Form 2555 for Expats: Line-by-Line Instructions to Claim the FEIE

- Documents You'll Need to File Form 2555

- Before You Start: Which Parts Will You Complete?

- Part I: General Information

- Part II: Bona Fide Residence Test (Complete Part II OR Part III)

- Part III: Physical Presence Test (Complete Part II OR Part III)

- Part IV: All Taxpayers - Foreign Earned Income

- Part V: All Taxpayers

- Part VI: Housing Exclusion and Deduction

- Part VII: Figuring the Foreign Earned Income Exclusion

- Parts VIII and IX: Housing Exclusion and Deduction

- Common Form Completion Errors

- Where to Get Form 2555 and How to File

- Let Greenback Handle Your Form 2555

Form 2555 is the IRS form you must file to claim the Foreign Earned Income Exclusion (FEIE), allowing you to exclude up to $130,000 of foreign-earned income for the 2025 tax year.

This guide provides step-by-step, line-by-line instructions for completing Form 2555. The form has nine parts, but you’ll only complete the sections that apply to your situation. Whether you qualify under the bona fide residence test or the physical presence test determines which parts you’ll fill out.

Before starting, make sure you’ve gathered employer information, detailed travel records, income documentation, and, if you’re claiming housing benefits, housing expense receipts. For an overview of who needs Form 2555 and whether you qualify, see our complete Form 2555 guide.

You Can Complete Form 2555 Without Guesswork

This line-by-line walkthrough shows you exactly what information goes on each line and how to calculate the amounts.

Documents You’ll Need to File Form 2555

Have these ready before starting the form:

- Employer names and addresses (foreign and U.S.)

- Complete travel calendar with entry/exit dates for all countries

- Foreign income statements (payslips, W-2s, or foreign equivalents)

- Previous Form 2555 (if filed before)

- Housing expense receipts (rent, utilities, insurance) if claiming housing benefits

- Foreign tax payment records

Critical: Each spouse must file their own separate Form 2555 if both qualify. Even when filing jointly, complete two separate forms.

Before You Start: Which Parts Will You Complete?

Form 2555 has nine parts, but you won’t fill out all of them. Here’s what you need to know:

Everyone completes:

- Part I (General Information)

- Part IV (All income)

- Part V (Transition section)

- Part VII (Calculating your exclusion)

Complete Part II OR Part III (not both):

- Part II: if using bona fide residence test

- Part III: Using the physical presence test

For help deciding which test you qualify for, see our guide on bona fide residence vs physical presence.

Complete only if applicable:

- Part VI (Housing exclusion/deduction) – if you had foreign housing expenses

- Part VIII (Housing exclusion calculation) – if claiming housing exclusion

- Part IX (Housing deduction) – if self-employed with housing deduction

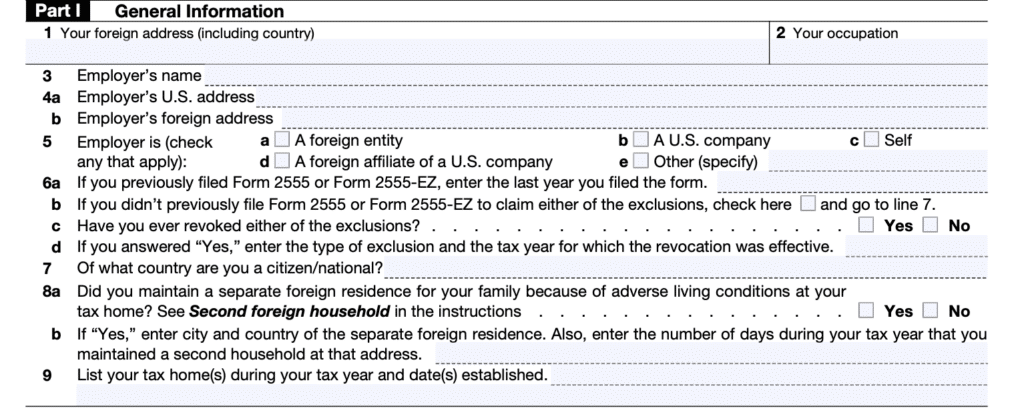

Part I: General Information

This straightforward section asks for basic details:

- Lines 1-4: Your name, Social Security Number, and information about your employer(s)

- Line 5: If your employer is a foreign entity, indicate whether it’s:

- A foreign entity

- A U.S. company

- A foreign affiliate of a U.S. company

- Line 6a: Check “Yes” if you filed Form 2555 or 2555-EZ in a previous year. Enter the most recent year.

