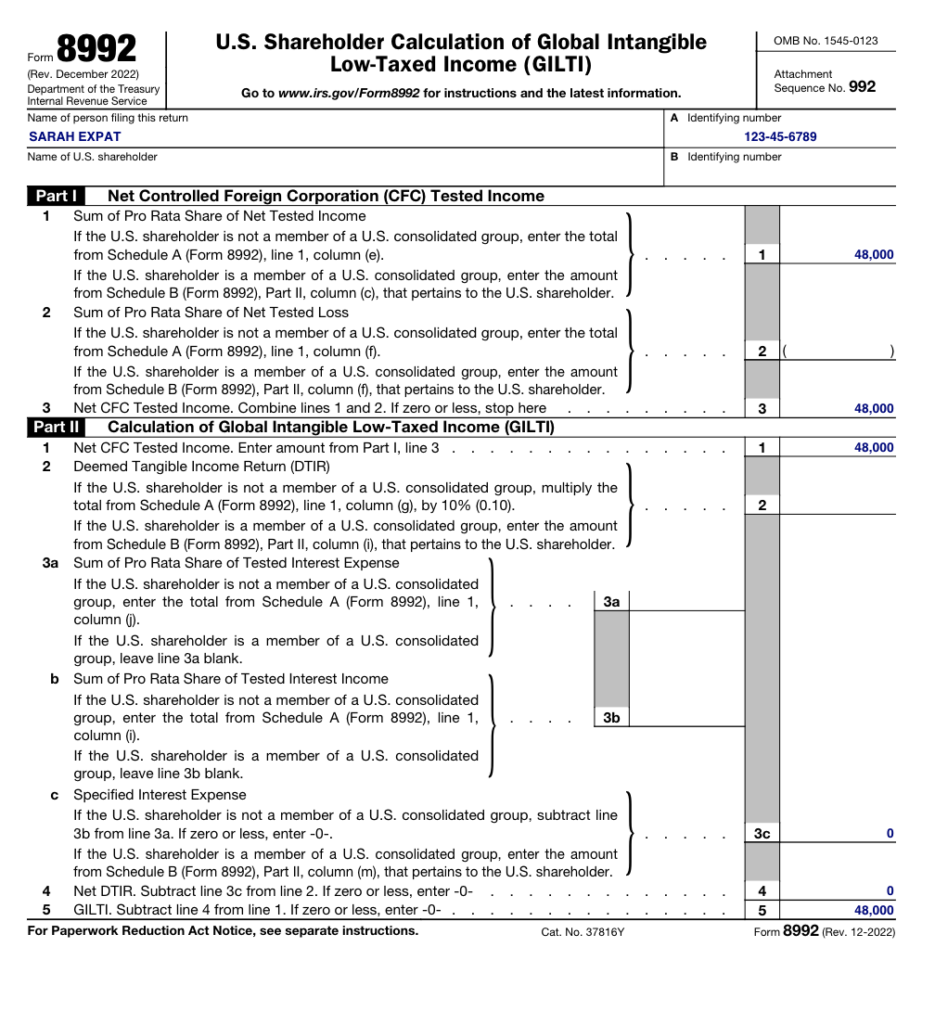

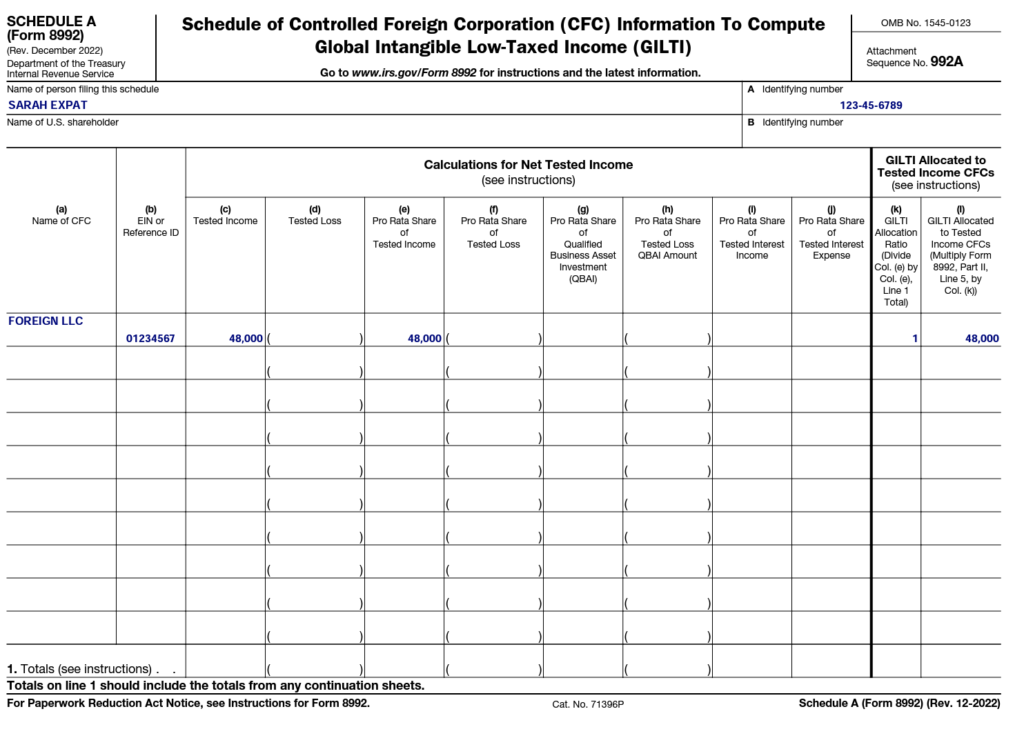

An Example of How GILTI Is Calculated

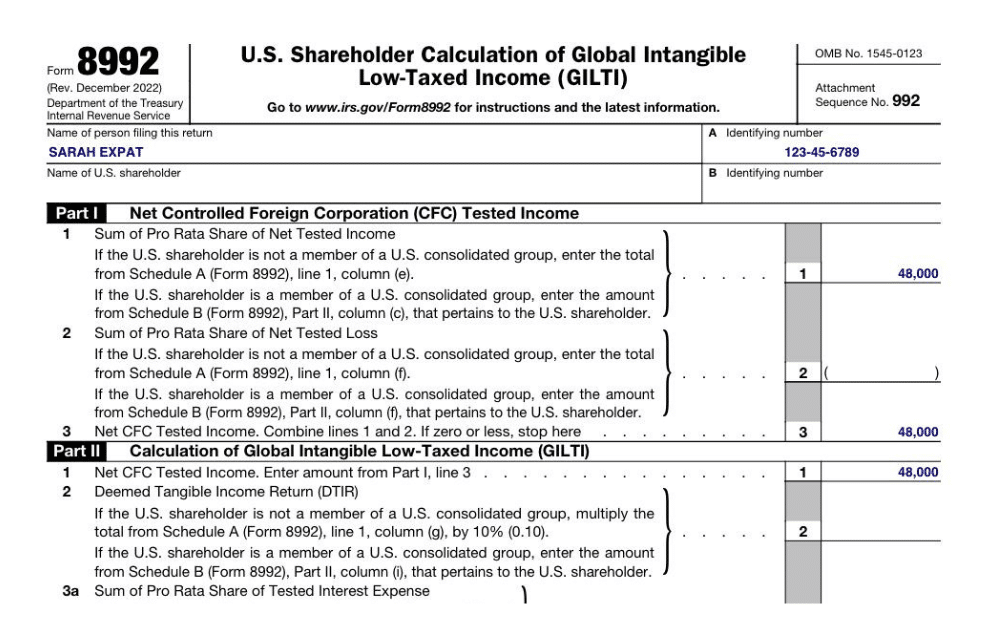

Next, let’s walk through a brief case study of how to make a GILTI tax calculation in the case of a US shareholder (Sarah Expat) who has a single, profitable CFC in this GILTI example:

- CFC’s gross income, fewer deductions, and Subpart F income = Tested Income

- Certain depreciable assets used in the business = QBAI (Qualified Business Asset Investment)

- 10% of QBAI = DTIR (Deemed Tangible Income Return)

- Tested Income, less DTIR = GILTI, taxable to the US shareholder

Sarah Expat owns a public relations business that she operates through a foreign LLC that she solely owns. She spends 35 days or less in the US and meets all other requirements for the FEIE. She is single, takes the standard deduction, and does not have any other income or deductions.

In 2023, she had gross receipts of $50,000 for services provided to clients and no Subpart F income. She had operating expenses of $2,000 and did not own any depreciable business property.

Compare her US income tax both with and without a salary:

| No Salary | $36,000 Salary | |

| FC Gross Income | $ 50,000.00 | $ 50,000.00 |

