U.S. Gift Tax for Americans Abroad: Guide to Giving and Receiving

- Two Forms, Two Scenarios

- Quick Reference: Gift Tax Thresholds at a Glance

- Part 1: When You GIVE Gifts (Form 709)

- What Is the U.S. Gift Tax?

- When Do I Actually Owe Gift Tax?

- How to File Form 709: U.S. Gift Tax Return

- Common Gift Tax Scenarios for Expats (Giving Gifts)

- Part 2: When You RECEIVE Gifts (Form 3520)

- What Is a Foreign Gift?

- When Must I Report Receiving a Foreign Gift?

- Are Foreign Gifts Taxable?

- How to File Form 3520 for Foreign Gifts

- Common Foreign Gift Scenarios (Receiving Gifts)

- Penalties for Failing to Report Gifts

- Special Rules and Exceptions

- Gift Tax Planning Strategies for Expats

- Common Gift Tax Mistakes to Avoid

- How Greenback Can Help

- Related Resources

According to the IRS, Americans must report foreign gifts exceeding $100,000, but here’s the relief: these gifts aren’t taxed. The U.S. gift tax system works differently than most countries, with separate reporting rules depending on whether you’re giving or receiving a gift.

Two Forms, Two Scenarios

For Americans living abroad, gift tax rules create confusion because two separate scenarios require different forms:

| Your Situation | Form to File | When Required |

|---|---|---|

| You GIVE a gift (to anyone, anywhere) | Form 709 | When you give more than $19,000 to one person in a year |

| You RECEIVE a gift (from a foreign person) | Form 3520 | When you receive more than $100,000 from foreign individuals (refers to aggregate gifts during the tax year from foreign individuals or estates) |

Mixing up these forms or missing filing requirements can trigger penalties up to 25% of the gift value.

In this guide, you’ll learn:

- Exact dollar thresholds for 2025 and 2026

- Which form applies to your situation

- Step-by-step filing instructions

- How to avoid costly penalties

- Strategic planning to minimize reporting

Quick Reference: Gift Tax Thresholds at a Glance

When You GIVE a Gift (Form 709)

| Gift Type | 2025 Tax Year Limit | 2026 Tax Year Limit | What This Means |

|---|---|---|---|

| Annual exclusion (per person) | $19,000 | $19,000 | Give this amount to unlimited recipients without filing |

| Married couple (combined) | $38,000 | $38,000 | Double the exclusion through gift splitting |

| Non-U.S. citizen spouse | $190,000 | $194,000 | Special higher limit for foreign spouses |

| Lifetime exemption (individual) | $13.99M | $15M | Total you can give over your lifetime tax-free |

| Lifetime exemption (married) | $27.98M | $30M | Combined exemption for couples |

Pro Tip

Pro TipThe annual exclusion resets every January 1. You could give someone $19,000 on December 31, 2025, and another $19,000 on January 1, 2026, without ever filing Form 709.

Worried a foreign gift might trigger IRS reporting?

When You RECEIVE a Gift (Form 3520)

| Gift Source | 2025 Threshold | 2026 Threshold | Must Report? |

|---|---|---|---|

| Foreign individual or estate | $100,000+ | $100,000+ | Yes |

| Foreign corporation/partnership | $20,116+ | TBD* | Yes |

| U.S. person (even from abroad) | Any amount | Any amount | No |

| Covered expatriate | Over $19,000 | Over $19,000 | Yes + tax may apply |

*Adjusted annually for inflation

Take NoteA “foreign person” means the donor’s citizenship status, not where the money came from. A U.S. citizen wiring money from London is NOT a foreign person.

Part 1: When You GIVE Gifts (Form 709)

Quick Answer: Do I Need to File Form 709?

File Form 709 if:

- ✓ You gave more than $19,000 to any one person in 2025 or 2026

- ✓ You gave more than $190,000/$194,000 to your non-U.S. citizen spouse

- ✓ You’re married and want to split gifts with your spouse (even under limits)

Don’t file Form 709 if:

- ✗ All your gifts were under $19,000 per person

- ✗ You only gave to your U.S. citizen spouse

- ✗ You paid tuition/medical bills directly to institutions

- ✗ You only gave to charities

What Is the U.S. Gift Tax?

