FBAR Filing: Requirements, Deadlines, and Penalties

- What Is an FBAR?

- FBAR Filing Requirements: Who Has to File?

- When Is the FBAR Due?

- What Counts Toward the $10,000 FBAR Threshold?

- How Do You File an FBAR Online?

- What If You Have Not Filed an FBAR?

- What Are the FBAR Penalties?

- How Does the FBAR Compare to Form 8938?

- Special FBAR Situations

- Common FBAR Mistakes to Avoid

- Frequently Asked Questions about FBAR

- Let Greenback Handle Your FBAR

- Related Resources

You must file an FBAR (FinCEN Form 114) if the combined balance of your foreign financial accounts went over $10,000 at any point during the year. The FBAR is filed with FinCEN, the Treasury Department’s Financial Crimes Enforcement Network, separately from your tax return. The filing deadline is April 15, with an automatic extension to October 15. Filing an FBAR creates no additional tax liability. It is an informational disclosure only.

The $10,000 threshold is aggregate: all your foreign accounts are added together, not evaluated individually. Non-willful penalties for failing to file reach $16,536 per form, but voluntary compliance programs allow most first-time filers to catch up without incurring any penalty.

The most common account types that trigger FBAR requirements include:

- Foreign bank accounts: checking, savings, and certificates of deposit

- Foreign investment and brokerage accounts held at overseas financial institutions

- Foreign retirement and pension accounts such as UK ISAs, Australian superannuation funds, and Canadian RRSPs

- Accounts with signature authority: accounts you control but may not personally own, including employer accounts

Read on to find out who must file, what the deadlines are, and what to do if you have years of unfiled FBARs.

Ensure Your FBAR Form is Filed Correctly. Get Expert Help!

What Is an FBAR?

The FBAR, filed on FinCEN Form 114, is an annual reporting form filed electronically with the U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN). It is submitted through the BSA E-Filing System, separately from your federal tax return.

Created under the Bank Secrecy Act, the FBAR exists to help the U.S. government detect tax evasion, money laundering, and other financial crimes involving offshore accounts. The form collects basic information: the names and addresses of foreign financial institutions, account numbers, and the highest balance held in each account during the year.

One critical point: filing an FBAR does not mean you owe additional taxes. The FBAR is a disclosure form. It tells the Treasury you have foreign accounts. It does not affect your tax liability.

Since 2012, all FBARs must be filed electronically. Paper submissions are no longer accepted.

FBAR Filing Requirements: Who Has to File?

FBAR filing is required if all four of the following conditions apply to you, per FinCEN’s FBAR reporting guidelines:

| Trigger | What It Means | Key Detail |

|---|---|---|

| U.S. person status | Citizen, Green Card holder, resident alien, or U.S. entity | Where you live does not change this obligation |

| Foreign financial account | Account located outside the U.S. | Includes bank, brokerage, mutual fund, and many pension accounts |

| Aggregate value over $10,000 | Combined maximum balance across all accounts | Measured at any single point during the year, even briefly |

| Financial interest or signature authority | You own the account, or you can direct transactions | Signature authority alone creates a filing obligation |

Who Is Considered a U.S. Person for FBAR Purposes?

You are a U.S. person for FBAR purposes if you are any of the following:

- A U.S. citizen, no matter where in the world you live

- A lawful permanent resident (Green Card holder), even after years of living abroad

- A resident alien who meets the IRS substantial presence test

- A domestic entity formed under U.S. law, including LLCs, corporations, partnerships, trusts, and estates

A U.S. citizen who has lived in Germany for 20 years has the same FBAR obligation as a New Yorker with a French savings account.

What About Joint Accounts and Signature Authority?

Joint accounts count in full toward your $10,000 threshold, even when you own only part of the funds. Each U.S. person on a joint account must generally file separately. However, spouses may file a single combined FBAR if all foreign accounts are jointly owned and neither spouse has separate foreign accounts, provided both spouses sign Form 114a.

Signature authority creates a filing obligation even in the absence of ownership. If you can direct transactions on an employer account, a family member’s account, or a business account, and the combined value of your reportable accounts crosses $10,000, that account belongs on your FBAR.

When Is the FBAR Due?