- Line 6b: Check this box if you’ve never claimed the FEIE before.

- Line 6c-d: Only complete if you previously claimed the FEIE but then revoked it. Most expats will leave this blank.

- Line 7: Your occupation abroad (examples: “software engineer,” “English teacher,” “consultant”)

- Line 8: List your employer’s name and foreign address

- Lines 9a-d: Complete if you maintained a separate residence for your family due to adverse living conditions. This is rare and applies when your work location is dangerous or lacks basic infrastructure, so your family lives elsewhere.

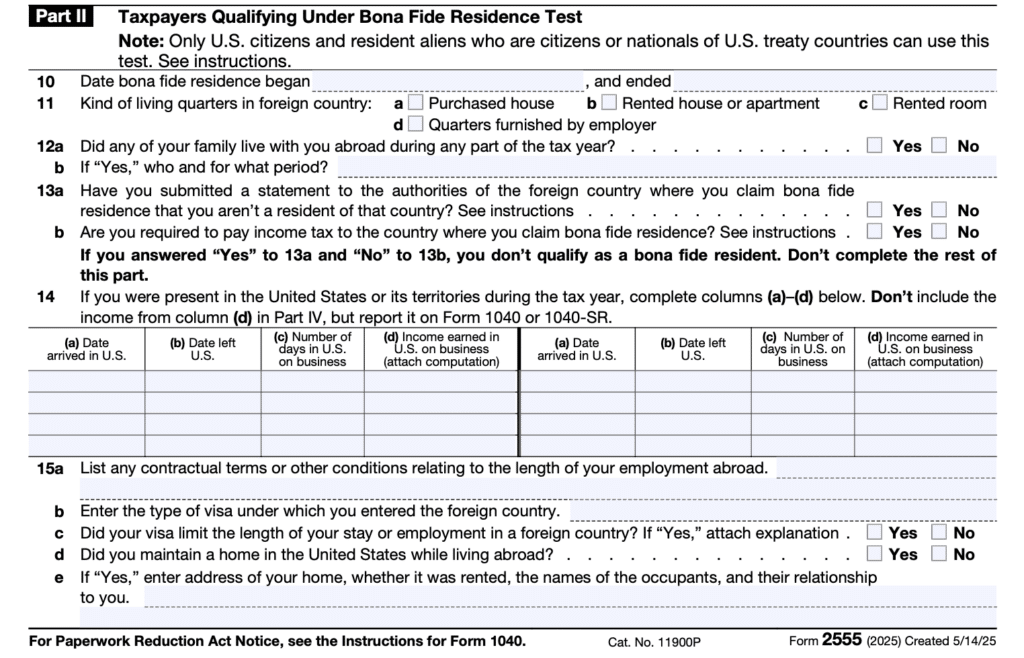

Part II: Bona Fide Residence Test (Complete Part II OR Part III)

Skip to Part III if you’re using the physical presence test instead.

- Line 11: Date you arrived and established bona fide residence

- Example: If you moved to Germany on March 15, 2024, and established residence, enter “03/15/2024”

- Line 12a: Your complete foreign address

- Line 12b: Type of living quarters

- “Rented apartment”

- “Owned house”

- “Company-provided housing”

- Line 13a: Did family members live with you abroad?

- Check “Yes” or “No”

- Line 13b: Are you required to pay income tax in the foreign country?

- Check “Yes” or “No”

- Critical: If you answered “Yes” to 13a and “No” to 13b, you don’t qualify under this test. Use Part III instead.