The U.S. gift tax is a federal tax on transfers of money or property to another person when you don’t receive equal value in return. The person giving the gift is responsible for any tax owed and reporting requirements, not the recipient.

| What Counts as a Gift | What’s NOT a Gift |

|---|---|

| Cash to family members | Business transactions at fair value |

| Property deeded to children | Paying someone for services |

| Stocks or bonds given to friends | Transfers between U.S. citizen spouses |

| Interest-free loans (difference is a gift) | Tuition paid directly to schools |

| Adding someone to your account | Medical bills paid directly to providers |

ImportantThis applies to U.S. citizens and green card holders regardless of where they live. If you’re an American living abroad and give a substantial gift to anyone (whether in the U.S. or abroad), you follow the same gift tax rules as Americans living domestically.

The $19,000 Annual Exclusion: Your Free Pass

For 2025 and 2026, you can give up to $19,000 per person per year without needing to file Form 709.

Key Rules:

| Rule | What It Means | Example |

|---|---|---|

| Per recipient | Give $19,000 to unlimited people | Give $19,000 to each of your 3 children = $57,000 total, no reporting |

| Per year | Resets January 1 | Give $19,000 on Dec 31, 2025 + $19,000 on Jan 1, 2026 = OK |

| Per person | You and spouse each get $19,000 | Married couple can give $38,000 to one person |

Pro TipStrategic use of annual exclusions can transfer substantial wealth without ever filing Form 709. A married couple with 3 children could give away $114,000 per year ($38,000 × 3) with zero reporting

Gift Splitting for Married Couples

Example: Gift Splitting in Action

Michael and Sarah want to give their daughter $35,000 for a down payment.

| Scenario | Michael Gives Alone | Michael + Sarah Split |

|---|---|---|

| Gift amount | $35,000 | $35,000 |

| Annual exclusion | $19,000 | $19,000 each |

| Amount over exclusion | $16,000 | $0 |

| Form 709 required? | Yes | No* |

| Tax owed? | No (lifetime exemption) | No |

*Gift splitting requires filing Form 709 to make the election, even when under limits

Special Rules for Non-U.S. Citizen Spouses

Gifts between U.S. citizen spouses are normally unlimited. However, if your spouse is not a U.S. citizen, different limits apply:

| Tax Year | Annual Limit to Non-U.S. Citizen Spouse |

|---|---|

| 2025 | $190,000 |

| 2026 | $194,000 |

Take Note: Gifts above these amounts require filing Form 709.

The Lifetime Gift Tax Exemption

Quick Facts:

| Category | 2025 Limit | 2026 Limit |

|---|---|---|

| Individual lifetime exemption | $13.99 million | $15 million |

| Married couple (combined) | $27.98 million | $30 million |

| When tax actually owed | After exceeding lifetime limit | After exceeding lifetime limit |

| Tax rate if you exceed | 18% to 40% | 18% to 40% |

ImportantThis lifetime exemption is unified with the estate tax exemption. When you make gifts exceeding the annual exclusion, you simply reduce your available lifetime exemption. You only owe actual gift tax after exhausting this entire lifetime amount.

Example: How the Lifetime Exemption Works

Patricia gives her son $250,000 in 2025 to start a business.

| Step | Amount | Explanation |

|---|---|---|

| Total gift | $250,000 | Full amount given |

| Annual exclusion | -$19,000 | No reporting needed for this portion |

| Amount over exclusion | $231,000 | Must report on Form 709 |

| Tax owed? | $0 | Still far below $13.99M lifetime limit |

| New lifetime exemption | $13.759M | Reduced from $13.99M |

When Do I Actually Owe Gift Tax?

Very few people ever pay gift tax. You only owe gift tax if your cumulative gifts over your lifetime exceed:

- $13.99 million in 2025

- $15 million in 2026 (made permanent under One Big Beautiful Bill Act)

ImportantIf you exceed these amounts, gift tax rates range from 18% to 40% depending on the amount. But reaching this threshold means you’ve already given away millions tax-free.

Gifts That Never Require Form 709

| Gift Type | Limit | Key Rule |

|---|---|---|

| To U.S. citizen spouse | Unlimited | No reporting ever |

| To qualified charities | Unlimited | Can deduct on tax return |

| Political contributions | Unlimited | To political organizations |

| Tuition payments | Unlimited | Must pay school directly |

| Medical expenses | Unlimited | Must pay provider directly |

| Under annual exclusion | $19,000 per person | Per recipient, per year |

ImportantFor tuition and medical payments, you must pay the institution or provider directly. If you give money to the person and they pay, it’s a taxable gift subject to annual exclusion limits.

