Form 8949 for U.S. Expats Explained: Reporting Capital Gains and Losses

- What is IRS Form 8949?

- When to File Form 8949

- What's New for the 2025 Tax Year (Filed in 2026)

- Short-Term vs. Long-Term Capital Gains on Form 8949

- How to Complete Form 8949: A Step-by-Step Guide

- Reporting Foreign Property Sales on Form 8949

- The Foreign Tax Credit and Form 8949

- Reporting Cryptocurrency on Form 8949

- What Is the Difference Between Form 8949 and FBAR?

- Common Form 8949 Mistakes to Avoid

- Frequently Asked Questions

- Get Expert Help With Form 8949

- Related Resources

What is IRS Form 8949?

IRS Form 8949 (Sales and Other Dispositions of Capital Assets) is the tax document used to report the individual sale or exchange of capital assets. It acts as a detailed transaction log, reconciling figures from broker statements, such as Forms 1099-B, 1099-S, and 1099-DA, with your final tax return.

When to File Form 8949

All U.S. citizens and green card holders must file this form if they sold, traded, or disposed of an asset during the tax year. This requirement applies globally and includes:

- Selling shares in a foreign company through a non-U.S. brokerage

- Trading or selling cryptocurrency (including crypto-to-crypto swaps)

- Selling foreign rental property or vacation homes

- Selling foreign mutual funds or ETFs (which may also trigger PFIC reporting)

- Trading stocks through a U.S. brokerage while living abroad

- Selling inherited property located outside the U.S.

The Reporting Sequence: From Transaction to Tax Return

Reporting capital gains follows a specific hierarchy, ensuring that every individual transaction is accounted for before it impacts your final tax liability. In the tax world, information “carries over” through the following sequence:

- Itemize on Form 8949: List every individual sale.

- Aggregate on Schedule D: Subtotals from 8949 are carried over here to calculate your net gain or loss.

- Report on Form 1040: Your final capital gain or loss flows through to your main tax return.

What’s Different for US Expats

For U.S. citizens and green card holders living abroad, Form 8949 reporting has layers of complexity that domestic-focused resources often miss:

- No 1099-B from Foreign Brokers: Non-U.S. institutions will not provide the standard tax forms. You are still responsible for itemizing every trade manually.

- Currency Conversion is Mandatory: Every transaction must be converted to U.S. dollars using the “spot rate” on the specific date of the trade. Fluctuations in exchange rates alone can trigger a taxable gain, even if the asset’s price didn’t change.

- Double Taxation Protection: If you paid local capital gains tax to your host country, you must coordinate Form 8949 with Form 1116 (Foreign Tax Credit) to ensure you aren’t taxed twice on the same profit.

- The FEIE Limitation: A common misconception is that the Foreign Earned Income Exclusion covers capital gains. The FEIE applies only to “earned” income (wages/self-employment); capital gains are always reported separately.

For the broader rules on how foreign capital gains are taxed, including currency conversion, the Foreign Tax Credit, and primary residence exclusions, see our complete guide to foreign capital gains tax for US expats.

What’s New for the 2025 Tax Year (Filed in 2026)

This year introduces significant shifts in how digital assets are categorized and reported to the IRS:

1. New Digital Asset Categories (Boxes G through L)

Form 8949 now includes specific checkboxes for digital asset transactions. Short-term digital asset transactions should be reported using Boxes G, H, or I. Long-term digital asset transactions should be reported using Boxes J, K, or L.

Digital asset transactions should no longer be reported using Boxes C or F, which are now reserved for other capital assets not reported on Form 1099-B.

2. The Debut of Form 1099-DA

Starting in 2025, major crypto exchanges and brokers are now required to send Form 1099-DA to both you and the IRS. This form shows the total amount of money received from selling or trading digital assets.

- Matching your records: You must make sure the total amounts on your 1099-DA match what you report on your Form 8949. If these numbers don’t line up, the IRS is more likely to flag your return for an inquiry.

- Tracking what you paid: For 2025, many brokers are only reporting your sales price, not what you originally paid for the crypto. You are still responsible for proving your original purchase price to calculate your actual profit or loss.

For a deep dive into these new requirements and how they impact your filing, see our complete guide to Form 1099-DA and digital asset reporting.

3. Wash Sales and Digital Assets

Despite legislative proposals, the wash sale rule has not been expanded to digital assets for the 2025 tax year.

Cryptocurrency continues to be treated as property, not as stock or securities, for purposes of Section 1091. This means you may still sell a digital asset at a loss and repurchase it within 30 days without the loss being disallowed, provided the transaction has economic substance.

