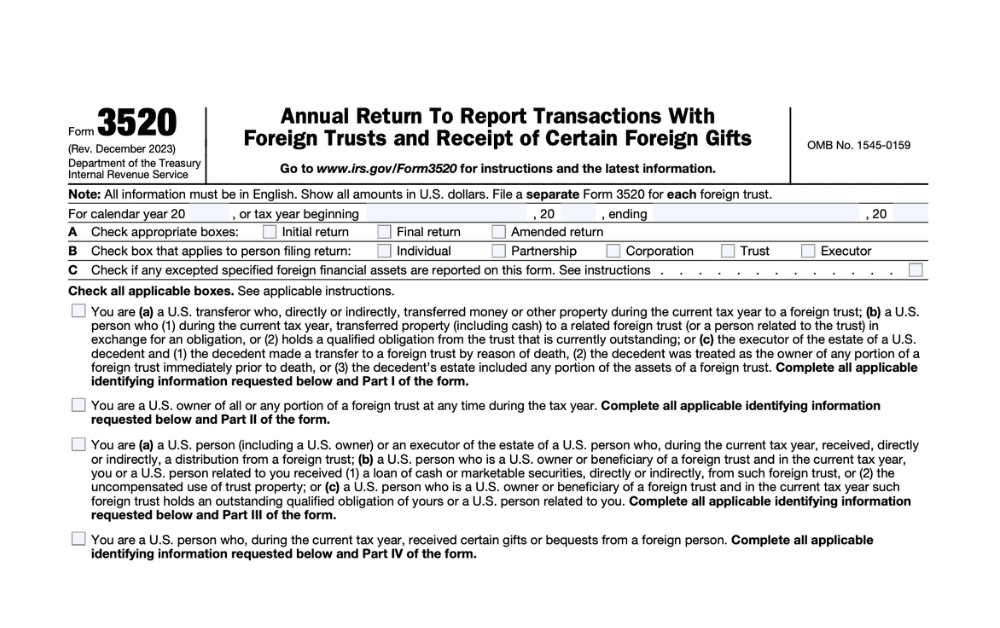

Do I Need to File Form 3520 for a Foreign Gift, Inheritance, or Trust?

If you are a U.S. person who received a gift or inheritance totaling more than $100,000 from a foreign individual or estate during the tax year, you are required to file Form 3520 with the IRS. The same applies if you received more than $20,116 (for the 2025 tax year) from foreign corporations or partnerships.

According to the IRS, Form 3520 is also required for U.S. persons who are involved in transactions with foreign trusts, including creating, transferring property to, receiving distributions from, or owning any part of a foreign trust. The most common triggers for filing include:

- Large foreign gifts or inheritances exceeding $100,000 from non-U.S. individuals or estates

- Gifts from foreign entities exceeding the annually adjusted threshold ($20,116 for 2025)

- Any distribution received from a foreign trust (no minimum threshold)

- Ownership of any part of a foreign trust under the grantor trust rules

- Transfers of cash or property to a foreign trust by a U.S. person

Form 3520 Is Informational — But Penalties Can Be Severe

Here’s what you need to know about Form 3520 and why this informational return carries some of the steepest penalties in the tax code for non-compliance.

What Triggers a Form 3520 Filing Requirement?

Form 3520 covers two distinct categories of reporting: foreign gifts and bequests, and foreign trust transactions. The rules for each are different.

Foreign Gifts and Bequests (Part IV)

You must file Form 3520 if you received gifts or inheritances from foreign sources that exceed the following thresholds during the tax year:

| Source of Gift | Reporting Threshold (2025) | What to Report |

|---|---|---|

| Foreign individual or foreign estate | More than $100,000 total | Each gift over $5,000 must be separately identified |

| Foreign corporation or foreign partnership | More than $20,116 total | Each gift and the identity of the donor |

The $100,000 threshold applies to the aggregate amount received from a single foreign person and all related parties combined, not per individual gift. If your mother abroad sends you $60,000 and your father sends $50,000 in the same year, the IRS treats this as $110,000 from related parties, triggering the filing requirement even though neither gift individually exceeds the threshold.

Foreign Trust Transactions (Parts I, II, and III)

Foreign trust reporting requirements are broader and have no dollar minimum. You must file Form 3520 if any of the following apply:

- You created a foreign trust or transferred cash or property to one

- You are treated as the owner of any part of a foreign trust under the grantor trust rules (Sections 671-679)

- You received any distribution from a foreign trust, regardless of amount

- You or a related U.S. person received a loan or use of property from a foreign trust you own or benefit from

The IRS generally considers foreign retirement plans to be trusts. Many foreign pension plans, provident funds, and other non-U.S. retirement arrangements are classified as foreign trusts subject to Form 3520 and Form 3520-A reporting. This is one of the most common surprises for Americans living abroad, particularly those participating in employer-sponsored retirement plans in their country of residence.

What Is Form 3520-A and Do I Need to File Both?

If a foreign trust has a U.S. owner, the trust itself must file Form 3520-A (Annual Information Return of Foreign Trust With a U.S. Owner). This is a separate requirement from Form 3520, and both forms must be filed.