Real-World Example: Education Payments

James wants to help his niece with college expenses.

| Option | Payment Method | Amount | Form 709 Required? |

|---|---|---|---|

| Option 1 | Pays $50,000 directly to university | $50,000 | No |

| Option 2 | Gives niece $50,000, she pays university | $50,000 | Yes (for $31,000 over limit) |

Same money, different tax treatment based on how it’s paid.

How to File Form 709: U.S. Gift Tax Return

Form 709 is the U.S. Gift (and Generation-Skipping Transfer) Tax Return.

Filing at a Glance:

| Detail | Information |

|---|---|

| When to file | April 15 (or June 15 for expats) |

| Extension available | Yes, until October 15 |

| E-file option | No – must mail paper form |

| Filed with 1040? | No – filed separately |

| Tax typically owed | Usually $0 (lifetime exemption applies) |

What You’ll Need:

- Description of each gift

- Date gift was made

- Fair market value (appraisal for property)

- Recipient’s name and relationship

- Your cumulative lifetime gifts

Mailing Address:

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999Pro TipEven when no tax is owed, Form 709 creates an official IRS record of the gift’s value. This can prevent future disputes about valuations, especially for property or business interests.

Common Gift Tax Scenarios for Expats (Giving Gifts)

Scenario 1: Helping Children Buy Property

Situation: Emily lives in France and wants to give each of her two children $100,000 to help with home purchases in the U.S.

| Detail | Amount | Explanation |

|---|---|---|

| Total gifts | $200,000 | $100,000 × 2 children |

| Annual exclusion | -$38,000 | $19,000 × 2 children |

| Must report on Form 709 | $162,000 | Amount over exclusion |

| Tax owed | $0 | Lifetime exemption applies |

| Remaining lifetime exemption | $13.828M | $13.99M – $162,000 |

Scenario 2: Gift to Foreign Parent

Situation: David lives in Japan and sends his mother in the Philippines $25,000 for medical expenses.

| Payment Method | Form 709 Required? | Why |

|---|---|---|

| Paid directly to medical providers | No | Unlimited medical exclusion |

| Sent to his mother | Yes | $6,000 over $19,000 exclusion |

Scenario 3: Family Member Starting a Business

Situation: Rebecca in Germany gives her nephew $150,000 to start a business in Canada.

| Step | Amount | Action |

|---|---|---|

| Gift amount | $150,000 | Full amount |

| Annual exclusion | -$19,000 | Automatic |

| Amount to report | $131,000 | Must file Form 709 |

| Tax owed | $0 | Lifetime exemption |

| Key point | n/a | Nephew’s location (Canada) doesn’t change Rebecca’s filing requirements |

Part 2: When You RECEIVE Gifts (Form 3520)

Quick Answer: Do I Need to File Form 3520?

File Form 3520 if you received:

- ✓ More than $100,000 from a foreign individual or estate (refers to aggregate gifts during the tax year from foreign individuals or estates)

- ✓ More than $20,116 from a foreign corporation or partnership

- ✓ Multiple gifts from related foreign persons totaling over $100,000

Don’t file Form 3520 if:

- ✗ The gift came from a U.S. citizen or green card holder

- ✗ Total gifts from foreign individuals were under $100,000

- ✗ You’re giving a gift (that’s Form 709, not Form 3520)

What Is a Foreign Gift?

For U.S. tax purposes, a foreign gift is money or property you receive from a foreign person that you treat as a gift.

“Foreign Person” Includes:

| ✓ Foreign Person | ✗ NOT Foreign Person |

|---|---|

| Nonresident alien individuals | U.S. citizens (even if living abroad) |

| Foreign corporations | Green card holders |

| Foreign partnerships | U.S. domestic trusts |

| Foreign estates | U.S. corporations |

| Foreign trusts | U.S. partnerships |

Critical: The donor’s tax status determines whether a gift is “foreign,” not where the money came from.

Real-World Examples:

| Situation | Is It a Foreign Gift? | Why? |

|---|---|---|

| Maria in Spain receives $150,000 from her U.S. citizen brother’s London bank | No | Brother is U.S. citizen |

| Tom in California receives $150,000 from his Canadian mother in Canada | Yes | Mother is nonresident alien |

| Sarah receives $120,000 from her green card holder father in Germany | No | Father is U.S. person |

When Must I Report Receiving a Foreign Gift?

