What Is Form 1099-A and What Does It Mean for My Taxes?

You don’t need to file Form 1099-A yourself. If a property you owned was foreclosed on, repossessed, or abandoned, your lender files Form 1099-A with the IRS and sends you a copy. Your responsibility is to use the information on that copy when you file your tax return, because the event may create a taxable gain or loss.

According to the IRS instructions for Form 1099-A, the form reports the transfer of secured property. You may receive one if any of the following occurred:

- Foreclosure on a home or other real property

- Repossession of property used as loan collateral (such as business equipment)

- Voluntary surrender of collateral property to settle a debt

- Abandonment of property that secured a loan

Received Form 1099-A?

Here’s what Form 1099-A means for you and how it affects your tax return.

When Would I Receive Form 1099-A?

Your lender must send you Form 1099-A by January 31 of the year following the event. Any entity that lent money secured by property can issue this form, including banks, credit unions, mortgage companies, government agencies, and private lenders.

You may receive more than one Form 1099-A if you had multiple loans on a single property. Each lender must file separately.

Form 1099-A is not the same as Form 1099-C (Cancellation of Debt). If your lender both acquired the property and canceled the remaining debt in the same year, they may send you only a Form 1099-C instead. That form includes the property information that would have been on Form 1099-A, plus the canceled-debt amount, which the IRS may treat as taxable income. If you receive both forms, review them carefully because they report different tax consequences.

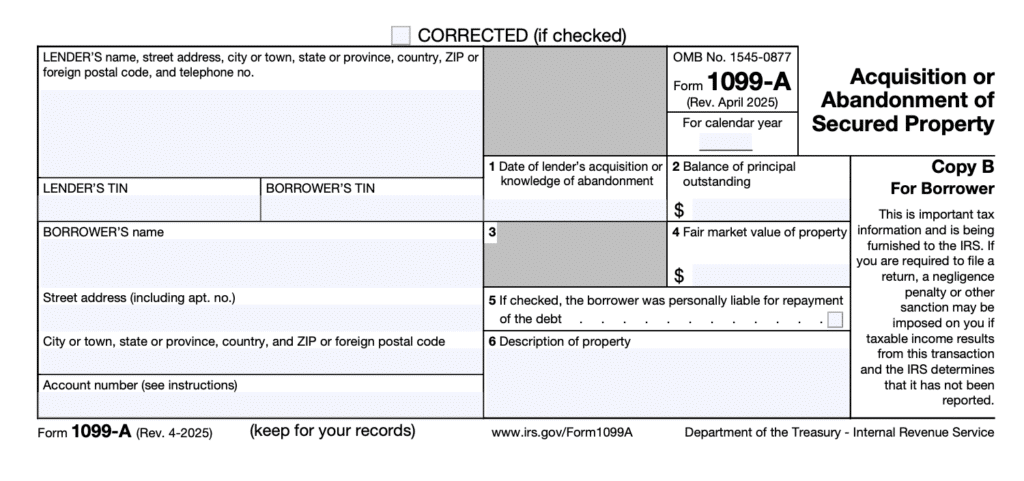

What Information Does Form 1099-A Include?

Form 1099-A provides the key data points you (or your tax preparer) will need:

| Box | What It Reports | Why It Matters |

|---|---|---|

| Box 1 | Date the lender acquired or learned of the abandonment | Determines the tax year you must report |

| Box 2 | Balance of principal outstanding | May affect gain/loss calculation depending on whether you were personally liable |

| Box 4 | Fair market value (FMV) of the property | Used to calculate whether you have a gain or a loss |

| Box 5 | Whether you were personally liable for the debt | Changes how the IRS calculates your gain or loss |

How Does Form 1099-A Affect My Tax Return?

Receiving Form 1099-A doesn’t automatically mean you owe taxes, but it does mean there may be a reportable gain or loss from the property transfer. The tax treatment depends on several factors, including:

- Whether you were personally liable for the debt

- The fair market value of the property versus your adjusted basis (what you originally paid plus improvements, minus depreciation)

- Whether any debt was canceled alongside the acquisition

For more detailed guidance on calculating gains, losses, and the implications of canceled debt, the IRS provides two helpful publications: Publication 544 (Sales and Other Dispositions of Assets) and Publication 4681 (Canceled Debts, Foreclosures, Repossessions, and Abandonments).

Because the calculations can become complex quickly, especially when debt cancellation, depreciation, and personal liability intersect, this is an area where working with a qualified tax professional can save you time and prevent costly errors.

What If I Own Property Abroad?

If you’re a U.S. taxpayer with property overseas, a foreclosure or abandonment abroad adds extra layers of complexity. You may need to convert foreign currency amounts, account for foreign tax implications, and determine how the property fits into your broader U.S. filing obligations.

Americans abroad may also need to consider how the gain or loss interacts with protections like the Foreign Earned Income Exclusion or Foreign Tax Credit, and whether any related foreign accounts trigger FBAR reporting requirements.

What Should I Do If I Didn’t Receive Form 1099-A?

If your property was foreclosed, repossessed, or abandoned and you haven’t received Form 1099-A, contact your lender directly to request a copy. Even if you never receive the form, you are still required to report the event on your tax return. The IRS expects you to report all taxable events regardless of whether you received the corresponding form.

Get Help Reporting Form 1099-A on Your Tax Return

Foreclosures and property abandonments involve some of the trickiest gain-and-loss calculations in the tax code. When you factor in potential debt cancellation, personal liability questions, and (for expats) foreign property complications, working with a qualified accountant isn’t just helpful, it’s essential for getting it right.

If you’re an American living abroad dealing with a foreclosure or property issue, our CPAs and Enrolled Agents can handle the full picture, from Form 1099-A reporting to foreign asset compliance. If you own property abroad, our specialists are well-versed in the unique reporting requirements that come with cross-border real estate.

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on U.S. expat taxes or working with Greenback, contact our Customer Champions.

Make Sure Your 1099-A Is Filed Correctly

The information provided is for general guidance only and should not be considered professional tax advice. Tax laws and regulations are subject to change, and individual circumstances may vary. Please consult with a qualified tax professional for specific advice regarding your tax situation.

Related Resources

- What Is a 1099 Form and How Does It Affect Your Expat Taxes?

- Form 1040: The Expat’s Guide

- Form 8949: How to Report Capital Gains and Losses

- U.S. Taxes on Foreign Property: Buying and Selling Real Estate Abroad

- How to Claim the Foreign Earned Income Exclusion

- FBAR Filing Requirements

- Foreign Tax Credit Guide

- What Happens If I File My U.S. Expat Taxes Late?