IRS Finalizes Schedule 1-A: What the New OBBBA Deductions Mean for U.S. Expats

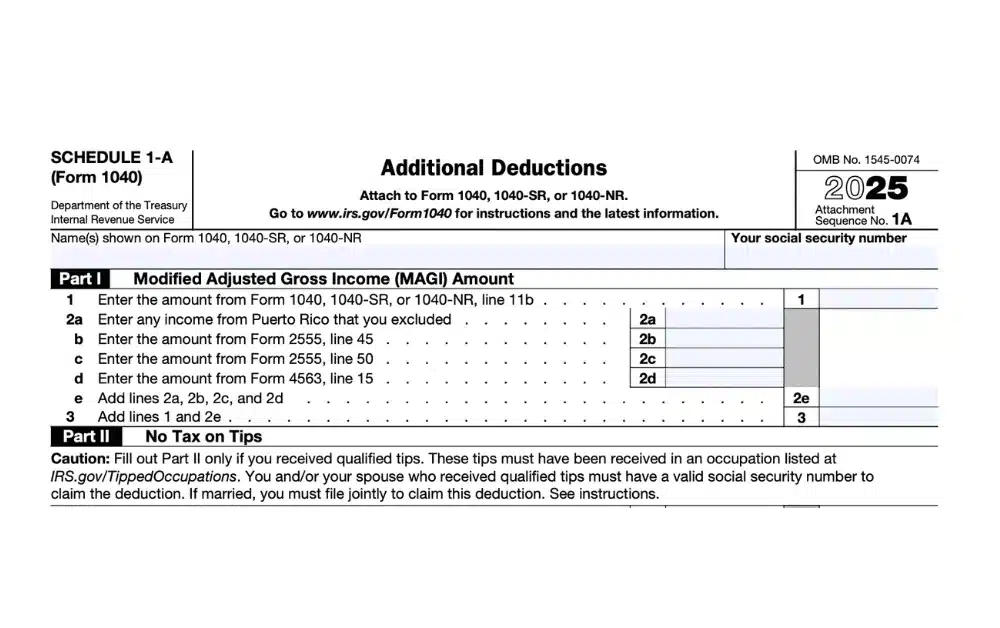

The IRS has finalized Schedule 1-A (Form 1040), a brand-new form for the 2025 tax year to be filed in 2026. This development follows Congress’s passage of the One Big Beautiful Bill Act (OBBBA) in July 2025, which temporarily added four new deductions: tips, overtime pay, car loan interest, and an enhanced senior deduction.

For Americans living abroad, the real story isn’t the deductions themselves (most expats won’t qualify) but rather how Schedule 1-A interacts with the Foreign Earned Income Exclusion (FEIE) when calculating Modified Adjusted Gross Income (MAGI). This matters because MAGI determines eligibility for many tax benefits, and the new form explicitly requires adding back excluded foreign income.

The bottom line: Schedule 1-A represents a significant structural change to the 1040 filing system, but most expats will find limited practical benefit from the actual deductions. Here’s why.

New Schedule 1-A Deductions Could Lower Your Tax Bill

Why Did the IRS Create Schedule 1-A?

When Congress passed OBBBA in July 2025, it temporarily added four new deductions effective for tax years 2025 through 2028. Rather than overcrowding existing forms, the IRS created a new schedule specifically for these OBBBA provisions.

Schedule 1-A will be filed alongside Form 1040, 1040-SR, or 1040-NR starting with the 2025 tax year (filed in 2026).

This is a completely separate form from the existing Schedule 1 (Additional Income and Adjustments), which continues to be used for reporting additional income and above-the-line deductions like student loan interest and the foreign housing deduction.