If the foreign trust will not or cannot file Form 3520-A, the responsibility falls on the U.S. owner to complete a Substitute Form 3520-A and attach it to their Form 3520. Filing one form does not satisfy the requirement for the other.

Notable exceptions: Canadian RRSPs, RRIFs, and certain other Canadian retirement plans that qualify under Rev. Proc. 2014-55 are exempt from Form 3520-A. Additionally, certain foreign employee benefit plans may qualify for an exemption under Revenue Procedure 2020-17.

What Are the Penalties for Not Filing?

Form 3520 penalties are among the harshest in the tax code, and they apply even though the form is informational and typically does not result in tax owed. The IRS assesses penalties separately depending on which part of the form is late or incomplete.

| Violation | Penalty |

|---|---|

| Failure to report foreign gifts (Part IV) | 5% of gift value per month, up to 25% maximum |

| Failure to report trust creation or transfers (Part I) | 35% of gross value of property transferred |

| Failure to report trust distributions (Part III) | 35% of gross value of distributions received |

| Failure to file Form 3520-A (trust owner reporting) | Greater of $10,000 or 5% of gross trust assets owned |

These penalties can be stacked, meaning a U.S. person who both owns and receives distributions from a foreign trust could face penalties under multiple sections simultaneously.

Penalties can be waived if you demonstrate the failure was due to reasonable cause and not willful neglect. However, the reasonable cause standard requires you to show both that you had a legitimate reason for missing the deadline and that you acted in good faith. Preparing a strong reasonable cause argument is where professional guidance becomes essential.

When Is Form 3520 Due?

| Filer Location | Deadline | Extended Deadline |

|---|---|---|

| U.S.-based filers | April 15, 2026 | October 15, 2026 (with Form 4868) |

| Americans living abroad | June 15, 2026 (automatic) | October 15, 2026 (with Form 4868) |

Form 3520-A has a separate, earlier deadline: March 15, 2026, for calendar-year trusts.

Form 3520 must be filed separately from your income tax return and mailed to the IRS Service Center in Ogden, Utah. It generally cannot be e-filed.

If you need to file either form, requesting a regular extension on Form 4868 is strongly recommended. This extends the due date for Form 3520 as well, which can help you avoid penalties if gathering the required foreign trust or gift documentation takes longer than expected.

Why Is Form 3520 Especially Complex for Expats?

Americans living abroad are far more likely to encounter Form 3520 requirements than domestic taxpayers, often without realizing it. Several common expat situations trigger reporting obligations that have nothing to do with deliberate tax planning:

- Foreign pension participation: Contributing to an employer-sponsored pension in your country of residence can create a foreign trust for U.S. tax purposes, requiring both Form 3520 and Form 3520-A every year.

- Receiving gifts from family abroad: When foreign family members give you cash or property to help with a home purchase, education, or life event, the aggregate amount often exceeds the $100,000 threshold without anyone thinking about U.S. reporting.

- Inheritance from non-U.S. relatives: Foreign inheritances are not taxable income, but they must be reported on Form 3520 if they exceed the threshold. Many expats discover this requirement years later and face catching up.

- Foreign trust distributions: Even small distributions from a foreign trust require Form 3520, and the penalty for missing this reporting is 35% of the gross distribution amount.

If you have missed prior years’ filings, the IRS Streamlined Filing Procedures may offer a path to come into compliance without the harshest penalties, provided the non-filing was non-willful.

Let Greenback Handle Your Form 3520 Filing

Form 3520 sits at the intersection of foreign trust law, international gift tax rules, and cross-border estate planning. The form itself is detailed, the penalty structure is severe, and the rules for determining whether a foreign arrangement qualifies as a “trust” are anything but straightforward.

Greenback’s CPAs and Enrolled Agents handle Form 3520 and Form 3520-A filings for Americans abroad every day. We’ll determine whether your foreign pension, gift, inheritance, or trust triggers a filing requirement, ensure the form is completed accurately, and coordinate it with your broader expat tax return.

No matter how late, messy, or complex your return may be, we can help. You’ll have peace of mind, knowing that your taxes were done right.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on taxes or working with Greenback, contact us, and one of our Customer Champions will happily address all your concerns.

Make Sure Your Foreign Gifts and Inheritances Are Reported Correctly

This article is intended for informational purposes only and does not constitute legal or tax advice. While Greenback makes every effort to ensure the information is accurate and up-to-date, every tax situation is unique. For advice tailored to your specific situation, consult one of our expat tax professionals.

Related Resources

- Foreign Trust Reporting: A Tax Guide for Expats

- U.S. Gift Tax for Americans Abroad: Guide to Giving and Receiving

- Form 709: Do I Need to File for a Gift I Made?

- Moving Your Retirement Account Overseas: What U.S. Expats Need to Know

- Streamlined Filing Procedures: How to Catch Up on Taxes

- FBAR: What It Is, Who Must File, and How to Report Foreign Accounts

- U.S. Tax Forms for Expats: What You Need to File

- Taxes for U.S. Citizens Living Abroad

- U.S. Expat Taxes: The Complete Guide for Americans Living Abroad

- Tax Deadlines for U.S. Expats