- Line 14a-c: Enter details about your visa or residence permit

- Type of visa (e.g., “work visa,” “resident permit”)

- Whether it limits your length of stay

- Any contractual employment terms

- Lines 15a-d: U.S. Trips During the Tax Year

- If you visited the U.S. during the year, complete this table for EACH trip:

- Column (a): Dates in U.S. (e.g., “06/15/2025 to 06/22/2025”)

- Column (b): Number of days in the U.S. (“7 days”)

- Column (c): Income earned while in the U.S. (calculate based on daily rate)

- If you visited the U.S. during the year, complete this table for EACH trip:

How to calculate U.S.-earned income: If your annual salary is $100,000 and you worked 7 days in the U.S.:

- Daily rate: $100,000 ÷ 365 = $274/day

- U.S. income: $274 × 7 days = $1,918

This amount is NOT foreign earned income and cannot be excluded. Report it separately.

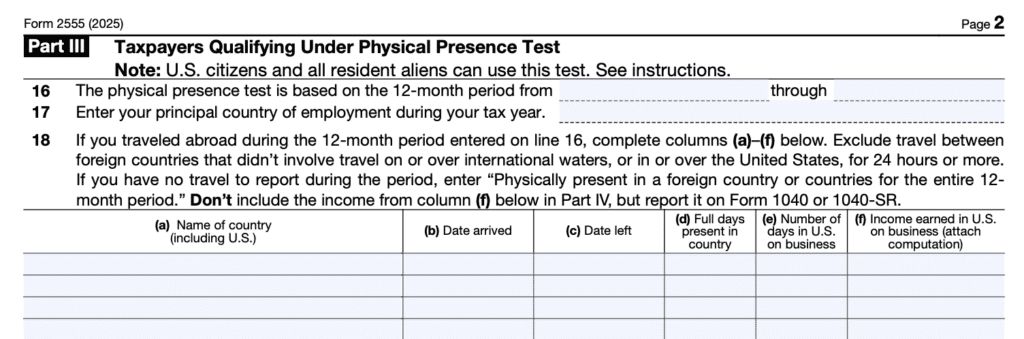

Part III: Physical Presence Test (Complete Part II OR Part III)

Skip this if you completed Part II.

- Line 16: The 12-month period you’re using to qualify

- Enter dates strategically. The period doesn’t have to be the calendar year.

- Example: “06/01/2025 to 05/31/2026”

- Line 17: Principal country of employment

- Example: “Thailand,” “Spain,” “Japan”

- Lines 18a-f: Travel Table

- Complete this table showing EVERY day of your 12-month qualifying period:

- Column (a) – Name of country (including the U.S.):

- List each country you visited

- List countries in chronological order

- Include the U.S. for any trips home

- Column (b) – Date arrived:

- Format: MM/DD/YYYY

- The first entry should be the start of your 12-month period

- Column (c) – Date left:

- Format: MM/DD/YYYY

- Last entry should be the end of your 12-month period

- Column (d) – Full days present:

- Count only FULL days (entire 24-hour periods)

- Travel days don’t count as full days

- Example: Arrived July 1, left July 5 = 3 full days (July 2, 3, 4)

- Column (e) – Number of days in U.S.:

- Transfer days from column (d) when the country is “United States.”

- Column (f) – Income earned in U.S.:

- Calculate based on the daily rate

- Example: $100,000 salary ÷ 365 = $274/day × days in US

No travel example: If you spent the entire 12 months in one country with no travel, write: “Physically present in a foreign country or countries for the entire 12-month period.”