You must file Form 3520 based on these thresholds:

| Source of Gift | 2025 Threshold | 2026 Threshold | Aggregate Rule |

|---|---|---|---|

| Foreign individual | $100,000+ | $100,000+ | Combine all gifts from same person |

| Foreign estate (inheritance) | $100,000+ | $100,000+ | Total from that estate |

| Foreign corporation | $20,116+ | TBD* | Adjusted annually |

| Foreign partnership | $20,116+ | TBD* | Adjusted annually |

*Inflation-adjusted each year

Take NoteThese thresholds apply to the total amount you receive during the tax year, not individual transfers.

For foreign individuals or estates, the $100,000 threshold applies to the aggregate amount from that foreign person, and includes amounts from related persons the IRS treats as a single source.

For foreign corporations or partnerships, the $20,116 threshold for 2025 applies to the aggregate amount received from all foreign entities during the year. The IRS does not use a “same source” rule for entities — you combine amounts from all foreign corporations and partnerships when determining whether you must file Form 3520.

The “Same Source” and “Related Parties” Rules

The IRS aggregates gifts from related foreign persons to prevent people from avoiding reporting by splitting large gifts.

How Aggregation Works:

| Example | Individual Amounts | Must Aggregate? | Total | File Form 3520? |

|---|---|---|---|---|

| Uncle + his wife + their child | $45K + $40K + $25K | Yes (related) | $110K | Yes |

| Uncle + unrelated friend | $50K + $50K | No (unrelated) | $100K each | No |

| Mother + Father | $60K + $50K | Yes (spouses) | $110K | Yes |

Real-World Example: Related Party Aggregation

Kevin receives gifts from his Italian relatives:

| Gift From | Relationship | Amount | Aggregate? |

|---|---|---|---|

| Uncle Mario | Uncle | $45,000 | Yes |

| Aunt Lucia | Mario’s wife | $40,000 | Yes |

| Cousin Francesca | Mario & Lucia’s daughter | $25,000 | Yes |

| Total from related source | $110,000 | Must file Form 3520 |

If Kevin received $50,000 from Uncle Mario and $50,000 from an unrelated foreign friend, he would NOT need to file Form 3520 because neither source individually exceeded $100,000.

Are Foreign Gifts Taxable?

Short answer: No. The U.S. does not tax recipients of gifts.

| What | Taxable? | Why |

|---|---|---|

| The gift itself | No | Never taxed to recipient |

| Interest earned on gifted cash | Yes | Investment income |

| Dividends from gifted stocks | Yes | Investment income |

| Rental income from gifted property | Yes | Rental income |

| Capital gains when you sell gifted property | Yes | Gain on sale |

Take NoteIf the gift generates income after you receive it, that income IS taxable. Report it on your Form 1040.

Foreign Inheritances: Same Rules as Gifts

The IRS treats inheritances from foreign estates the same as gifts for reporting purposes.