The FBAR deadline for the 2025 tax year is April 15, 2026, with an automatic extension to October 15, 2026. You do not need to request this extension. It applies automatically to every filer.

| Filing Deadline | Date | Notes |

|---|---|---|

| FBAR filing deadline | April 15, 2026 | For 2025 tax year accounts |

| FBAR extension (automatic) | October 15, 2026 | No request, form, or fee required |

| U.S. tax return (expats) | June 15, 2026 | Separate from FBAR; does not affect FBAR deadline |

| Tax return extended deadline | October 15, 2026 | Requires Form 4868; separate from FBAR |

When are FBARs due? The FBAR filing deadline is April 15. If you miss it, you automatically receive an extension to October 15. You do not need to request the FBAR extension. It is granted to every filer.

Does the FBAR extension apply to your tax return? No. An extension for your federal income tax return does not extend your FBAR deadline, and the FBAR extension does not extend your tax return deadline. The two are entirely independent.

Does the automatic June 15 extension for Americans abroad apply to FBARs? No. That extension applies only to income tax returns and has no effect on your FBAR filing obligation.

If you served in a combat zone during the tax year, you may qualify for additional time under military tax relief provisions. A qualified tax professional can confirm whether this applies to your situation.

What Counts Toward the $10,000 FBAR Threshold?

The $10,000 threshold is based on the aggregate maximum value of all your foreign financial accounts combined, not on each account individually. If any single combination of your accounts briefly touched $10,001, you have crossed the threshold for the entire year.

Accounts That Are Reportable

- Foreign bank accounts: checking, savings, and certificates of deposit

- Foreign investment and brokerage accounts held at foreign institutions

- Foreign mutual funds and unit trusts

- Foreign retirement and pension accounts (with some exceptions; see below)

- Life insurance policies with cash surrender value held at foreign institutions

- Accounts where you have signature authority, even if you do not own the funds

Accounts That Are Not Reportable

- Accounts held at U.S. military banking facilities overseas

- IRA or 401(k) accounts at U.S. institutions that invest in foreign assets

- Social Security payments deposited into foreign bank accounts (the account itself may still be reportable)

Currency conversion: Convert all foreign currency balances to U.S. dollars using the Treasury’s official exchange rates for December 31 of the reporting year.

Real-World Examples

Example 1: Digital Nomad with Multiple Small Accounts

Sarah works remotely and lives in Portugal. She has EUR 3,500 in a Portuguese checking account, GBP 4,200 in a UK savings account, and USD 3,800 in a Mexican investment account. Her combined maximum reached approximately $11,800. Even though no single account exceeded $10,000, Sarah must file an FBAR that reports all three accounts.

Example 2: Retiree with a Foreign Pension

James retired to Spain and continues to receive a UK pension. He has EUR 15,000 in a Spanish bank account. His Spanish account alone exceeds the threshold, and his UK pension account may also be reportable depending on whether he has access to the funds. James must file an FBAR and should consult a tax professional about the pension account’s reportability.

Example 3: Corporate Expat with Signature Authority

Michelle works for a U.S. company in Singapore. She has signing authority over her employer’s Singapore operating account, which holds $500,000. Michelle does not own those funds, but she can direct transactions. Her employer account must appear on her personal FBAR because of her signature authority.