4. Account-by-Account Basis Tracking

Beginning January 1, 2025, taxpayers can no longer rely on a universal method that aggregates digital asset basis across multiple wallets or accounts. Basis must now be tracked on a wallet-by-wallet or account-by-account basis, making detailed record keeping more important for Form 8949 reporting.

Do I Need to File Form 8949 as a U.S. Expat?

Short-Term vs. Long-Term Capital Gains on Form 8949

The length of time you hold an asset determines your tax rate and which part of Form 8949 it belongs in:

| Holding Period | Classification | Form 8949 Section | Tax Rate |

|---|---|---|---|

| One year or less | Short-term | Part I | Ordinary income rates |

| More than one year | Long-term | Part II | Preferential long-term capital gains rates (0%, 15%, or 20%) |

Form 8949 implication: Even one extra day of holding can shift a transaction from Part I to Part II of Form 8949 and change your tax rate substantially. Always document your acquisition date carefully and verify it against broker statements before completing the form.

For the current year’s brackets, NIIT thresholds, and how rates apply specifically to expats, see our complete guide to foreign capital gains tax for US expats.

How to Complete Form 8949: A Step-by-Step Guide

Step 1: Gather Your Transaction Records

Collect all documentation for investment sales during the tax year:

- Form 1099-B from U.S. brokers (if applicable)

- Form 1099-DA from digital asset brokers

- Foreign broker statements showing buy and sell transactions

- Real estate closing statements

- Records of purchase dates, amounts, and capitalized improvement costs

Step 2: Categorize Your Transactions

Each transaction goes into one of twelve box categories based on holding period, asset type, and what was reported to the IRS:

| Asset Type | Holding Period | Basis Reported | Box |

|---|---|---|---|

| Traditional securities | Short-term | Yes (on 1099-B) | A |

| Traditional securities | Short-term | No (on 1099-B) | B |

| Traditional securities | Short-term | No 1099-B received | C |

| Traditional securities | Long-term | Yes (on 1099-B) | D |

| Traditional securities | Long-term | No (on 1099-B) | E |

| Traditional securities | Long-term | No 1099-B received | F |

| Digital assets | Short-term | Yes (on 1099-DA) | G |

| Digital assets | Short-term | No (on 1099-DA) | H |

| Digital assets | Short-term | No 1099-DA received | I |

| Digital assets | Long-term | Yes (on 1099-DA) | J |

| Digital assets | Long-term | No (on 1099-DA) | K |

| Digital assets | Long-term | No 1099-DA received | L |

For most expats using foreign brokers that do not issue Form 1099-B or 1099-DA, you will check Box C or Box F for traditional securities and Box I or Box L for digital assets.