| You Inherit | Amount | Form 3520 Required? |

|---|---|---|

| Cash from grandmother in Scotland | £125,000 (~$160,000) | Yes |

| Property from uncle in France | €90,000 (~$95,000) | No (under $100K) |

| Business shares from aunt in Mexico | $250,000 value | Yes |

How to File Form 3520 for Foreign Gifts

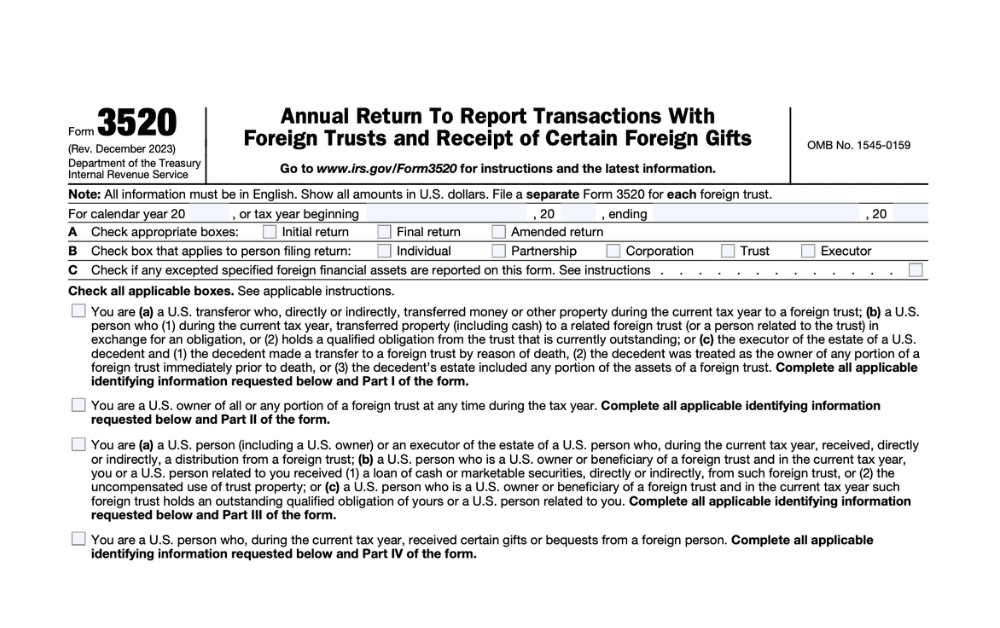

Form 3520 (Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts) – Part IV covers foreign gifts.

Filing at a Glance:

| Detail | Information |

|---|---|

| When to file | April 15 (or June 15 for expats abroad) |

| Extension | October 15 (same as Form 1040 extension) |

| E-file option | No – must mail paper form |

| Filed with 1040? | No – filed separately |

| Tax owed | Never – informational only |

| Complete which section | Part IV only (skip trust sections) |

Information You’ll Need:

- ☐ Donor’s name and address

- ☐ Date gift was received

- ☐ Description of property

- ☐ Fair market value in U.S. dollars

- ☐ Relationship to donor

- ☐ Exchange rate used (if applicable)

Mailing Address:

Internal Revenue Service Center

P.O. Box 409101

Ogden, UT 84409

Important: For inheritances, use the date you became the legal owner. If the death date and transfer date occur in different tax years, report at the death date to avoid late-filing penalties.

Common Foreign Gift Scenarios (Receiving Gifts)

Scenario 1: Wedding Gift from Foreign Family

Situation: Lisa (U.S. citizen in Texas) marries Pierre (French citizen). Pierre’s parents (French citizens in France) give them €110,000 (~$120,000) as a wedding gift.

| Analysis | Conclusion |

|---|---|

| Are Pierre’s parents foreign persons? | Yes (French citizens, not U.S. persons) |

| Amount exceeds $100,000 threshold? | Yes ($120,000) |

| Must file Form 3520? | Yes – Lisa must file |

| Is gift taxable to Lisa? | No – never taxed |

Scenario 2: Multiple Gifts from Same Foreign Source

Situation: Mark’s Australian parents (both foreign citizens) give him:

| Month | Purpose | Amount |

|---|---|---|

| January | Car | $30,000 |

| June | Business investment | $45,000 |

| November | Home repairs | $35,000 |

| Total | $110,000 |

Conclusion: Even though each gift was under $100,000, Mark must aggregate them (same source) and file Form 3520.

Scenario 3: Property Inherited from Abroad

Situation: Jennifer inherits an apartment in Italy worth €200,000 (~$220,000) from her aunt (Italian citizen).

| Detail | Answer |

|---|---|

| Is this a foreign bequest? | Yes |

| Amount exceeds $100,000? | Yes ($220,000) |

| Must file Form 3520? | Yes |

| Taxable to Jennifer? | No (gift/inheritance itself) |

| If Jennifer sells later? | Yes (capital gains tax on gain) |

Scenario 4: Below Threshold (No Filing Required)

Situation: Robert receives $75,000 from his uncle in Germany.

| Analysis | Result |

|---|---|

| Amount below $100,000 threshold? | Yes ($75,000) |

| Form 3520 required? | No |

| Taxable? | No |

| Should keep documentation? | Yes (good practice) |

Penalties for Failing to Report Gifts

The IRS takes gift reporting seriously. Penalties differ based on which form you failed to file.

Penalty Comparison at a Glance

| Form | Base Penalty | Maximum | When It Applies |

|---|---|---|---|

| Form 709 (giving) | 5% of tax due per month | 25% of tax | When tax is actually owed (rare) |

| Form 3520 (receiving) | 5% of gift value per month | 25% of gift value | Always – even when no tax owed |

Critical Difference: Form 3520 penalties apply to the gift amount itself, making them much more severe than Form 709 penalties.

Form 709 Penalties (For Givers)

Penalty Types:

| Penalty Type | Rate | Maximum | Applies When |

|---|---|---|---|

| Late filing | 5% per month | 25% | Of the tax due |

| Late payment | 0.5% per month | 25% | Of unpaid tax |

| Interest charges | Variable rate | None | From due date |

Pro TipIf no tax is actually owed (because you’re under lifetime exemption), penalties may be minimal or waived if you can show reasonable cause for late filing.

