What Is Form 1098? Mortgage Interest, Tuition, and More

- Different Types of Form 1098

- What is Form 1098 (Mortgage Interest Statement)?

- Who Receives Form 1098?

- What's Included on Form 1098

- Mortgage Interest Deduction Explained

- Expat-Specific Scenarios

- How to Use Form 1098 on Your Tax Return

- Common Expat Scenarios

- What If You Don't Receive Form 1098?

- Maximizing Your Deduction

- Common Mistakes to Avoid

- Next Steps

The IRS requires lenders to send Form 1098 when you pay $600 or more in mortgage interest during the year—but “Form 1098” actually refers to a family of tax forms. While Form 1098 (mortgage interest) is the most common, you might also encounter Form 1098-T (tuition), 1098-E (student loan interest), or 1098-C (charitable vehicle donations). For American expats, the mortgage interest version is typically the most valuable, potentially saving thousands on your U.S. taxes.

The bottom line: Form 1098 helps you claim tax deductions, with the mortgage-interest version most relevant for expats. If you received any 1098 form, you likely qualify for valuable deductions—including on foreign properties that serve as your main or second home.

Received a Form 1098? Make Sure You’re Claiming It Correctly.

Different Types of Form 1098

Form 1098 – Mortgage Interest Statement (Most Common)

Reports mortgage interest of $600 or more that you paid during the year. This applies to your primary residence, second homes, and even qualified foreign properties.

Form 1098-T – Tuition Statement

Educational institutions send this form reporting tuition and fees paid, which may qualify you for education credits like the American Opportunity Credit.

Form 1098-E – Student Loan Interest Statement

Student loan servicers send this when you paid $600 or more in student loan interest, which may be deductible up to $2,500 per year.

Form 1098-C – Contributions of Motor Vehicles

Charitable organizations send this when you donate a vehicle worth more than $500.

For the rest of this article, we’ll focus on Form 1098 (mortgage interest), since it’s the most common and valuable for American expats.

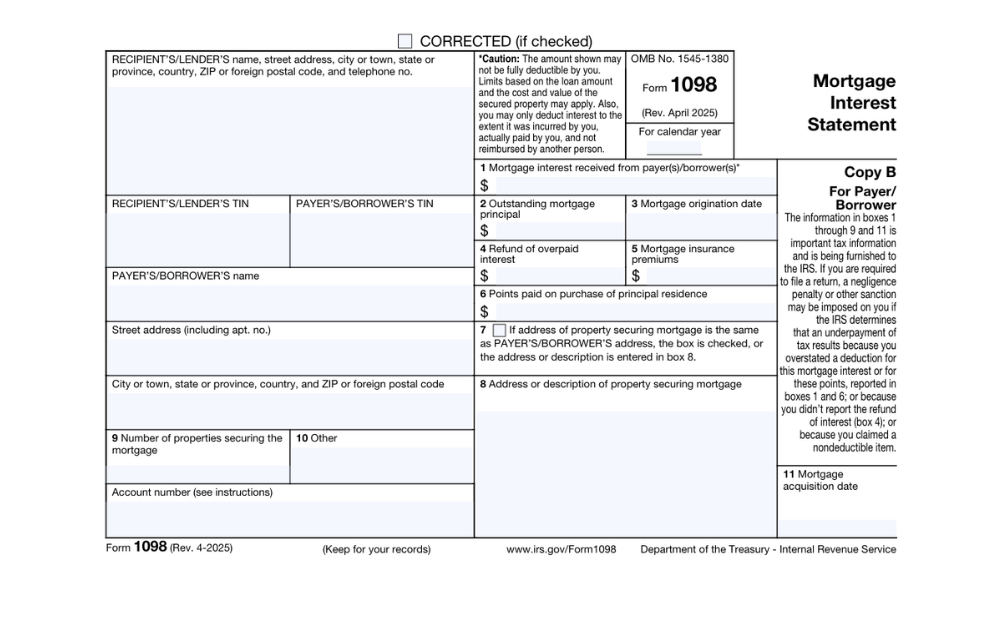

What is Form 1098 (Mortgage Interest Statement)?