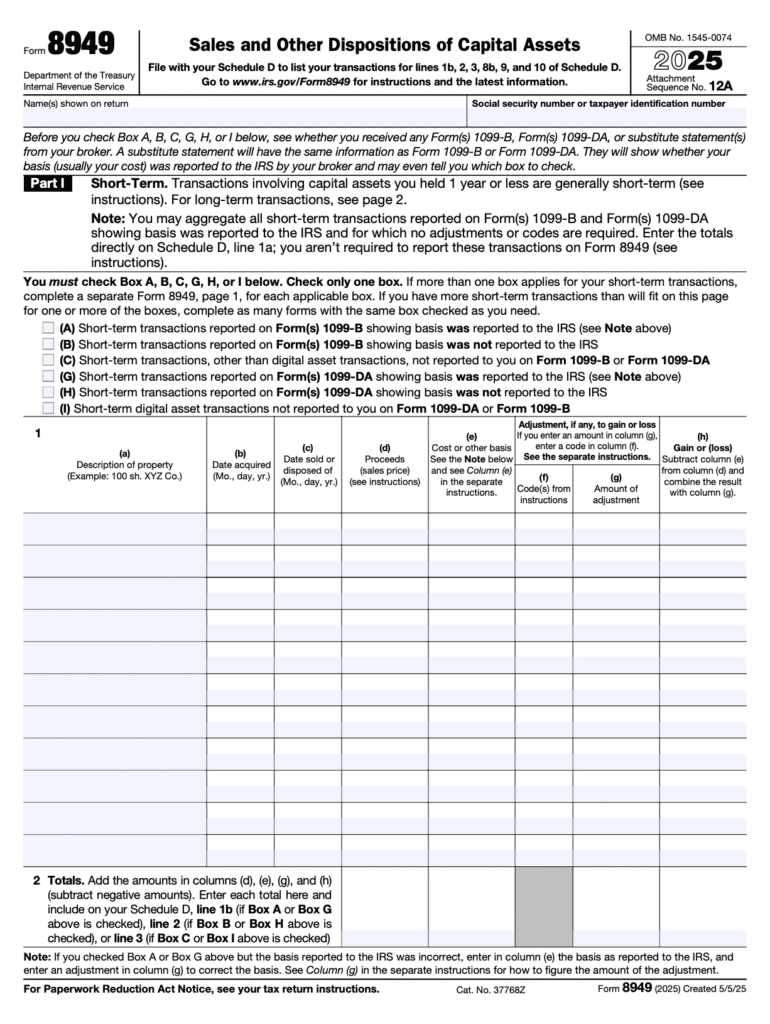

Step 3: Complete Each Column for Every Transaction

Form 8949 has eight columns. Enter the following for each transaction, and see the image below to map the information outlined in the chart to the actual form.

| Column | What to Enter | Example |

|---|---|---|

| (a) Description | What you sold | “100 shares XYZ Corp” or “0.5 BTC” |

| (b) Date acquired | Purchase date | 03/15/2018 |

| (c) Date sold | Sale or disposition date | 06/22/2025 |

| (d) Proceeds | Sale price in USD | $12,500 |

| (e) Cost basis | Purchase price in USD plus improvements | $8,000 |

| (f) Adjustment code | Letter code if adjustment applies | H, W, B, etc. |

| (g) Adjustment amount | Dollar amount of adjustment | -$5,000 (negative for exclusions) |

| (h) Gain or loss | (d) minus (e) plus or minus (g) | $4,500 |

Step 4: Convert Foreign Currency to USD

Convert every foreign currency amount to USD using the exchange rate on the transaction date. Use the purchase date rate for cost basis (column e) and the sale date rate for proceeds (column d).

For a comprehensive view of which exchange rates to use, where to find them, and how to handle multi-currency transactions, see our guide on IRS foreign exchange rates. Document every exchange rate used and keep this documentation with your tax records, the IRS may request it during an audit.

Step 5: Apply Adjustment Codes (If Needed)

If a transaction needs an adjustment, enter the code in column (f) and the dollar amount in column (g). Common adjustment codes:

| Code | When to Use |

|---|---|

| B | Incorrect cost basis reported on Form 1099-B or 1099-DA |

| E | Selling expenses not reflected in reported proceeds |

| H | Section 121 exclusion of gain from sale of primary residence |

| W | Wash sale loss disallowed (now applies to digital assets in 2025) |

For Section 121 exclusions and wash sale adjustments, the adjustment amount in column (g) is entered as a negative number to reduce the gain.

Step 6: Transfer Totals to Schedule D

Add the totals from each Form 8949 page (one set of totals per box category used) and transfer them to the corresponding lines on Schedule D. Schedule D calculates your overall net capital gain or loss, which then flows to your Form 1040.

Reporting Foreign Property Sales on Form 8949

When you sell property abroad, the IRS treats it as a capital asset sale. To fill out Form 8949 correctly, you need three main pieces of information:

- What you paid (Cost Basis): This is the original purchase price plus any major home improvements (like a new roof or a kitchen remodel). You must convert these amounts to USD using the exchange rate from the date of the purchase or improvement.

- What you received (Sale Proceeds): This is the final sale price minus costs like agent commissions and legal fees. Convert this to USD using the exchange rate from the date of the sale.

- How long you owned it: If you owned the home for more than one year, it is a long-term sale (Part II of the form). One year or less is short-term (Part I).

Common Codes for Property Sales

You may need to use “Adjustment Codes” in Column (f) to tell the IRS more about the sale:

- Code H (The Home Sale Exclusion): If the property was your primary home and you meet the IRS rules (Section 121), you can often exclude up to $250,000 (or $500,000 for couples) of the profit from your taxes. You list the profit you’re “hiding” from the tax bill as a negative number in Column (g).

- Code O (Other Expenses): Use this if you have selling costs—like foreign transfer taxes or legal fees—that weren’t already subtracted from your sale price.

Is it a Home or a Rental?

The “path” your information takes through the tax return changes depending on how the property was used:

- If it was your home: The information goes directly onto Form 8949.

- If it was a rental: The sale is reported on Form 4797 first. This is because the IRS needs to “recapture” (tax) the depreciation deductions you took while renting the property. Only the final result of that form moves over to your Form 8949 or Schedule D.

For more details on home sale exclusions, how to handle rental depreciation, or what to do if your sale money is sitting in a foreign bank account, see our guide to foreign property tax for U.S. expats.

The Foreign Tax Credit and Form 8949

If you paid foreign tax on a capital gain, the Foreign Tax Credit (FTC) is claimed separately on IRS Form 1116. It is not reported directly on Form 8949, because this form is specifically about the asset. They want to know what you sold, what it cost to buy, and what your profit was when you sold it (in US Dollars).