Key Point: However, failing to file creates problems for future estate tax purposes because the IRS won’t have official records of gifts that used up portions of your lifetime exemption.

Form 3520 Penalties (For Recipients)

Form 3520 penalties are severe and apply even though no tax is owed.

How Penalties Calculate:

| Months Late | Penalty Rate | Total Penalty |

|---|---|---|

| 1 month | 5% | 5% of gift |

| 2 months | 5% × 2 | 10% of gift |

| 3 months | 5% × 3 | 15% of gift |

| 4 months | 5% × 4 | 20% of gift |

| 5+ months | 5% × 5 | 25% of gift (maximum) |

Real Penalty Calculation Example:

Sarah received a $150,000 gift from her Japanese grandmother in January 2025 but forgot to file Form 3520 by April 15, 2026. The IRS discovers the oversight in August 2026 (4 months late).

| Calculation | Amount |

|---|---|

| Gift value | $150,000 |

| Penalty rate | 5% per month |

| Months late | 4 months |

| Total penalty | $30,000 |

Critical: This is a $30,000 penalty for simply failing to report a gift that wasn’t even taxable. The 5% monthly penalty quickly accumulates to the 25% maximum.

Additional Consequences:

- ⚠️ IRS may determine tax treatment of the gift (potentially treating it as taxable income)

- ⚠️ Increased audit risk

- ⚠️ Difficulties resolving the matter later

Reasonable Cause Exception

Both Form 709 and Form 3520 penalties may be waived if you can demonstrate “reasonable cause.”

What Qualifies as Reasonable Cause:

| ✓ May Qualify | ✗ Unlikely to Qualify |

|---|---|

| Serious illness preventing filing | Forgot about the requirement |

| Natural disaster | Was too busy |

| Death in immediate family | Didn’t know (without good faith effort) |

| Filed as soon as you learned of requirement | Accountant didn’t tell me |

| Good faith effort to comply | Misunderstood the rules |

Steps to Request Relief:

- File the delinquent form immediately

- Include a written statement explaining reasonable cause

- Provide supporting documentation

- Show you acted in good faith

- Demonstrate you filed as soon as you became aware

Pro TipIf you discover you should have filed Form 3520 in a previous year, file it immediately with a statement explaining the reasonable cause for the delay. This may help avoid or reduce penalties.

Special Rules and Exceptions

Gifts from U.S. Persons Living Abroad

A gift from a U.S. citizen or green card holder is NOT a foreign gift, regardless of circumstances.

| Scenario | Foreign Gift? | Why |

|---|---|---|

| U.S. citizen in Singapore wires $200K from Singapore bank | No | Donor is U.S. person |

| Green card holder in France gives €150K | No | Donor is U.S. person |

| U.S. citizen gifts property located in Italy | No | Donor status matters, not property location |

Example: Rachel (New York) receives $200,000 from her brother (U.S. citizen living in Singapore), wired from his Singapore bank account.

| Question | Answer |

|---|---|

| Is this a foreign gift? | No – brother is U.S. citizen |

| Does Rachel file Form 3520? | No |

| Does her brother file Form 709? | Yes – if over $19,000 (he gave $200,000) |

Key Takeaway: The donor’s citizenship/residency status determines whether it’s a foreign gift, not the location of the money or property.

Covered Expatriates: The Tax Exception

Critical exception: Gifts from covered expatriates ARE taxable to the recipient.

What Is a Covered Expatriate?

A former U.S. citizen or green card holder who:

- Renounced their status, AND

- Meets criteria (typically net worth over $2 million OR average annual income tax over ~$200,000 in five years before expatriation)

How It Works:

| Detail | Amount/Rule |

|---|---|

| Annual exclusion | $19,000 (for 2025/2026) |

| Amount over exclusion | Subject to 40% tax |

| Who pays tax | The recipient (not the donor) |

| Form to use | Form 708 (not Form 3520) |

| Applies to gifts received | On or after June 17, 2008 |

Example: Covered Expatriate Gift

Your uncle renounced U.S. citizenship in 2020 and qualified as a covered expatriate. In 2025, he gives you $100,000.

| Calculation | Amount | Explanation |

|---|---|---|

| Total gift | $100,000 | Full amount |

| Annual exclusion | -$19,000 | Not taxable |

| Taxable amount | $81,000 | Subject to 40% tax |

| Tax you owe | $32,400 | You pay, not your uncle |

ImportantThis unusual rule exists to prevent wealthy individuals from avoiding U.S. estate and gift taxes by renouncing citizenship and then gifting money to U.S. relatives.