Form 1098, officially titled “Mortgage Interest Statement,” is an information return that lenders must file when they receive $600 or more in mortgage interest from you during the tax year. The form reports the total mortgage interest you paid, which you can then use to claim the mortgage interest deduction on your tax return.

Your lender sends you Copy B of Form 1098 by January 31st, while Copy A goes directly to the IRS. If you have multiple mortgages, you’ll receive a separate Form 1098 for each one.

Why This Matters for American Expats

As an American living abroad, you’re required to file U.S. tax returns regardless of where your income comes from or where you live. The mortgage interest deduction is one of the most valuable tax benefits available, and it doesn’t matter whether your property is in Manhattan or Madrid—qualified mortgage interest is deductible.

Many expats mistakenly think they can’t claim this deduction on foreign properties. That’s simply not true. The tax code treats foreign and domestic mortgages equally, as long as the property qualifies as your main home or second home.

Who Receives Form 1098?

You’ll receive Form 1098 if you meet these criteria:

- You paid $600 or more in mortgage interest during the tax year

- The mortgage is secured by real property (your home serves as collateral)

- You’re the primary borrower, legally obligated to pay the debt

- The lender is in the business of lending money

What’s Included on Form 1098

The form contains several important boxes:

- Box 1: Mortgage Interest Received – The total deductible mortgage interest you paid during the year

- Box 2: Outstanding Mortgage Principal – Your loan balance as of January 1st

- Box 3: Mortgage Origination Date – When your loan began

- Box 4: Refund of Overpaid Interest – Any interest refunds you received

- Box 5: Mortgage Insurance Premiums – Premium payments that may be deductible

- Box 6: Points Paid on Purchase – Deductible points paid when buying your home

Mortgage Interest Deduction Explained

The mortgage interest deduction allows you to reduce your taxable income by the amount of qualified mortgage interest you paid during the year. This deduction is particularly valuable for expats who may already be using the Foreign Earned Income Exclusion or Foreign Tax Credit to reduce their U.S. tax liability.

Current Deduction Limits (2025 Tax Year)

For mortgages obtained after December 15, 2017:

- Maximum deductible debt: $750,000 ($375,000 if married filing separately)

For mortgages obtained on or before December 15, 2017:

- Maximum deductible debt: $1,000,000 ($500,000 if married filing separately)

These limits are scheduled to revert to $1,000,000 for all mortgages after December 31, 2025, unless Congress extends the current rules.

Qualifying Property Types

Your mortgage interest is deductible if the loan is secured by:

- Your main home (primary residence)

- A second home or vacation property

- A qualified home under construction

- Land on which you’re building a qualified home

The property can be a house, condominium, cooperative, manufactured home, boat, RV, or any structure with sleeping, cooking, and toilet facilities.

Expat-Specific Scenarios

Foreign Property Mortgages

Good news: You can deduct mortgage interest on foreign properties that qualify as your main or second home. The IRS doesn’t distinguish between domestic and foreign real estate for this deduction.

Example: Sarah, a U.S. expat living in London, owns a flat in the UK that serves as her primary residence. She has a £400,000 mortgage and paid £12,000 in interest during 2025. Since this property is her primary residence, the mortgage interest is fully deductible on her U.S. tax return (after conversion to USD).

Currency Conversion Requirements

When reporting foreign mortgage interest:

- Convert all amounts to U.S. dollars using the average exchange rate for the tax year

- Use consistent exchange rates throughout your return

- Keep records of the exchange rates used

- Your foreign lender likely won’t provide Form 1098, so request a similar statement showing interest paid

Rental Properties Abroad

If you own foreign rental property, mortgage interest is deductible as a rental expense on Schedule E, not as an itemized deduction on Schedule A. This can be more advantageous since rental expenses aren’t subject to the standard deduction threshold.