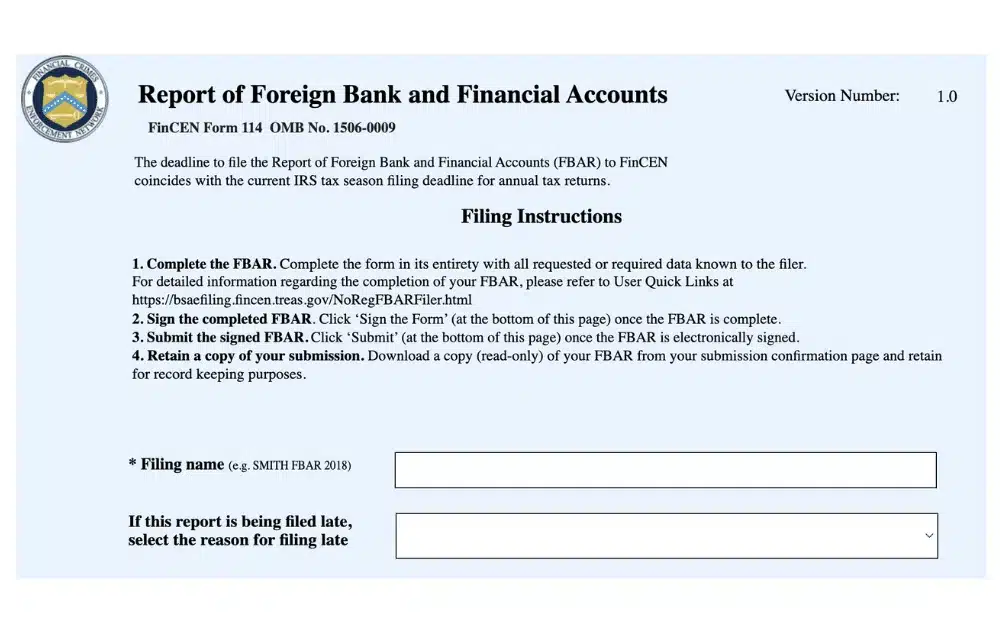

How Do You File an FBAR Online?

You file an FBAR online through the BSA E-Filing System on FinCEN’s website. All FBAR submissions are electronic. The system walks you through each required field. You do not attach the FBAR to your tax return, and there is no paper filing option.

Information You Will Need

- Account numbers for all reportable foreign accounts

- Names and addresses of the financial institutions where the accounts are held

- The maximum balance in each account at any point during the year

- Account type: bank, securities, or other

- Your ownership interest or the nature of signature authority for each account

Convert all foreign currency amounts to U.S. dollars using the Treasury exchange rates described above.

For a step-by-step walkthrough of the form fields, how to handle multiple accounts, joint filers, and signature authority accounts, see our guide to completing FinCEN Form 114.

FBAR Filing Services: We Handle the Details for You

What If You Have Not Filed an FBAR?

If you have past-due FBARs, do not wait. The IRS has voluntary compliance programs specifically designed to help people get current before the IRS contacts them first. Filing proactively is almost always the better path, and most filers who use these programs avoid penalties entirely.

Delinquent FBAR Submission Procedures

This program is for filers who are current on their tax returns but have missed one or more FBAR filings. You qualify if:

- The IRS has not already contacted you about the delinquent FBARs

- You properly reported all foreign account income on your U.S. tax returns

- Your failure to file was non-willful (you did not know about the requirement or received incorrect advice)

Process: File all missing FBARs electronically for up to six years back and include a brief statement explaining why they were not filed on time. When the IRS accepts this, all penalties are waived.

Learn more: Filing Past-Due FBAR Forms

Streamlined Filing Compliance Procedures

Use this program if you are behind on both your tax returns and your FBARs. You file three years of amended or delinquent tax returns, six years of FBARs, and a certification that your failure to file was non-willful.

For Americans who lived outside the U.S. for at least 330 days in one of the three years covered, there are typically no penalties under the Streamlined Foreign Offshore Procedures. U.S. residents use the Streamlined Domestic Offshore Procedures, which carry a 5% penalty on the highest aggregate balance of unreported accounts.

Learn more: Everything to Know About Streamlined Filing

What Are the FBAR Penalties?

The purpose of discussing FBAR penalties is not to create anxiety. It is to underscore why voluntary compliance matters and why acting before the IRS contacts you makes such a significant difference.

Non-Willful Violations (Honest Mistakes)

- Up to $16,536 per form per year for unfiled FBARs

- Following the Supreme Court’s 2023 Bittner ruling, penalties apply per form (per year), not per account

- The IRS frequently waives non-willful penalties for first-time filers who demonstrate reasonable cause

Willful Violations (Intentional Non-Compliance)

- Greater of $165,353 or 50% of the highest account balance per violation, per year

- Potential criminal prosecution in extreme cases (rare, but possible)

What Counts as Reasonable Cause?

- You were unaware of the FBAR requirement

- You received incorrect advice from a professional

- You made a good-faith effort to comply, but made an error

2026 Enforcement Update: Recklessness Now Triggers Willful Penalties

In January 2026, the U.S. Court of Appeals for the Second Circuit ruled in United States v. Reyes that reckless disregard of the FBAR requirement is sufficient to trigger the maximum willful penalty. You do not need to have intentionally concealed accounts. Six other circuits have adopted the same standard, meaning this interpretation now applies across nearly every U.S. jurisdiction.

At the same time, a September 2025 ruling in United States v. Sagoo gave taxpayers a potential new defense, with a federal court holding that the IRS may not be able to impose willful FBAR penalties without first providing a jury trial.