Related Article: Trump’s 2025 Tax Policies: What U.S. Expats Need to Know

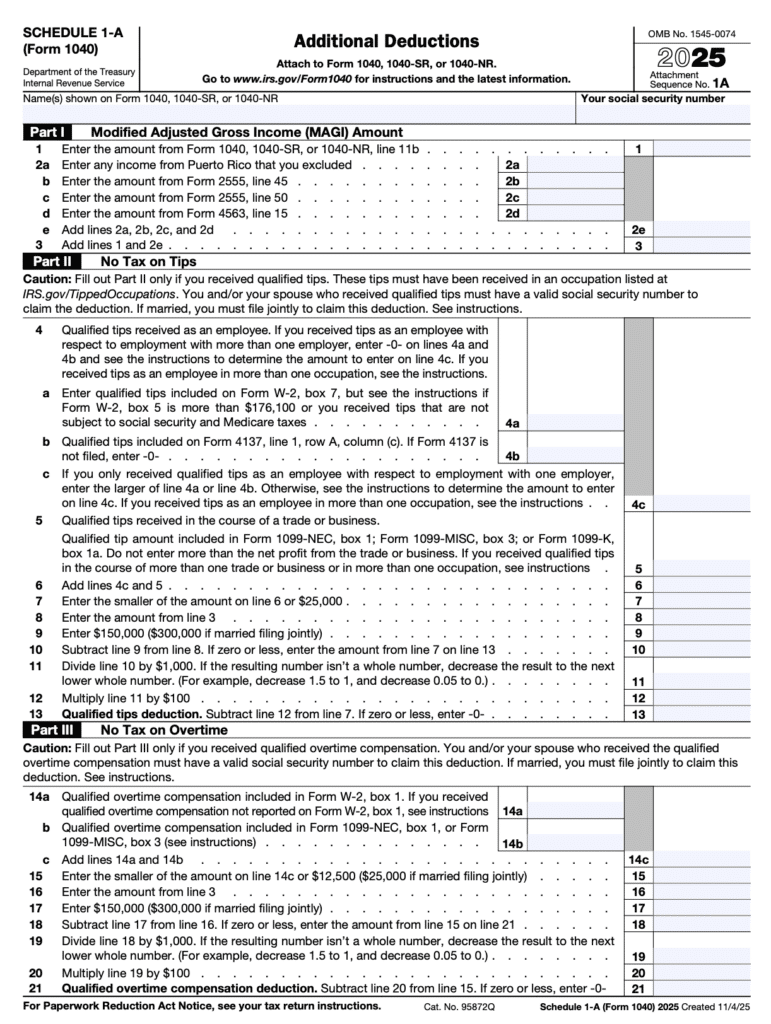

The Four OBBBA Deductions: What They Are

Schedule 1-A covers four temporary deductions:

1. Tips Deduction

Taxpayers can deduct qualified tips reported on W-2s or 1099s. For self-employed individuals, the deduction cannot exceed net business profit.

Why expats can’t use it: Foreign employers don’t have U.S.-compliant tip reporting systems, can’t withhold U.S. payroll taxes, and often operate under labor laws that don’t recognize U.S. tip reporting requirements.

2. Overtime Deduction

Covers overtime pay reported on W-2 forms. The deduction rarely applies to contractors since “overtime” is a legal concept tied to U.S. labor law.

Why expats can’t use it: Foreign employers don’t follow U.S. overtime laws or payroll systems, making qualification nearly impossible.

3. Car Loan Interest Deduction

Allows up to $10,000 in interest paid on qualifying U.S. passenger vehicle loans from U.S. lenders. This is the only OBBBA deduction available if you’re married filing separately.

Why expats can’t use it: Loans from foreign banks aren’t eligible. Unless you maintain a U.S.-based vehicle with a U.S. lender, this deduction won’t apply.

4. Enhanced Senior Deduction

Adds up to $6,000 per taxpayer born before January 2, 1961 (up to $12,000 for joint filers). The deduction phases out starting at $150,000 MAGI (single) or $250,000 MAGI (joint).

Why some expats may lose out: Even if you exclude income with FEIE, those amounts are added back into MAGI for this deduction, pushing many retirees abroad above the threshold.

Learn more about U.S. Expat Deductions and Credits.

The Expat Angle: Why MAGI Calculations Matter Most

Here’s what makes Schedule 1-A significant for expats, even if you can’t claim the deductions:

Excluded Income Still Counts Toward MAGI

Schedule 1-A explicitly requires adding back amounts excluded under:

- The Foreign Earned Income Exclusion (Form 2555)

- The Puerto Rico exclusion

- The American Samoa exclusion

This means even if your foreign earned income isn’t taxed thanks to the FEIE, it still raises your Modified Adjusted Gross Income, which can phase you out of these new deductions.