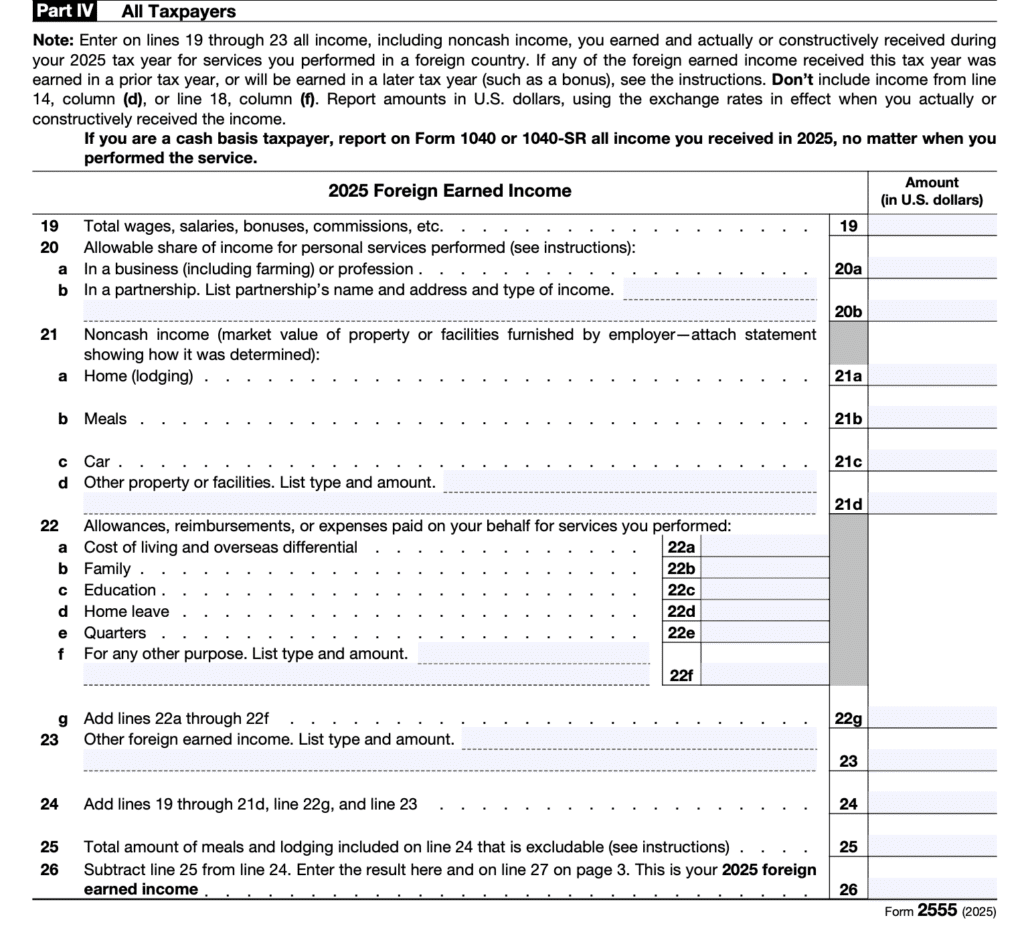

Part IV: All Taxpayers – Foreign Earned Income

Everyone completes Part IV to report total foreign earned income.

- Line 19: Total wages, salaries, bonuses, and commissions

- Line 20a-b: Business or self-employment income (Schedule C filers)

- Line 21: Allowances, reimbursements, or noncash income, including:

- Housing provided by the employer

- Cost-of-living allowances

- Overseas differential pay

- Education allowances for dependents

- Line 22: Other foreign earned income (specify the type)

- Line 23: Total foreign earned income before meal/lodging exclusion

- Line 24: Noncash meals and lodging are excluded under different rules

- Line 25: Enter the amount from line 24

- Line 26: Your total foreign-earned income (line 23 minus line 25)

- This amount flows to Part V, line 27.

What About US-Earned Income?

If you worked in the U.S. during the tax year (shown in Part II, line 15 or Part III, line 18), that income is NOT foreign earned income.

You must:

- Calculate the U.S. portion based on days worked

- Attach a statement showing your calculation

- Report the U.S. income on your Form 1040, but NOT include it in Part IV of Form 2555

Part V: All Taxpayers

- Line 27: Enter the amount from line 26 (your total foreign earned income)

- Line 27 question: Are you claiming the housing exclusion or housing deduction?

- If NO: Skip Parts VI, VIII, and IX. Go directly to Part VII to calculate your exclusion.

- If YES: Complete Part VI next.

Most expats who rent or own a home abroad can claim some housing benefits, so answer “Yes” if you have housing expenses.

