Should You Check the Virtual Currency Checkbox on Form 1040?

- What Is Virtual Currency?

- How Does the IRS Tax Virtual Currency?

- Should I Check the Virtual Currency Checkbox on Form 1040?

- Do I Have to Report Virtual Currency on My FBAR?

- What If I Fail to Report My Virtual Currency Activity?

- What Are Some Best Practices for Using Virtual Currency?

- Virtual Currency Reporting Doesn't Have to Be Complicated

Navigating the digital age, virtual currency has emerged as a pivotal player in online transactions. More than just digital tokens, these currencies open doors to a world of internet-based trading and purchases, bridging the gap between traditional fiat currency and the evolving digital economy.

As it gains traction, it poses unique challenges and opportunities, especially when it comes to tax implications. This raises a crucial question for taxpayers: Should you check the virtual currency checkbox on Form 1040? Unraveling this query is key to understanding the intersection of digital assets and fiscal responsibility.

Key Takeaways

- The term digital asset is now what the IRS refers to as what is commonly known as virtual currency or cryptocurrency. For purposes of this article, we will use all three terms interchangeably.

- Virtual currency serves the same purpose as traditional money in representing value in a digital form.

- Even real-world goods and services can be exchanged for virtual currency in some situations, much like the US dollar.

What Is Virtual Currency?

Virtual currency is a form of digital currency that can be used to make purchases on the Internet. It can also be traded for other virtual currencies, as well as fiat currency which is the real-world paper currency we are all accustomed to using.

The best-known types are cryptocurrencies such as Bitcoin and Ethereum.

While virtual currency has faced plenty of criticism over the years, there’s no denying that it has become a powerful force in the global economy. Whether you accept or pay with cryptocurrency, invest in it, are an experienced currency trader, or receive a small amount as a gift, it’s important to understand the tax implications of your situation.

How Does the IRS Tax Virtual Currency?

The IRS regards virtual currencies as property for taxation purposes, meaning general principles for property transactions also apply here. The tax classification of your virtual currency—whether as personal, business, or investment property—depends on its specific usage, influencing how it’s taxed. This approach aligns digital asset handling with traditional property tax guidelines.

Let’s look at some common transactions and how they might be taxed.

1. Buying Virtual Currency

Purchasing digital assets with traditional currencies (like the US dollar) and storing them in an electronic wallet or account doesn’t constitute a taxable event and doesn’t require reporting. Similarly, transferring these assets between your own wallets or accounts also falls outside the realm of taxable transactions.

If you sell, trade or dispose of cryptocurrency investments in any way that causes you to recognize a gain in taxable accounts, you must report that gain as taxable income. This does not apply if you trade cryptocurrency in a tax-deferred or tax-free account like an individual retirement account (IRA).

According to the IRS, converting one type of digital asset into another is seen as two separate transactions: a sale of the first and a purchase of the second. This approach impacts how these exchanges are viewed for tax purposes.

2. Mining Virtual Currency

“Mining” is a complicated process used to gain new virtual currencies. This process is especially associated with mining Bitcoin.

If you successfully mine a virtual currency, you must report it as income. To value this income, use the fair market value of that currency on the day you received it.

In addition to this, if you mined the virtual currency as part of your own trade or business, it will be considered business property. If you earn cryptocurrency by mining it, the income is taxable and must be reported on Form 1099-NEC. You must report this even if you don’t receive a 1099 form as the IRS considers this taxable income and is likely subject to self-employment tax in addition to income tax.

3. Being Paid for Goods and Services

If someone pays you cryptocurrency in exchange for goods or services, the payment counts as taxable income, just as if they’d paid you via cash, check, credit card, or digital wallet.

For tax reporting purposes, you must include the dollar value of the cryptocurrency in U.S. dollars on the day it was received or determine your taxable income for the goods or services you provided.

4. Selling Virtual Currency

When you sell or spend cryptocurrency you have a capital transaction resulting in a gain or loss just as you would if you sold shares of stock. When disposing of cryptocurrency, it’s necessary to report each sale on your tax return.

Keeping good records of what your actual cost was for each virtual currency is a crucial part of correctly reporting sales on your tax return. You are required to keep track of and accurately report all purchases and sales. This is ultimately your responsibility regardless of whether or not the virtual currency exchanges provide you with incorrect or incomplete information.

5. Receiving Virtual Currency as Payment for Work Performed

If you receive virtual currency as payment for wages or salaries,, you must report it as income. This applies whether you are being paid for work as an employee or independent contractor.

To value your payment, use the fair market value of that currency on the day you received it.

6. Paying Employees or Independent Contractors

If you use virtual currency to pay an employee’s wages or an independent contractor’s fee, it will be subject to the same tax and reporting as any other payment made using property.

- If you are paying an employee with virtual currency, the payment will be subject to the federal wage withholding tax as well as FICA and FUTA taxes.

- If you are paying an independent contractor, you may have to report this payment on form 1099-NEC to the IRS and the independent contractor.

Once again, to value this transaction, use the fair market value of that currency on the day you paid it to an employee or contractor.