Real-World Example:

Sarah, age 62, retired in Portugal:

- Foreign pension income: $95,000

- Uses FEIE to exclude $95,000 from U.S. taxation

- MAGI for Schedule 1-A purposes: $95,000 (excluded amount added back)

- Below the $150,000 phaseout threshold

- Could potentially claim the $6,000 senior deduction

John, age 63, retired in France:

- Foreign pension income: $160,000

- Uses FEIE to exclude $130,000 from U.S. taxation

- MAGI for Schedule 1-A purposes: $160,000 (entire amount added back)

- Above the $150,000 phaseout threshold

- Senior deduction begins phasing out, and receives a reduced benefit

Most Working Expats Won’t Benefit

The tips and overtime deductions require U.S. employer reporting systems that simply don’t exist abroad. Foreign employers:

- Don’t classify compensation as “tips” or “overtime” under U.S. law

- Don’t issue W-2s with proper U.S. payroll codes

- Aren’t subject to Fair Labor Standards Act overtime rules

- Can’t withhold U.S. Social Security and Medicare taxes

Even if you receive tips or work overtime abroad, without U.S.-compliant documentation, you can’t claim these deductions.

Related: 3 Tax Deductions for Tips, Overtime, and More That Expats Can’t Use

Using Schedule 1-A for Your 2025 Tax Return

Now that Schedule 1-A is finalized, here’s what expats need to know about filing:

Who Must File Schedule 1-A:

You’ll need to file Schedule 1-A if you’re claiming any of the four OBBBA deductions. Most expats will skip this form entirely because:

- Tips and overtime deductions require U.S. employer W-2 reporting

- Car loan interest requires U.S.-based vehicle financing

- Senior deduction may be phased out due to MAGI calculations

When to File:

Schedule 1-A is filed with your Form 1040 by these deadlines:

- April 15, 2026: Standard filing deadline

- June 15, 2026: Automatic extension for Americans living abroad (no forms required)

- October 15, 2026: Final deadline with Form 4868 extension

How It Works with Other Forms:

Schedule 1-A totals flow to your Form 1040, line 2. If you’re also filing:

- Schedule 1 for additional income and adjustments

- Form 2555 for the Foreign Earned Income Exclusion

- Form 1116 for Foreign Tax Credit

All of these forms work together, and excluded income from Form 2555 gets added back when calculating MAGI for Schedule 1-A eligibility.

Understanding the Form Confusion: Schedule A vs. Schedule 1 vs. Schedule 1-A

With three similarly named schedules, it’s easy to get confused. Here’s what each form does:

1. Schedule A (Form 1040)

- Purpose: Itemized deductions

- Covers: Mortgage interest, state/local taxes, charitable contributions, medical expenses

- Who Uses It: Taxpayers who itemize instead of taking the standard deduction

- Status: Permanent form, updated annually

2. Schedule 1 (Form 1040)

- Purpose: Additional income and adjustments to income

- Covers: Business income, rental income, unemployment, student loan interest, IRA contributions, foreign housing deduction

- Who Uses It: Taxpayers with income sources beyond W-2s or valuable above-the-line deductions

- Status: Permanent form, updated annually

3. Schedule 1-A (Form 1040)

- Purpose: OBBBA deductions only

- Covers: Tips, overtime, car loan interest, and senior deduction

- Who Uses It: Taxpayers qualifying for one or more of the four OBBBA deductions

- Status: NEW in 2025, temporary (expires after 2028)

Schedule 1-A is not an update or replacement for Schedule 1 or Schedule A. It’s a completely separate form that works alongside them.

For comprehensive guidance on Schedule 1 (the main form for additional income and adjustments), see our complete Schedule 1 filing guide.

Don’t Miss Newly Created Adjustments

Strategic Implications for Expats

Who Might Actually Benefit:

Retirees abroad with moderate income:

- Born before January 2, 1961

- Total foreign income (including excluded amounts) under $150,000 (single) or $250,000 (joint)

- Could claim the enhanced $6,000/$12,000 senior deduction

Expats maintaining U.S. vehicle loans:

- Financed through U.S. lenders

- Could deduct up to $10,000 in car loan interest

- Rare situation for full-time expats

Who Won’t Benefit:

Working expats with foreign employers:

- Cannot claim tips or overtime deductions without a U.S. employer reporting

- Foreign payroll systems don’t generate the required documentation

High-earning expats:

- FEIE exclusions added back to MAGI

- Likely to exceed $150,000/$250,000 thresholds

- Senior deduction phases out or disappears entirely

Expats without U.S.-based loans:

- Foreign vehicle loans don’t qualify

- Car loan interest deduction unavailable

What Should Expats Do Now?