The practical takeaway: the gap between “I did not know about FBAR” and maximum willful penalty exposure has narrowed significantly. Coming forward voluntarily through the proper programs is more important than ever.

Learn more: FBAR Willful Violation: What Reyes and Sagoo Mean for U.S. Taxpayers

For a complete breakdown of how penalties are calculated, how the Bittner ruling changed the math, and how to dispute a penalty, see our complete guide to FBAR penalties.

How Does the FBAR Compare to Form 8938?

The U.S. government has two separate foreign account reporting requirements that frequently apply to the same accounts. They are often confused, but they serve different purposes and go to different agencies.

| FBAR (FinCEN Form 114) | FATCA (Form 8938) | |

|---|---|---|

| Filing threshold | $10,000 aggregate (all filers) | $200,000/$300,000 (abroad, single); $400,000/$600,000 (abroad, married) |

| Where to file | FinCEN, separately from tax return | IRS, attached to your tax return |

| What is covered | Foreign financial accounts | Foreign financial assets (broader category) |

| Who must file | Individuals and entities | Individuals only |

| Deadline | April 15 (automatic extension to October 15) | Same as your tax return deadline |

Threshold note: For Form 8938, the higher dollar figure in each pair is the threshold measured at any point during the year; the lower figure is the threshold measured on the last day of the year. For U.S. residents (not living abroad), the thresholds are significantly lower: $50,000 on the last day or $75,000 at any point (single filers).

The key distinction between the two forms: an account can hold an asset. If the account itself is a foreign brokerage account, it belongs on both the FBAR and Form 8938. If you hold a foreign asset directly, such as ownership shares in a foreign company held in your own name rather than through an account, it must be reported only on Form 8938.

Many U.S. taxpayers with foreign accounts must file both forms for the same accounts.

Learn more: FBAR vs. Form 8938: What Is the Difference and Do You Need to File Both?

Special FBAR Situations

Joint Accounts with a Non-U.S. Spouse

You do not need to report your non-U.S. spouse’s individual accounts if you have no financial interest or signature authority over them. However, if you hold joint accounts with your spouse, those accounts count toward your $10,000 threshold.

Spouses may file one joint FBAR when all foreign accounts are jointly owned and neither spouse has separate foreign accounts requiring disclosure. Both spouses must sign Form 114a to authorize the joint filing.

Learn more: FBAR Filing Rules for Joint Accounts with Non-U.S. Citizens

Business Owners and Signature Authority

If you own a business with foreign accounts or have signing authority over employer accounts abroad, special rules apply:

- Business accounts count toward your personal $10,000 aggregate threshold

- You must report accounts where you have signature authority, even if you own no portion of the funds

- Consolidated FBAR filing may be available for parent companies reporting on behalf of subsidiaries

Learn more: What Business Owners Need to Know About FBAR Filing

Children with Foreign Accounts

If your child has foreign accounts with a combined balance exceeding $10,000, you must file an FBAR on their behalf. This applies to custodial accounts, trust accounts where the child is a beneficiary, and joint accounts held with a child. The FBAR is filed in the child’s name and using the child’s Social Security Number, even if the child is not required to file a tax return.

Cryptocurrency on Foreign Exchanges

FinCEN has proposed rules that would explicitly require FBAR reporting for cryptocurrency held in foreign exchange accounts, but as of the 2025 tax year, those proposed rules have not been finalized. Current guidance suggests that if you hold crypto on a foreign exchange that also holds fiat currency (such as USD or another national currency), the entire account value may count toward the $10,000 threshold. Foreign exchange accounts holding both crypto and fiat currency should generally be reported. For accounts holding crypto only, consulting a qualified tax professional is the safest course for 2025.

Common FBAR Mistakes to Avoid

- Assuming the threshold is per account, not aggregate. The $10,000 limit applies to the combined maximum of all your foreign accounts. Three accounts at $4,000 each equal $12,000 in aggregate, requiring an FBAR for all three.

- Thinking that your foreign bank reports on your behalf. Some foreign banks share account data with the U.S. government under FATCA, but that does not eliminate your personal FBAR filing obligation.

- Forgetting dormant or old accounts. That savings account from a previous assignment abroad, still open with a few thousand dollars, counts toward your threshold if it was open during the year and your combined total crossed $10,000.

- Overlooking retirement and pension accounts. Foreign retirement accounts are generally reportable if you have access to the funds. This is a frequent blind spot for long-term expats and retirees.