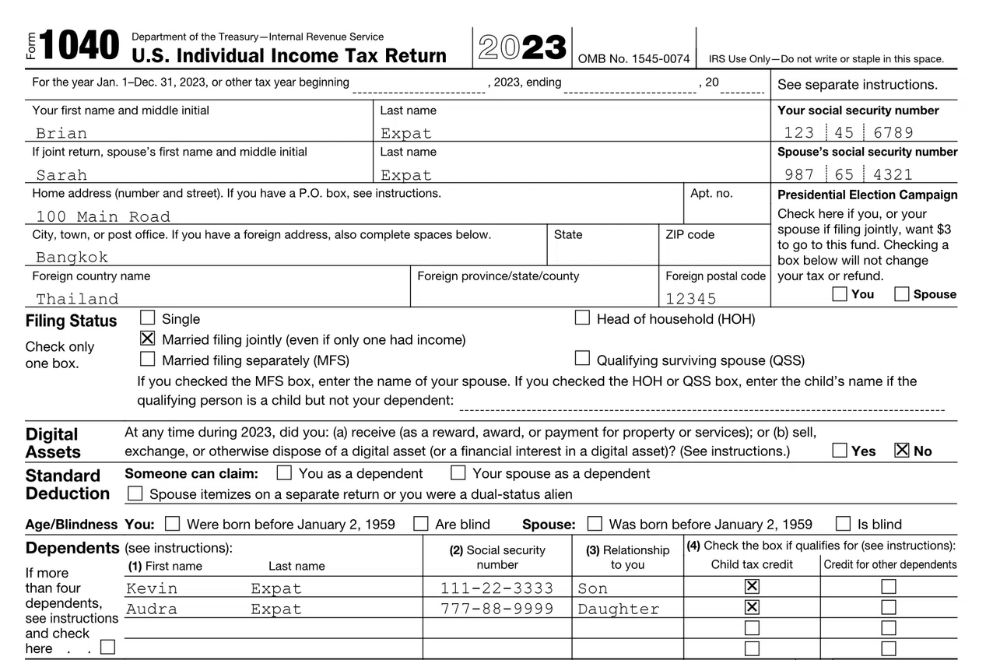

Should I Check the Virtual Currency Checkbox on Form 1040?

You should check the virtual currency checkbox on Form 1040 if you’ve engaged in a reportable transaction involving digital assets. Reportable transactions encompass a range of activities including the sale of these assets, their use in purchasing goods or services, receiving them as payment, mining activities, trading one digital asset for another, and acquiring them through methods such as airdrops.

If you have taken part in any of these transactions, you should check “Yes” on the virtual currency checkbox on Form 1040.

Non-reportable transactions for digital assets include purchasing them, holding them without selling or exchanging them, and transferring them between wallets or accounts you own. These activities do not require reporting on Form 1040.

If you have only taken part in transactions like these, you should check “No” on the checkbox on Form 1040.

This advice is generalized, and there’s a lot of nuance involved in virtual currency taxations. We recommend consulting a tax professional if you’ve engaged with virtual currency at all during the year. Failing to meet your reporting requirements could result in severe penalties.

Do I Have to Report Virtual Currency on My FBAR?

All US citizens with at least $10,000 in one or more non-US bank accounts must report it by filing a Foreign Bank Account Report (FBAR). Naturally, many Americans living abroad are required to file this form.

But what if you have $10,000 in virtual currency stored in a foreign account or exchange? Do you have to report that too? As it stands, the answer appears to be no. According to FinCEN Notice 2020-2, taxpayers are not required to report foreign wallets, exchanges, or accounts holding only this asset.

However, the same notice states that this rule may change in the future. Check back with us for further updates.

What If I Fail to Report My Virtual Currency Activity?

If you fail to report your virtual currency activity when required, you could face a range of penalties, including an IRS audit, incurred interest, or tax penalties. But there are still several ways in which you could avoid incurring penalties.

The first step is contacting the IRS and disclosing your failure to report income accurately. This might allow you to enter into an agreement with the IRS that may reduce or eliminate any penalties. If the IRS believes that you have intentionally avoided reporting virtual currency activity, they may impose additional penalties. This could include a higher accuracy-related penalty or even criminal prosecution.

What Are Some Best Practices for Using Virtual Currency?

To ensure compliance with tax regulations when using virtual currency, it is crucial to maintain comprehensive records. The following information should be recorded:

- The date you received the virtual currency

- How you receive the virtual currency (payment of wages, for selling goods, etc.)

- The fair market value of the currency on the day you received it

- The purpose for which you are holding the currency (e.g., investment or business use)

- The date you sold or exchanged the virtual currency

- The fair value of the currency on the date you sold or exchanged it

It is highly recommended to seek the advice of a tax professional to assist with remaining tax compliant.

Virtual Currency Reporting Doesn’t Have to Be Complicated

We hope this guide has helped you understand virtual currency—and whether you should check the Form 1040 virtual currency checkbox. If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

Featured In