1. Determine If Schedule 1-A Applies to You

Most expats can skip this form. You only need Schedule 1-A if you:

- Are 62 or older with total income (including excluded amounts) under the MAGI thresholds

- Maintain a U.S. vehicle loan through a U.S. lender

- Have U.S. employer-reported tips or overtime (rare for expats)

2. Focus on Proven Expat Tax Strategies

Rather than counting on limited OBBBA deductions, expats should maximize existing, reliable tax benefits:

- Foreign Earned Income Exclusion (FEIE): Exclude up to $130,000 of foreign earned income (2025 tax year)

- Foreign Tax Credit (FTC): Dollar-for-dollar credit for foreign taxes paid

- Foreign Housing Deduction: Available for self-employed expats on Schedule 1

- Totalization Agreements: Avoid double Social Security taxation

3. Understand Your Complete Filing Picture

Schedule 1-A is just one small piece of expat tax filing. For comprehensive guidance on Schedule 1 (which most expats actually need) and Schedule 1-A, see our Schedule 1 complete filing guide.

4. Calculate Your True MAGI

If you’re a senior expat potentially eligible for the enhanced deduction, remember that your MAGI includes excluded foreign income added back. Run the numbers before assuming eligibility.

5. Get Professional Help

The interaction between Schedule 1-A, FEIE, and MAGI calculations can be complex. Greenback’s expat tax specialists can review your specific situation and determine whether any OBBBA deductions apply to you.

Ready to make sure you’re covered? Get started with Greenback today and let our expat tax experts handle the details for you.

Frequently Asked Questions About Schedule 1-A

Is Schedule 1-A final?

Yes. The IRS has finalized Schedule 1-A, and it’s available for use starting with the 2025 tax year (filed in 2026).

When will I first use it?

With your 2025 tax return, filed in 2026. You’ll only file it if you qualify for one or more of the four OBBBA deductions.

Does Schedule 1-A change how FEIE works?

No, the FEIE functions the same way. However, excluded income is counted toward MAGI when determining eligibility for the four OBBBA deductions on Schedule 1-A.

Are the deductions permanent?

No. Under OBBBA, these deductions are temporary and currently set to expire after the 2028 tax year. Congress would need to pass new legislation to extend them.

Do I still need to file Schedule 1?

Yes. Schedule 1 continues to be required for reporting additional income (like business income, rental income, or unemployment) and claiming adjustments to income (like student loan interest, IRA contributions, or the foreign housing deduction). Schedule 1-A is a separate, additional form.

What if I’m married filing separately?

Only the car loan interest deduction is available when married filing separately. The tips, overtime, and senior deductions are not allowed for MFS filers.

The Bottom Line: Policy Over Practice for Most Expats

Schedule 1-A represents a significant structural addition to the U.S. tax system, but for most American expats, it’s more about understanding policy implications than claiming actual deductions.

Key Takeaways:

- Schedule 1-A is a new, temporary form created for OBBBA deductions (2025-2028)

- Most working expats can’t use tips/overtime deductions due to foreign employer reporting requirements

- MAGI calculations include excluded income, potentially phasing out the senior deduction

- The senior deduction may benefit retirees abroad with moderate total income

- Car loan interest only applies to U.S.-based vehicle financing

- The form is now finalized and ready for use in the 2026 filing season

For comprehensive guidance on the forms you’ll actually need (like Schedule 1 for additional income and adjustments), see our complete Schedule 1 filing guide.

Get Expert Help with Your Expat Taxes

Greenback is an American company founded in 2009 by U.S. expats. We’ve been helping Americans get their taxes done right for over 15 years, and many of our CPAs and Enrolled Agents are expats themselves, living in 14 time zones and experiencing firsthand the challenges of filing from abroad.

Whether Schedule 1-A applies to you or not, our team can help you navigate the complete expat tax filing process from FEIE to Foreign Tax Credits to business income reporting.

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on U.S. expat taxes or working with Greenback, contact our Customer Champions.

Schedule 1-A changes may apply to your foreign income.

This article is for informational purposes only and should not be considered tax advice. Tax laws change frequently, and individual circumstances vary. Please consult with a qualified tax professional for advice specific to your situation.