Gifts vs. Income: Important Distinctions

The IRS scrutinizes large transfers from foreign persons to ensure they’re truly gifts and not disguised compensation.

Red Flags vs. Clear Gifts:

| Red Flags (Probably Income) | Clear Gifts |

|---|---|

| Regular payments over time | One-time or occasional transfers |

| Tied to services you provide | No services expected |

| From employer/client | From family members |

| Payments from foreign business you work for | Inheritance or family support |

| Tied to performance or deliverables | No strings attached |

Example Comparison:

| Situation | Is It a Gift? | Tax Treatment |

|---|---|---|

| Maria receives $50,000 from her aunt in Brazil for her wedding | Yes | Not taxable (but report on Form 3520 if over threshold) |

| Maria receives $5,000/month from her aunt’s Brazilian company while consulting | No | Taxable compensation on Form 1040 |

If Misclassified, You Could Owe:

- ✗ Income tax on the entire amount

- ✗ Self-employment tax (if applicable)

- ✗ Penalties for underreporting income

Student Support Payments

Many expat families question how to handle parents supporting students from abroad.

| Payment Type | Form 3520 Required? | Counts Toward Threshold? |

|---|---|---|

| Tuition paid directly to school | No | No – unlimited exclusion |

| Medical paid directly to provider | No | No – unlimited exclusion |

| Money sent to student for living expenses | If over $100K | Yes |

| Money sent to student for any purpose | If over $100K | Yes |

Example: Student Support

Hans (German citizen) whose daughter attends U.S. university each year:

| Hans Pays | Form 3520 Required? | Why |

|---|---|---|

| $60,000 directly to university for tuition | No | Direct payment exclusion |

| $50,000 to daughter for rent/food/books | If total from Hans exceeds $100K | Counts toward threshold |

If Hans’ daughter receives more than $100,000 total from him in a year (not counting direct tuition payments), she must file Form 3520.

Filing Multiple Gift Tax Forms

Some situations require filing both Form 709 and Form 3520.

Example: Multi-Generational Gifts

Linda (U.S. citizen, California) receives $200,000 from her mother in Canada (Canadian citizen). Linda then gives $150,000 to her daughter for a home down payment.

Linda’s Requirements:

| Transaction | Form | Amount to Report | Why |

|---|---|---|---|

| Receiving from Canadian mother | Form 3520 | $200,000 | Foreign gift over $100K |

| Giving to daughter | Form 709 | $131,000 | Over $19,000 annual exclusion |

Both forms due April 15 (or June 15 for expats).

Take Note: These are two separate transactions with different reporting requirements, even though the money flows through the same person.

Gift Tax Planning Strategies for Expats

Strategy 1: Annual Exclusion Gifts (Use It or Lose It)

The $19,000 annual exclusion resets each January 1. Strategic use can transfer substantial wealth without filing Form 709.

Multi-Year Gifting Example:

Gregory wants to give his three children $300,000 total. Rather than triggering Form 709:

| Year | Amount Per Child | Total Given | Form 709 Required? |

|---|---|---|---|

| Year 1 | $19,000 × 3 | $57,000 | No |

| Year 2 | $19,000 × 3 | $57,000 | No |

| Year 3 | $19,000 × 3 | $57,000 | No |

| Years 4-5 | Remaining amounts | Balance | Depends on amounts |

| Total Over 5 Years | $300,000 | Minimal reporting |

This minimizes Form 709 filing and preserves more of his lifetime exemption for larger future gifts or estate planning.

Strategy 2: Gift Splitting for Maximum Benefit

Married couples can effectively double the annual exclusion through gift splitting.

Comparison:

| Scenario | Gift Amount | Form 709 Required? | Amount to Report |

|---|---|---|---|

| Monica (single) gives nephew $35,000 | $35,000 | Yes | $16,000 over limit |

| Monica (married) + spouse split gift | $35,000 | Yes* | $0 over limit |

*Filing required to elect gift splitting, even when under limits

Even when no tax is owed, gift splitting requires filing Form 709 to make the election.

Strategy 3: Direct Payment Strategy

For education and medical expenses, always pay providers directly when possible.

