Form 14653 Explained: The Certification Statement for Streamlined Filing

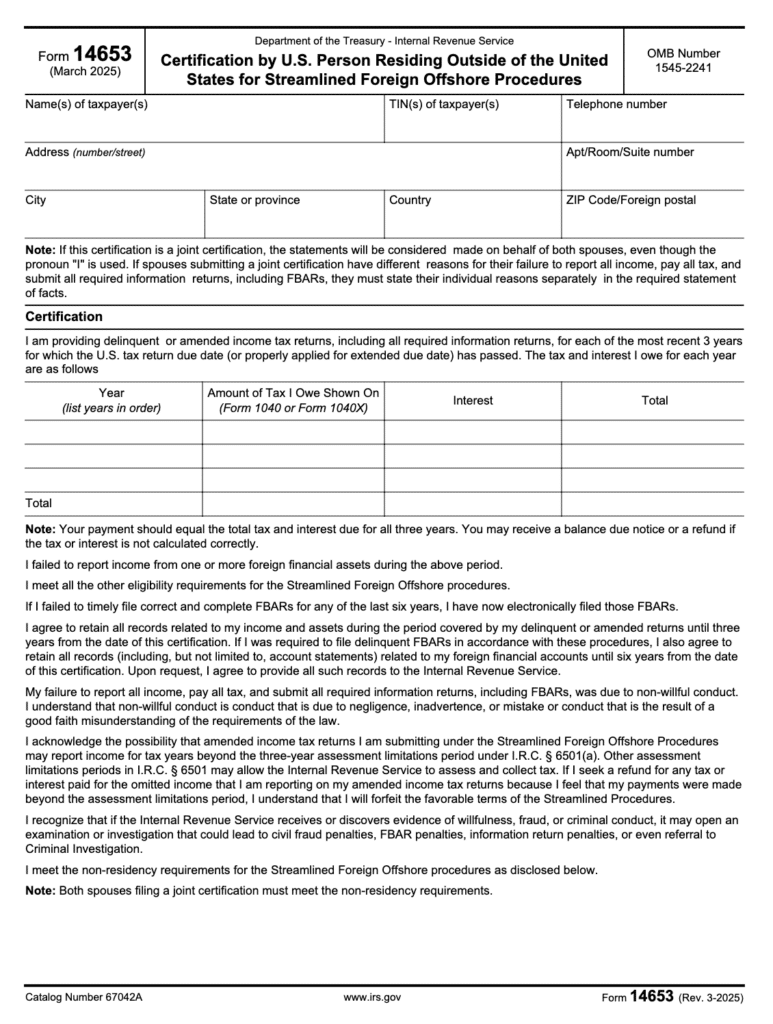

Form 14653, officially called the “Certification by U.S. Person Residing Outside of the United States for Streamlined Foreign Offshore Procedures,” is the IRS form you must submit when using the Streamlined Filing Compliance Procedures to catch up on delinquent U.S. tax returns without facing penalties. According to the IRS, this form certifies that your failure to file was non-willful, which is the critical requirement for penalty-free compliance through the Streamlined program.

The Streamlined Filing Procedures have helped thousands of U.S. expats get compliant since the program launched in 2012. When you file this way, there’s no set timeline for when the IRS will review your late returns and FBARs, but the important thing is that you’ve submitted everything to get caught up. Form 14653 is your certification that you qualify for this penalty relief.

Form 14653 Is Required for Streamlined Filing

What is Form 14653?

Form 14653 is the certification document required when you use the Streamlined Foreign Offshore Procedures to catch up on unfiled U.S. tax returns. You must complete and submit it along with three years of delinquent tax returns and six years of delinquent FBARs.

The form serves one critical purpose: to certify under penalty of perjury that your failure to file was non-willful. “Non-willful” means you didn’t intentionally or recklessly disregard your U.S. tax filing obligations. Common non-willful reasons include not knowing you had to file, receiving incorrect advice, or genuinely misunderstanding your obligations as a U.S. expat.

The IRS uses Form 14653 to screen Streamlined program applicants and ensure only truly non-willful taxpayers receive penalty relief. If you admit willfulness in your statement of facts on this form, your application will be denied.

How Do I Complete the Narrative Statement of Facts?

The most challenging part of Form 14653 is the “Narrative Statement of Facts” section. The IRS requires you to submit a written explanation of the specific facts that led to your failure to report all income, pay all taxes, and submit all required information returns, including FBARs.

What You Must Include in Your Statement

Your narrative statement must address:

Background Information:

- Personal and financial circumstances during the years you failed to file

- Where you lived and worked during the delinquent years

- Your education level and professional background

- Any language barriers or cultural factors relevant to your situation

Foreign Account Details:

- How and when you opened each foreign financial account

- Source of funds in the accounts (inheritance, employment income, business proceeds, savings from abroad, etc.)

- Your level of contact with the accounts (withdrawals, deposits, investment decisions)

- Whether you managed the accounts yourself or had a financial advisor

How You Discovered Your Filing Requirements:

- When and how you learned you had U.S. filing obligations

- What you did after learning about your obligations

- How quickly you took action to become compliant

Tax Professional History:

- Contact information for any tax professional you worked with previously

- What advice they gave you about filing requirements

- Why that advice led to non-compliance

Physical Presence Certification:

- If you’re a U.S. citizen or green card holder: Certification that you spent more than 330 days outside the U.S. in at least one of the last three years

- If you’re not a U.S. citizen or green card holder and don’t currently live in the U.S.: A list of all days you spent in the U.S. during the last three years (this determines whether you pass the Substantial Presence Test and are treated as a U.S. person for tax purposes)

The 330-day requirement for Streamlined eligibility is different from the Physical Presence Test used for the Foreign Earned Income Exclusion. For FEIE, you need 330 days in any consecutive 12-month period. For Streamlined eligibility, you need 330 days outside the U.S. in at least one of the last three calendar years.