Form 8949 is used to calculate what you made (your profit), while Form 1116 calculates how much you already paid in taxes to another country. Keeping them separate prevents “double-dipping” and ensures your foreign tax credit is applied as a dollar-for-dollar reduction of your U.S. tax bill, rather than just a deduction from your income.

To ensure your return is technically accurate and avoids IRS matching notices, follow these two rules:

1. Report the “Gross” Gain (Before Foreign Taxes)

You have to report your sale proceeds (the total amount you received) and cost basis (what you originally paid for the asset) exactly as they occurred.

- The Rule: Do not subtract foreign taxes from your total sale amount.

- The Logic: Form 8949 is used to calculate your realized gain, or, said more simply, the actual profit you made on the investment. The foreign tax you paid is a separate credit that reduces your U.S. tax bill later, rather than reducing the profit itself.

2. Do Not Use Column (g) for Foreign Taxes

Column (g) on Form 8949 is titled “Adjustments.”

- What stays out: Foreign tax payments.

- What goes in: This column is strictly for specific “math corrections,” such as the Section 121 primary residence exclusion (where you don’t pay tax on a home sale) or cost basis corrections.

- Where it goes instead: Foreign tax paid is listed in Part II of Form 1116.

The Flow of Information: From Sale to Credit

To visualize how your profit moves through the tax return:

- Form 8949: You list the “Raw Data” (What you paid vs. what you sold it for).

- Schedule D: This form totals those numbers to find your Net Profit.

- Form 1040: The IRS calculates the U.S. tax owed on that profit.

- Form 1116: This is where you show the tax you already paid abroad to reduce the U.S. tax bill from Step 3.

For the underlying rules on when the Foreign Tax Credit applies to capital gains, how to calculate it for foreign property sales, and how it interacts with the Net Investment Income Tax, see our complete guide to foreign capital gains tax for US expats.

Reporting Cryptocurrency on Form 8949

The IRS treats cryptocurrency as property. This means every time you “get rid” of it, it counts as a sale that must be reported on Form 8949.

What counts as a sale?

You must report the transaction if you:

- Sell crypto for cash (USD or foreign currency).

- Swap crypto, such as trading Bitcoin for Ethereum.

- Spend crypto to buy a product or pay for a service.

- Receive crypto as pay and later sell or spend it.

For every trade, you need to track four things: the date you bought it, the date you sold it, what you paid for it (in USD), and what it was worth when you sold it (in USD).

Which boxes should you check for 2025?

The IRS now has specific categories just for digital assets. For the 2025 tax year, use these boxes:

- Short-term (held for a year or less): Use Boxes G, H, or I.

- Long-term (held for more than a year): Use Boxes J, K, or L.

Most expats use foreign exchanges that do not send reports to the IRS. In this case, you will likely check Box I (for short-term) or Box L (for long-term) and provide your own transaction records.

For more details on tracking your crypto across different wallets, reporting foreign accounts (FBAR), or how currency exchange rates affect your crypto, see our cryptocurrency tax guide for U.S. expats.

What Is the Difference Between Form 8949 and FBAR?

Form 8949 and the FBAR serve completely different purposes:

| Feature | Form 8949 | FBAR (FinCEN Form 114) |

|---|---|---|

| Purpose | Reports capital gains and losses from selling investments | Reports foreign financial account balances |

| Filed with | IRS (attached to your tax return) | FinCEN (filed separately from your tax return) |

| Determines taxes owed? | Yes | No (informational only) |

| Threshold | Any capital gain or loss | Foreign accounts exceeding $10,000 aggregate |

| Deadline | April 15 (June 15 for expats) | April 15 (automatic extension to October 15) |

You may need both forms if you sold investments held in foreign brokerage accounts (Form 8949) and have foreign accounts totaling over $10,000 (FBAR). If your foreign financial assets exceed FATCA thresholds, you may also need Form 8938. See our FBAR vs. FATCA comparison for details on when each applies.

Common Form 8949 Mistakes to Avoid

Form 8949 is one of the most common places for errors on an expat return. Between foreign brokers, multiple currencies, and new reporting rules for 2025, it is easy for small mistakes to trigger an IRS inquiry. Here are the most frequent errors we see at Greenback:

- Assuming foreign accounts don’t need to be reported: Even if a foreign broker doesn’t send you a tax form (like a 1099-B), you are still required to report every worldwide sale. The IRS matches data from thousands of foreign banks to your return.