Not All Income Belongs on Form 2555

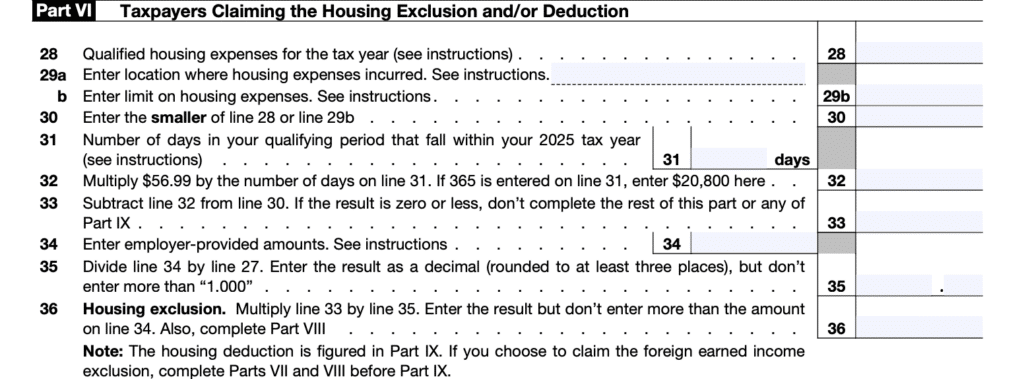

Part VI: Housing Exclusion and Deduction

Complete this section only if you answered “Yes” to the question on line 27.

- Line 28: Total qualified housing expenses for the year, including:

- Rent or mortgage interest

- Utilities (except telephone)

- Real and personal property insurance

- Residential parking

- Furniture rental

- Do NOT include:

- Mortgage principal

- Domestic labor (maids, gardeners)

- Purchased furniture

- Lavish or extravagant expenses

- Deductible interest and taxes

- Line 29a: City and country where you incurred housing expenses

- Line 29b: Your housing expense limit based on location

- For 2025, the standard limit is $39,000 ($130,000 × 30%). However, certain high-cost cities have higher limits. Check the IRS housing expense table for cities such as London, Tokyo, Hong Kong, and Singapore.

- Line 30: Enter the smaller of line 28 or line 29b

- Line 31: Number of qualifying days in your 2025 tax year

- If you qualified for the entire year, enter 365 (or 366 for leap years). If you qualified for part of the year, enter only the qualifying days.

- Line 32: Base housing amount ($56.99 × line 31)

- For a full year, this equals $20,800 ($56.99 × 365 days). This is the amount of housing the IRS considers “normal” and not excludable.

- Line 33: Your total housing amount (line 30 minus line 32)

- This is the excess housing you can potentially exclude or deduct.

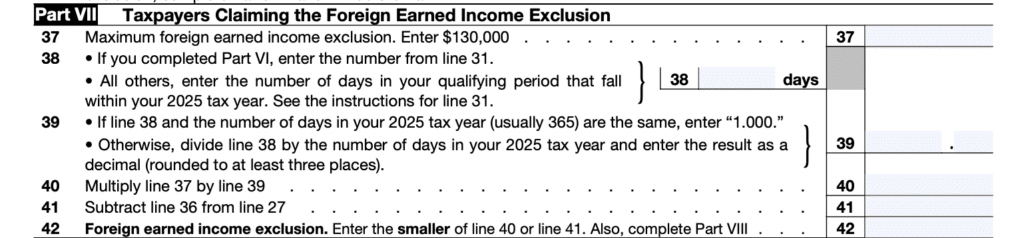

Part VII: Figuring the Foreign Earned Income Exclusion

This is where you calculate your actual FEIE amount.

- Line 37: Maximum FEIE for 2025: $130,000

- This is pre-filled by the IRS. For 2026, this will be $132,900.

- Line 38: Number of qualifying days in your 2025 tax year

- This should match line 31 if you’re claiming housing. If you qualified for the entire year, enter 365.

- Line 39: Calculate your qualifying fraction

- Divide line 38 by the number of days in the tax year (usually 365):

- Full year: 365 ÷ 365 = 1.000

- Partial year (moved abroad in July): 184 ÷ 365 = 0.504

- Line 40: Your prorated maximum exclusion

- Multiply line 37 by line 39.

- Example: 0.504 × $130,000 = $65,520

- Line 41: Your total foreign earned income from line 27

- Line 42: Your foreign earned income exclusion

- Enter the SMALLER of line 40 or line 41.

Example Calculation:

Maria moved to Brazil on August 1, 2025, and qualified under the bona fide residence test. She earned $48,000 working as a dancer from August through December.

- Line 38: 153 days (August 1 – December 31)

- Line 39: 153 ÷ 365 = 0.419

- Line 40: 0.419 × $130,000 = $54,470

- Line 41: $48,000

- Line 42: $48,000 (the smaller amount)

Maria can exclude her entire $48,000 because it’s less than her prorated maximum.