How to Use Form 1098 on Your Tax Return

Step 1: Determine if You Should Itemize

The mortgage interest deduction is only available if you itemize deductions using Schedule A. For 2025, the standard deduction is:

- Single: $15,000

- Married Filing Jointly: $30,000

- Head of Household: $22,500

You should itemize only if your total itemized deductions exceed your standard deduction amount.

Step 2: Complete Schedule A

Report your mortgage interest on Schedule A:

- Line 8a: Enter the amount from Box 1 of Form 1098

- Line 8b: Add any deductible mortgage interest not reported on Form 1098

- Line 8c: Enter deductible points not reported on Form 1098

Step 3: Consider Other Itemized Deductions

Maximize your benefit by claiming all available itemized deductions:

- State and local taxes (up to $10,000)

- Charitable contributions

- Medical expenses exceeding 7.5% of AGI

Common Expat Scenarios

Corporate Expat with Company Housing

Many corporate expats receive housing allowances or have company-provided housing. If your employer pays your mortgage interest directly, that payment is typically taxable income to you, but you can still claim the mortgage interest deduction.

Digital Nomad with Multiple Properties

If you own properties in multiple countries but use them as personal residences, you can potentially deduct mortgage interest on your main home and one second home. Properties used primarily for rental don’t qualify for the personal mortgage interest deduction.

Retiree with Foreign and U.S. Properties

Retirees often maintain homes in both the U.S. and their new country of residence. You can choose which property to treat as your main home and which as your second home for tax purposes, but you must be consistent.

What If You Don’t Receive Form 1098?

You might not receive Form 1098 if:

- You paid less than $600 in mortgage interest

- Your lender isn’t in the business of lending money

- You have a foreign lender who doesn’t file U.S. forms

Solution: You can still claim the deduction! Request a statement from your lender showing:

- Total interest paid during the tax year

- Outstanding loan balance

- Property address securing the loan

- Confirmation that you’re legally obligated to pay the debt

Maximizing Your Deduction

Home Equity Loans and Lines of Credit

For tax years 2018-2025, interest on home equity debt is deductible only if you use the proceeds to “buy, build, or substantially improve” the home that secures the loan. Personal use (like paying credit card debt) doesn’t qualify.

After 2025: The rules revert to allowing deductions regardless of how you use home equity loan proceeds, subject to the overall debt limits.

Refinancing Considerations

When you refinance:

- Interest on the new loan is deductible up to the amount of the old loan balance

- If you cash out additional equity, interest on that portion is only deductible if used for home improvements

- Points paid on refinancing must generally be deducted over the life of the loan

Common Mistakes to Avoid

1. Mixing Personal and Rental Property

Don’t claim mortgage interest on rental properties as an itemized deduction. Rental property mortgage interest goes on Schedule E as a rental expense.

2. Forgetting About Points

Points paid when purchasing or refinancing may be deductible either in full in the year paid or amortized over the loan term. Don’t miss this valuable deduction.

3. Incorrect Currency Conversion

Use consistent exchange rates and keep detailed records. The IRS expects reasonable, supportable conversion methods.

4. Exceeding Debt Limits

Monitor your total mortgage debt to ensure you don’t exceed the $750,000 limit ($1,000,000 for pre-2018 loans). Interest on debt above these limits isn’t deductible.

Next Steps

If you received any Form 1098 or paid mortgage interest during 2025:

- Identify which 1098 form you received and its specific purpose

- Gather all Forms 1098 and foreign lender statements

- Calculate your total itemized deductions to determine if itemizing benefits you

- Convert foreign currency amounts to U.S. dollars using consistent rates

- Complete the appropriate tax forms based on your deductions

The various 1098 forms can provide substantial tax savings for American expats, but the rules can be complex, especially when foreign properties or income sources are involved.

Have questions about Form 1098 or other expat tax matters? If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

File Your Taxes With Your Mortgage Deduction Done Right

This article provides general information and should not be considered personalized tax advice. Tax laws change frequently, and individual circumstances vary. Always consult with a qualified tax professional for advice specific to your situation.