Impact Comparison:

| Strategy | Direct to Institution | Given to Student |

|---|---|---|

| Amount | $100,000 tuition | $100,000 to student |

| Annual exclusion used | $0 | $19,000 |

| Amount over exclusion | $0 | $81,000 |

| Form 709 required | No | Yes |

| Limit | Unlimited | Subject to lifetime exemption |

Optimal Approach:

Pay directly to institution:

- ✓ No dollar limit

- ✓ Doesn’t count against annual exclusion

- ✓ Doesn’t count against lifetime exemption

- ✓ No Form 709 required

Give money to individual:

- ✗ Counts toward $19,000 annual exclusion

- ✗ Excess reduces lifetime exemption

- ✗ Form 709 required if over $19,000

Strategy 4: Cross-Border Considerations

Moving Between Countries:

| Consideration | Key Point |

|---|---|

| U.S. citizenship | Gift tax rules follow you worldwide |

| Residence doesn’t matter | Living abroad doesn’t change obligations |

| Foreign gift reporting | Applies regardless of where you live |

| Other countries | May have their own gift tax systems |

Dual Citizenship Situations:

If you have dual U.S./foreign citizenship:

- ✓ U.S. gift tax rules still apply to you

- ✓ You may have obligations in your other country

- ✓ Consult tax professionals in both countries

- ✓ Plan timing of large gifts carefully

Common Gift Tax Mistakes to Avoid

| Mistake | ❌ Wrong Assumption | ✓ Right Understanding |

|---|---|---|

| 1. Foreign gift definition | “My dad sent money from London, so it’s a foreign gift” | If dad is a U.S. citizen or green card holder, it’s NOT a foreign gift (donor status matters, not location) |

| 2. Tax on receiving | “I received $150,000 from France, so I’ll owe gift tax” | Recipients never owe U.S. gift tax (only Form 3520 reporting, no tax) |

| 3. Failing to aggregate | “I got $60K from uncle and $50K from aunt in Japan. Neither exceeds $100K, so no filing” | Must aggregate if related ($110K total exceeds threshold → file Form 3520) |

| 4. No Form 709 if no tax | “I gave $50K but won’t owe tax due to lifetime exemption, so I don’t need to file” | Must file Form 709 to track lifetime exemption usage, even if $0 tax owed |

| 5. Gift splitting without filing | “We each gave $15K ($30K total), we’re under $19K each, no filing” | Gift splitting requires filing Form 709 to make the election |

| 6. Confusing FBAR with Form 3520 | “I reported my foreign account on FBAR, so I don’t need Form 3520” | Different purposes: FBAR reports accounts; Form 3520 reports gifts received |

How Greenback Can Help

Gift tax reporting for Americans abroad involves multiple forms, complex rules, and severe penalties for mistakes.

What We Do:

| Service | Details |

|---|---|

| Form 709 Preparation | For gifts you’ve made over $19,000 |

| Form 3520 Preparation | For foreign gifts you’ve received over $100,000 |

| Delinquent Filing | Past years with reasonable cause explanations |

| Gift Tax Planning | Strategies for your unique situation |

| Current + Prior Years | Both current and back-year reporting |

Why Choose Greenback:

- ✓ Helped over 23,000+ expats file correctly

- ✓ 4.9 star average across 1,200+ TrustPilot reviews

- ✓ 15+ years of expat tax expertise

- ✓ Avoid costly 25% penalties

- ✓ Peace of mind knowing forms are filed right

Our Expertise:

We understand:

- When Form 709 vs. Form 3520 applies

- How to calculate aggregate gifts from related foreign persons

- Strategies to maximize annual exclusions

- How to properly document gifts for IRS compliance

- Reasonable cause arguments for missed filings

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on US expat taxes or working with Greenback, contact our Customer Champions.

Work with an expert who understands expat gift rules.

The information provided in this article is for general guidance only and should not be considered legal or tax advice. Tax laws change frequently, and individual circumstances vary. Always consult with a qualified tax professional before making decisions about your tax situation.

Related Resources

Essential Reading for Gift Tax Situations

- Form 3520 for Americans Living Abroad: Complete Guide

- Form 709: U.S. Gift Tax Guide for Expats

- Do I Have to Pay Taxes on Foreign Inheritance to the IRS?

- Form 1040 for U.S. Expats: Complete Filing Guide

- Streamlined Filing Procedures: Catching Up on Late Returns

- FBAR Filing Requirements for Expats

- Form 8938 (FATCA) Reporting

- U.S. Tax Forms for Expats: What You Need to File

- Tax Services and Pricing

- Foreign Pension Taxation in the U.S.