Do I Need Form 1310 to Claim a Tax Refund for a Deceased Family Member?

You need Form 1310 only if you are claiming a tax refund on behalf of a deceased taxpayer and you are not a surviving spouse filing a joint return or a court-appointed personal representative. If either of those exceptions applies to you, you can claim the refund without this form.

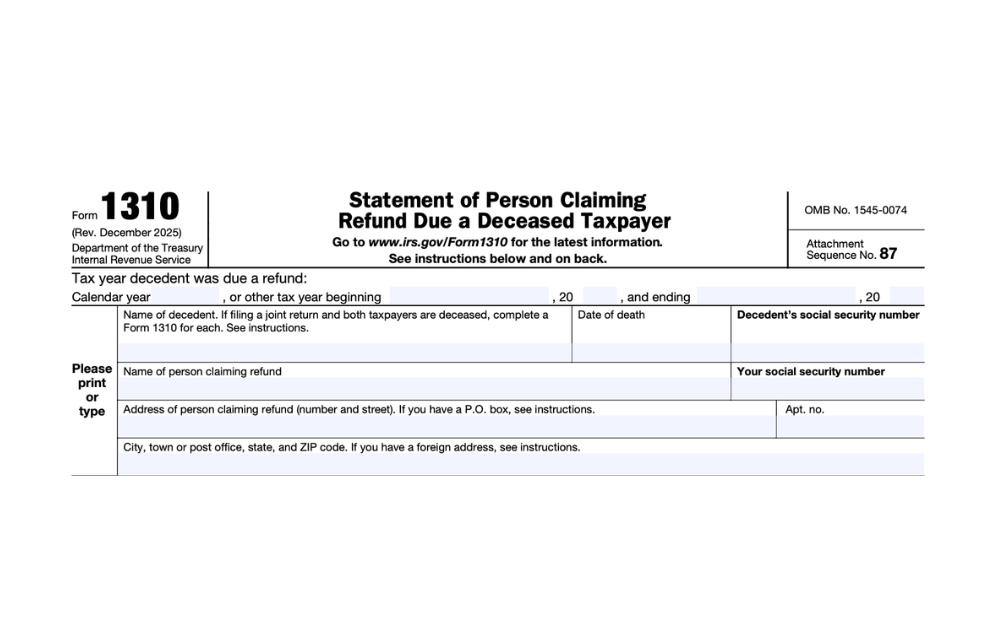

According to the IRS, Form 1310 (“Statement of Person Claiming Refund Due a Deceased Taxpayer”) is a one-page form that authorizes the IRS to release a refund to someone other than the deceased taxpayer. It’s filed with the decedent’s final Form 1040 when a refund is due. Common situations that require it include:

- Adult children handling a parent’s final tax return without a formal court appointment

- Siblings or other relatives managing the deceased’s tax affairs informally

- Executors named in a will who have not yet received official court documentation

Need Help Claiming a Refund for a Loved One?

Here’s exactly who needs this form, who doesn’t, and how to file it correctly, including from abroad.

Who Does NOT Need Form 1310?

Two groups can claim a deceased taxpayer’s refund without filing Form 1310:

| You Are | What to Do Instead | Documentation Required |

|---|---|---|

| Surviving spouse filing a joint return for the year of death | File the joint return normally; the IRS considers you married for the full year your spouse died | Write “DECEASED,” the decedent’s name, and date of death across the top of the return |

| Court-appointed personal representative filing the original return | File the return and attach a copy of the court certificate showing your appointment | Court certificate (a will or power of attorney is not acceptable as proof) |

If you are a court-appointed representative filing an amended return (Form 1040-X) or a claim for refund on Form 843, you must attach Form 1310 along with your court certificate, even if you previously filed the certificate with the IRS.

Who DOES Need Form 1310?

Anyone else claiming a refund on behalf of the deceased taxpayer needs to file Form 1310. This typically includes:

- Family members handling tax affairs without going through probate

- Executors named in a will who have not yet obtained a court appointment

- Anyone acting as an informal personal representative

When you check Line C on the form (the “other person” category), you must also complete Part II, which asks whether a court has appointed a personal representative and whether you expect one to be appointed. You also certify that you will distribute the refund according to applicable state laws.

How to File Form 1310

The form itself is straightforward. Here’s what each part requires:

Top section: Your name, SSN, and address (foreign addresses are accepted), plus the decedent’s name, SSN, and date of death.