For Married Couples: If you’re filing jointly and you and your spouse have different reasons for non-compliance, you must list each person’s individual reasons separately in the statement.

How Long Should My Statement Be?

The IRS wants complete, specific facts, not a novel. A thorough one-page statement is typically sufficient. More than ten pages is excessive and will likely annoy the reviewer.

Focus on facts that explain why your failure to file was genuinely non-willful:

- “I moved to Germany in 2018 for work and opened a local bank account for my salary. My German colleagues told me U.S. expats didn’t need to file U.S. taxes if they paid taxes in Germany. I believed this until I read an article in 2024 explaining my actual obligations.”

- “I inherited a bank account in Japan from my grandmother in 2019. I didn’t know foreign inheritances triggered FBAR reporting requirements.”

- “I was a dual citizen from birth and never lived in the U.S. My parents never filed U.S. taxes for me, and I didn’t know I had U.S. filing obligations until my bank flagged my account under FATCA in 2024.”

Be honest. Include facts that help your case and any that might hurt it. The IRS wants transparency, not perfection.

What Not to Say

Never include statements that suggest willfulness:

- “I knew I should file, but didn’t have time.”

- “I thought the IRS wouldn’t find out.”

- “I was hiding my foreign accounts.”

- “I ignored letters from the IRS.”

These admissions will disqualify you from the Streamlined program immediately.

Who Qualifies for Streamlined Filing?

You can use the Streamlined Foreign Offshore Procedures if you meet these requirements:

Residency Requirement: You must have spent more than 330 days outside the U.S. in at least one of the most recent three years for which you have U.S. tax filing obligations.

Filing Requirements:

- Three years of delinquent U.S. tax returns for which the due dates (including extensions) have passed

- Six years of delinquent FBARs for which the due dates (including extensions) have passed

If you didn’t have foreign financial accounts totaling more than $10,000 in any of the six FBAR years, you must explain why FBAR wasn’t required for those specific years.

Non-Willfulness Requirement: Your failure to file must have been non-willful. This is what Form 14653 certifies.

What Happens After You Submit Form 14653?

After you mail your Streamlined package (three years of returns, six years of FBARs, and Form 14653) to the IRS, there’s no set processing timeline. Some taxpayers receive confirmation within months; others wait over a year.

The IRS may:

- Accept your submission without further contact (most common for straightforward cases)

- Request additional information or documentation

- Audit one or more of your submitted returns

- Reject your submission if they determine your conduct was willful

Once accepted, you’re compliant and caught up on your U.S. tax obligations with no penalties assessed.

The IRS terminated the Offshore Voluntary Disclosure Program (OVDP) in 2018, which was another amnesty program that helped willfully noncompliant taxpayers become compliant without facing prosecution. All amnesty programs are offered at the IRS’s discretion and can be terminated at any point. Though the IRS typically gives notice before terminating an amnesty program, your best option is to use these programs before they’re no longer offered.

Are you a late filer looking for guidance? Whether you’re one year behind or many, our late filer services provide the clarity, support, and expertise you need to get back on track. We’ve helped thousands of U.S. expats catch up penalty-free, and we’ll walk you through every step of the process with patience and understanding.

What If I Don’t Qualify for Streamlined Filing?

If you don’t meet the 330-day foreign residency requirement, you may qualify for the Streamlined Domestic Offshore Procedures instead (which includes a 5% penalty on unreported foreign assets but still eliminates the more severe FBAR penalties).

If your conduct was willful, the Streamlined program is not available to you. You should consult with a tax attorney about other options for coming into compliance.

Behind on your U.S. expat taxes? If you’ve been living abroad and didn’t realize you needed to file U.S. tax returns, or you’ve fallen behind on your FBAR obligations, our Streamlined Filing services for late filers can help you get compliant without the stress. We’ve helped thousands of expats catch up penalty-free through the Streamlined procedures, and we’ll handle Form 14653 and all required documentation for you. You’ll have peace of mind knowing your submission is complete, accurate, and positions you for the best possible outcome.

Get Expert Help with Form 14653 and Streamlined Filing

Our team of dedicated CPAs and IRS Enrolled Agents has particular expertise in helping U.S. expats get caught up using the Streamlined program. We’ll help you craft a compelling narrative statement that demonstrates non-willfulness, prepare all required tax returns and FBARs, and ensure your submission is complete and accurate.

No matter how late, messy, or complex your situation may be, we can help. You’ll have peace of mind knowing that your taxes were done right and your Streamlined submission positions you for penalty-free compliance.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

Get Form 14653 Right the First Time

Disclaimer: This article provides general information about Form 14653 and Streamlined Filing Compliance Procedures. Tax laws can be complex and change frequently. For advice specific to your situation, consult with a qualified tax professional.

Related Resources

- Streamlined Filing for U.S. Expats: Your Penalty-Free Path to Tax Compliance

- FBAR: What It Is, Who Must File & How To Report Foreign Accounts

- Form 1040 for U.S. Expats: Filing Made Simple

- Physical Presence Test: Requirements and Day Counting

- Substantial Presence Test: Complete Guide

- Form 4868 for U.S. Expats: Extension Filing Explained

- Why Do I Have to Pay U.S. Taxes If I Live Abroad?

- U.S. Expat Taxes: The Complete Guide for Americans Living Abroad