| Less FC Deductible Expenses: | ||

| Operating Expenses | ($ 2,000.00) | ($ 2,000.00) |

| Salary | $ 0.00 | ($ 36,000.00) |

| FC Tested Income | $ 48,000.00 | $ 12,000.00 |

| Less DTIR (QBAI = $0) | $ 0.00 | $ 0.00 |

| GILTI | $ 48,000.00 | $ 12,000.00 |

| US Tax Return: | ||

| Income: | ||

| Wages, Salary | $ 0.00 | $ 36,000.00 |

| GILTI | $ 48,000.00 | $ 12,000.00 |

| Gross Income | $ 48,000.00 | $ 48,000.00 |

| Less FEIE | $ 0.00 | ($ 36,000.00) |

| Less Standard Deduction ( 2023, Single) | ($ 13,850.00) | ($ 13,850.00) |

| US Taxable Income | $ 36,000.00 | $ 0.00 |

| US Tax Total | $ 4,238.00 | $ 0.00 |

This example illustrates how the sole owner of a small controlled foreign corporation may mitigate the impact of GILTI without filing certain elections or restructuring their business. Of course, any planning should consider the impact of utilizing the Foreign Tax Credit instead of FEIE, as well as the effect on any foreign corporate and individual taxes.

Want Expert Advice on GILTI and How It Can Affect Your Expat Taxes?

Greenback’s team of experts is ready to ensure your taxes are prepared correctly without any hassle, including GILTI.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.