Part I: Check one box identifying your role:

- Line A: Surviving spouse requesting reissuance of a refund check

- Line B: Court-appointed personal representative (attach court certificate)

- Line C: Other person claiming the refund (must complete Part II)

Part II (Line C filers only): Answer yes/no questions about whether a personal representative has been appointed or will be appointed, and whether you’ll distribute the refund under applicable laws.

Part III: Sign and date the form.

Filing Details

| Question | Answer |

|---|---|

| Where to file | Attach to the decedent’s final Form 1040 and mail to the appropriate IRS address for the deceased’s state of residence. Expats should use the overseas filing address. |

| Can it be e-filed? | Some tax software supports electronic filing of Form 1310. Discuss with your preparer to avoid errors. |

| Deadline | Three years from the original due date of the return. For a 2025 return (due April 15, 2026), the deadline is April 15, 2029. |

| Death certificate | Do NOT attach it to the return. Per IRS Publication 559, keep the death certificate for your records and provide it only if the IRS requests it. |

| Separate copy needed? | If the final return was already filed, you can mail Form 1310 separately, but this may slow processing. |

Common Documentation Mistakes

The original article on this page previously stated that you should always attach a death certificate and may want to include a will or power of attorney. The IRS instructions clarify that:

- Death certificates should be kept for your records, not attached to the return

- A will is not acceptable as proof of personal representative status; only a court appointment certificate qualifies

- A power of attorney does not establish authority to claim a refund for a deceased person, since a POA terminates at death

What Expats Should Know

Filing Form 1310 from abroad adds a few practical considerations, though the form itself works the same way regardless of where you live.

- Foreign addresses are accepted. The form specifically accommodates international addresses. Enter your city, province, postal code, and country name (do not abbreviate) in the address fields.

- Refund delivery options. The IRS can send a refund check to a foreign address, but depositing a U.S. Treasury check at a foreign bank may involve fees or delays. If you have a U.S. bank account, providing that account information for direct deposit is usually faster and simpler.

- Mail timing. International mail to and from the IRS takes longer. If you’re filing by mail, use a trackable service and factor in additional processing time. Standard processing for Form 1310 claims is 6 to 8 weeks, but international mail can add several weeks on each end.

- Expat-specific final return considerations. If the deceased was an American living abroad, their final return may include expat-specific forms like Form 2555 (FEIE), Form 1116 (Foreign Tax Credit), or FBAR filings. The final FBAR covers accounts held up to the date of death, and the estate may have a separate FBAR obligation for accounts held during the estate administration period.

- Surviving spouse filing status. If your spouse passed away in 2025, you can file jointly for 2025 (without Form 1310) and may be eligible to file as a Qualifying Surviving Spouse for 2026 and 2027 if you have a dependent child.

Tax Implications of the Refund

A refund claimed through Form 1310 is generally not taxable income to the person receiving it. The refund represents an overpayment of the deceased’s taxes and becomes part of the estate. As the person claiming the refund, you are responsible for distributing it according to the decedent’s will or your state’s intestacy laws.

For very large estates, the refund may factor into the estate’s overall value for estate tax purposes, but this only applies to estates exceeding the federal estate tax exemption ($13.99 million for 2025).

Get Help with a Deceased Taxpayer’s Final Return

Filing a final tax return for a loved one is emotionally difficult, and the complexity increases when international tax obligations are involved. If the deceased was an American living abroad, their final return may involve the FEIE, Foreign Tax Credit, foreign account reporting, and potentially the Streamlined Filing Compliance Procedures if prior returns were unfiled.

Have questions about filing a final return or claiming a refund? Contact us, and one of our Customer Champions will gladly help. If you need specific advice on your situation, you can also get a consultation with one of our expat tax experts.

Let Us Handle the Paperwork So You Don’t Have To

This article is for informational purposes only and does not constitute legal or tax advice. Estate and tax refund rules vary by state and situation. For guidance on your specific circumstances, contact Greenback to speak with an expat tax specialist.

Related Resources

- Form 1040: U.S. Individual Income Tax Return

- Foreign Earned Income Exclusion

- Foreign Tax Credit Guide

- FBAR Filing Requirements

- U.S. Expat Tax Forms: What You Need to File

- What Happens If I File My Taxes Late?

- Streamlined Filing Compliance Procedures

- U.S. Expat Taxes: The Complete Guide

- Tax Refunds for U.S. Expats

- Why Do U.S. Citizens Living Abroad Pay Taxes?