- Line 43: Total exclusions (add lines 36 and 42 if claiming housing)

- If not claiming housing, line 43 equals line 42.

- Line 44: Enter the amount from line 27 (total foreign earned income)

- Line 45: Your foreign-earned income after exclusions

- Subtract line 43 from line 44. Enter this amount on Schedule 1 (Form 1040), line 8d, as a negative number.

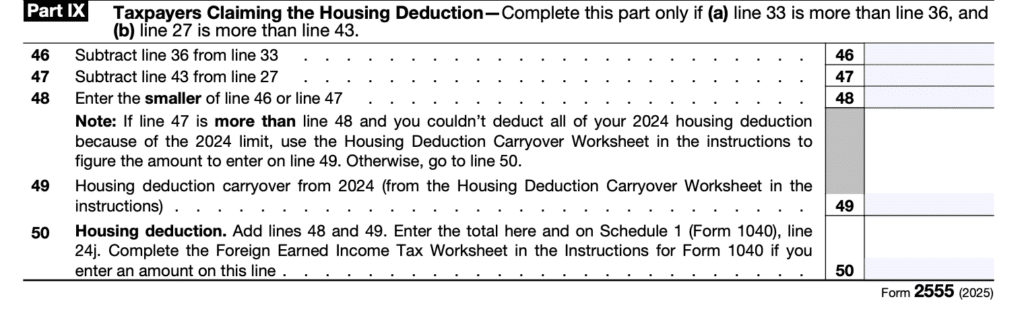

Parts VIII and IX: Housing Exclusion and Deduction

Complete Part VIII if you completed Part VI and are claiming the housing exclusion.

- Line 46: Enter the amount from line 33 (total housing amount)

- Line 47: Maximum housing exclusion limitation (varies based on income and exclusion amounts)

- Follow the form’s calculations using your foreign-earned income and FEIE.

- Line 48: Housing exclusion (the smaller of line 46 or line 47)

- This is your additional exclusion beyond the FEIE, up to your eligible housing costs.

Complete Part IX only if you’re self-employed and have a housing deduction (less common).

Common Form Completion Errors

- Line 38 doesn’t match line 31: the numbers should be the same (qualifying days). If they don’t match, your calculation will be wrong.

- Counting travel days as full days: The day you depart and the day you arrive are NOT full days.

- Including passive income in Part IV: Only earned income (wages, salaries, self-employment) goes on Form 2555.

- Not calculating U.S. income separately: Income earned while physically in the U.S. must be excluded from Part IV and reported separately on Form 1040.

- Wrong 12-month period on line 16: Choose your period strategically, especially for partial years abroad.

- Forgetting housing base amount: Line 32 reduces your housing exclusion by the base amount ($56.99/day for 2025).

- Not attaching the form to Form 1040: Form 2555 must be attached to your return. Without it attached, you can’t claim the exclusion.

For comprehensive guidance on common mistakes and tax strategy, see our complete Form 2555 guide.

Where to Get Form 2555 and How to File

Download Form 2555 from the IRS website. The official IRS instructions provide additional detail for complex situations.

How to file:

- Complete Form 2555

- Attach it to your Form 1040 or 1040-SR

- The exclusion from line 45 flows to Schedule 1 (Form 1040), line 8d

- Mail to the special IRS address for Form 2555 filers (see Form 1040 instructions)

Do NOT mail to your state’s address. Form 2555 filers use a different IRS processing center.

For filing deadlines, extensions, and late filing options, see our complete Form 2555 guide.

Let Greenback Handle Your Form 2555

Form 2555 requires careful attention to dates, accurate income calculations, and proper documentation. One mistake in counting qualifying days can disqualify your entire exclusion.

Greenback Expat Tax Services has deep expertise in expat taxes and Form 2555 preparation. We’re an American company founded in 2009 by U.S. expats for expats. We’ve helped 23,000+ expats file 71,000+ returns while maintaining a 4.9-star rating across 1,200+ TrustPilot reviews.

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on U.S. expat taxes or working with Greenback, contact our Customer Champions.

Make Sure Form 2555 Is Actually Saving You Money

Disclaimer: This article provides general information about Form 2555 and the Foreign Earned Income Exclusion. Tax laws are complex and subject to change. For advice specific to your situation, consult with a qualified tax professional.