- Ignoring signature authority. An employer account you can sign on, even as part of your regular job duties, belongs on your personal FBAR if the aggregate threshold is met.

Frequently Asked Questions about FBAR

Yes. All FBARs must be filed online through FinCEN’s BSA E-Filing System at bsaefiling.fincen.gov. Paper filing is not an option. The system is free to use, and the process walks you through each required field. You do not attach the FBAR to your tax return. If you prefer, a qualified tax professional can file the FBAR electronically on your behalf using a third-party e-filing authorization.

The FBAR exists to help the U.S. government detect and prevent tax evasion, money laundering, and other financial crimes involving offshore accounts. It is a reporting requirement, not a tax form. Filing an FBAR does not create additional tax liability. The form goes to FinCEN, not the IRS, though the IRS enforces FBAR penalties on FinCEN’s behalf.

The threshold is aggregate: all of your foreign financial accounts are added together. If you have three accounts holding $4,000 each, your combined total is $12,000, and you must file an FBAR reporting all three accounts, even though no single account exceeded $10,000 on its own.

Yes. The FBAR is required if your combined foreign account balances exceeded $10,000 at any single point during the year, even briefly. A temporary transfer, a payroll deposit, or a lump-sum payment that pushed the aggregate balance over the threshold for even one day creates the filing requirement for that entire year.

No. The FBAR (FinCEN Form 114) is filed separately with the Treasury’s Financial Crimes Enforcement Network and has an aggregate threshold of $10,000. Form 8938 (FATCA reporting) is attached to your federal tax return and has significantly higher thresholds, starting at $200,000 for single filers living abroad. Many taxpayers are required to file both. See our FBAR vs. Form 8938 comparison for a full breakdown.

If you properly reported all income from the foreign accounts on your U.S. tax returns, you can use the Delinquent FBAR Submission Procedures to file back FBARs without penalty. You file the missing FBARs electronically and include a brief explanation for their late filing. If you are also behind on tax returns, the Streamlined Filing Compliance Procedures allow qualifying filers to catch up on both with no penalty (for those living abroad).

Yes. The FBAR requires reporting any account over which you have signature authority, regardless of whether you own the funds. Signature authority over an employer’s foreign account is one of the most commonly overlooked FBAR triggers for corporate expats. If you can direct transactions on an employer account and the aggregate threshold is met, it must appear on your personal FBAR.

Yes, under limited circumstances. Spouses can file a joint FBAR if all foreign financial accounts are jointly owned and neither spouse has individual foreign accounts requiring separate disclosure. Both spouses must sign Form 114a to authorize the joint filing.

This is an evolving area. FinCEN has proposed rules that would explicitly require FBAR reporting for foreign-held cryptocurrency, but those rules had not been finalized as of the 2025 tax year. If you hold crypto on a foreign exchange that also holds fiat currency (USD or another national currency), the full account value likely counts toward the $10,000 threshold. For crypto-only foreign accounts, consult a qualified tax professional about your specific situation.

Let Greenback Handle Your FBAR

Many of Greenback’s CPAs and Enrolled Agents are expats themselves, living across 14 time zones. They have filed FBAR forms thousands of times and understand the real-life complexity of foreign accounts, pension systems, and multi-country situations.

FBAR filing services start at $125 for up to five accounts. Greenback handles everything from gathering the required account information to electronic submission.

FBAR Filing Done Right — Avoid Penalties, Get Expert Help

This article is for general informational purposes only and does not constitute tax or legal advice. FBAR rules are complex and change over time. Individual situations vary. Please consult a qualified tax professional for guidance specific to your circumstances.

Related Resources

- FinCEN Form 114 (FBAR): How to Report Foreign Bank Accounts

- FBAR Penalties: Non-Willful, Willful, and How to Avoid Them

- Filing Past-Due FBAR Forms: Your Options and How to Get Compliant

- FBAR vs. Form 8938: What Is the Difference?

- Streamlined Filing Compliance Procedures: Everything You Need to Know

- FBAR Willful Violation: What the Reyes and Sagoo Rulings Mean for U.S. Taxpayers

- FBAR Filing Rules for Joint Accounts with Non-U.S. Citizens

- What Business Owners Need to Know About FBAR Filing

- FATCA and Form 8938: Reporting Foreign Financial Assets

- FBAR Filing Services: Starting at $125