- Estimating exchange rates: You cannot use an average “year-end” rate or a rough guess. You must use the specific exchange rate for the day the transaction happened. Using the wrong rate can lead to under-reporting your actual profit.

- Using the wrong categories for crypto: For the 2025 tax year, digital assets have their own checkboxes (Boxes G through L). Do not use the traditional stock categories (Boxes A through F) for your crypto trades.

- Mixing different types of sales on one page: You cannot combine short-term and long-term sales on the same Form 8949 page. Each category needs its own separate section or its own physical form.

- Misunderstanding “Wash Sales” on crypto: Under the new 2025 rules (from the One Big Beautiful Bill), crypto is now subject to the same wash sale rules as stocks. If you sell crypto at a loss and buy it back within 30 days, you cannot claim that loss. It must be reported as a “disallowed loss” using Code W.

- Subtracting foreign taxes from your profit: Always report the “gross” amount (your full sale price). You claim the foreign taxes you paid later on Form 1116. If you subtract them on Form 8949, the IRS will think you’re “double-dipping” on your tax benefits.

- Forgetting “swaps” or “trades”: Many expats forget that trading one cryptocurrency for another (like Bitcoin for Ethereum) is a taxable sale. You have to report these trades individually, even if you never “cashed out” to a bank account.

Frequently Asked Questions

Yes. You must report all capital gain and loss transactions on Form 8949 regardless of whether you received a 1099-B or 1099-DA. Foreign brokers typically do not report to the IRS, which means you are responsible for tracking and reporting every transaction. Use Box C or F for traditional securities or Box I or L for digital assets to indicate these were not reported on a broker form.

No. Capital gains are unearned income and do not qualify for the FEIE. The Foreign Tax Credit on Form 1116 is the right tool when you have paid foreign tax on a gain. For more on how the FTC interacts with capital gains, see our foreign capital gains tax guide for US expats.

Use the exchange rate on the date of each transaction. Apply the purchase date rate to your cost basis and the sale date rate to your proceeds. For more detail on which rates to use and how to handle multi-currency transactions, see our guide on IRS foreign exchange rates.

Yes. The IRS treats cryptocurrency as property, so every disposition (selling crypto for fiat, swapping one crypto for another, or using crypto to pay for goods or services) is a taxable event reported on Form 8949. For 2025, use Boxes G through L for digital asset transactions instead of the traditional Boxes A through F.

Yes. Every exchange of one cryptocurrency for another is a taxable event. Calculate the gain or loss based on the fair market value of the crypto received versus your cost basis in the crypto you sold. Report each swap as a separate transaction on Form 8949.

Report the sale on Form 8949 and Schedule D. If the home was your primary residence and you meet the Section 121 ownership and use tests, you may exclude up to $250,000 of gain ($500,000 married filing jointly) using adjustment code “H” in column (f). For the full Section 121 rules, see our foreign capital gains tax guide for US expats.

Yes. If your total capital losses exceed your total capital gains for the year, you can deduct up to $3,000 of net capital loss against ordinary income ($1,500 if married filing separately). Any remaining losses carry forward indefinitely to future years. This calculation is done on Schedule D, not Form 8949 itself.

You can file an amended return (Form 1040-X) to correct errors. Common reasons expats amend include unreported foreign investment sales, incorrect currency conversions, missed Foreign Tax Credits, and miscalculated cost basis. If you have multiple years of unfiled or incorrect returns, our Streamlined Filing Compliance Services may help you catch up without penalties.

You always report the full gain on Form 8949, regardless of foreign tax paid. The Foreign Tax Credit is claimed separately on Form 1116, which reduces your overall US tax bill. Do not subtract foreign taxes from the gain on Form 8949 itself.

Get Expert Help With Form 8949

Form 8949 can become complex quickly when you are dealing with foreign brokers, multiple currencies, digital assets, and potential tax credits. Many of our expat clients at Greenback come to us after attempting to file on their own and realizing they are over their heads.

If you are ready to be matched with a Greenback accountant, get started here. For general questions about expat taxes or working with Greenback, contact our Customer Champions.

Make Sure Your Investment Sales Are Reported Correctly

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently, and individual circumstances vary. Always consult with a qualified tax professional about your specific situation.

Related Resources

- Schedule D (Form 1040) for Expats

- Foreign Tax Credit Guide

- Form 1116: How to Claim the Foreign Tax Credit

- Cryptocurrency Taxes for U.S. Expats

- Capital Gains Tax on Foreign Property

- Capital Gains Tax on Inherited Property

- FEIE vs. Foreign Tax Credit

- FBAR Filing Requirements

- FBAR vs. FATCA Comparison

- Form 8621: PFIC Reporting