Form 843 Explained: How to Claim a Refund or Penalty Abatement

- What is IRS Form 843?

- The December 2024 Redesign Changed Where Every Entry Goes

- The Kwong Ruling Made Form 843 the Path to COVID-Era Penalty Refunds

- Form 843 and Form 1040-X Cover Different Refunds

- Who Needs to File IRS Form 843?

- How to File IRS Form 843?

- Penalty Abatement Is the Most Common Use of Form 843

- Form 843 Claims Move on a Slower IRS Track

- A Few Common Mistakes Sink Form 843 Claims

- Frequently Asked Questions About Form 843

- Related Resources

Form 843, Claim for Refund and Request for Abatement, is the IRS form you use to ask for a refund of certain taxes, penalties, interest, or fees you have already paid, or to ask the IRS to remove (abate) penalties it has assessed but not yet collected. It is not used for income tax refunds (those go on Form 1040-X). For most reasons on the form, it cannot be e-filed and must be mailed on paper to the address tied to the underlying tax or notice. As of July 2026, one narrow exception exists: individual taxpayers with an IRS Online Account can e-file a Kwong v. United States claim for fully paid interest and penalties. The form was redesigned in December 2024, so the current version is Form 843 (Rev. 12-2024).

You may need Form 843 if:

- You want a penalty abated for failure to file, failure to pay, or an accuracy-related penalty when you have reasonable cause

- You qualify for first-time abatement (FTA) because your prior three years are clean

- You already paid a penalty you believe was wrongly assessed, including COVID-era late-filing penalties under the Kwong ruling

- You need a refund of Social Security or Medicare tax wrongly withheld that your employer will not return

We File Form 843 for Americans, Correctly and on Time.

Below, you will find what Form 843 covers, what changed in the December 2024 redesign, how to file it line by line, and the situations where it matters most for U.S. taxpayers, including Americans abroad.

What is IRS Form 843?

IRS Form 843, officially titled Claim for Refund and Request for Abatement, is the IRS’s general-purpose claim form for two related but distinct asks:

- A refund of certain taxes (other than income tax), interest, penalties, additions to tax, or fees you have already paid

- An abatement of certain penalties, additions to tax, or interest the IRS has assessed but you have not yet paid

The form runs two pages and asks you to identify your reason for filing, the tax period, the amount, the type of tax and return involved, the Internal Revenue Code section behind any penalty, and the facts that support your claim. The written explanation on Line 8 is where most successful claims live or die.

Form 843 is not connected to your annual income tax return. You file it separately, on paper, to the IRS address tied to the underlying tax or notice, unless you qualify for the narrow Kwong e-filing exception described below.

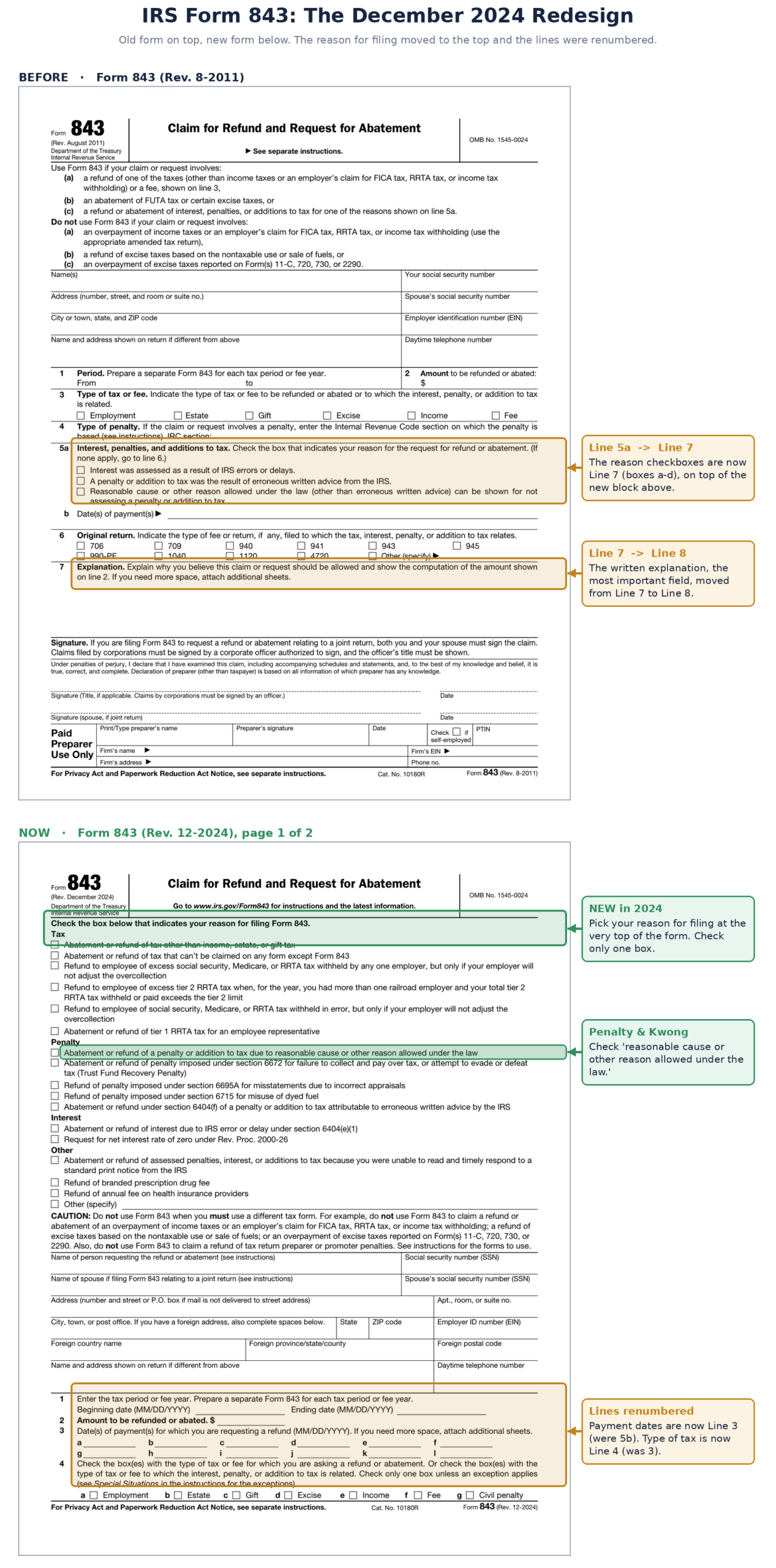

The December 2024 Redesign Changed Where Every Entry Goes

The IRS redesigned Form 843 in December 2024. If you are working from an older guide, a prior return, or a sample you saved years ago, the line numbers will not match the form in front of you. The biggest change: your reason for filing is now a set of checkboxes at the very top of the form, above your name, grouped under Tax, Penalty, Interest, and Other. You check exactly one. The rest of the form was renumbered around it.

A few of the boxes themselves also changed. Line 4 now includes a Fee box and a Civil penalty box, and Line 5 now lists more return types (944, 945, CT-2, and the Branded Prescription Drug Fee). The signature block added space for an Identity Protection PIN. Always download the current form straight from IRS.gov so you are working from Rev. 12-2024.

The Kwong Ruling Made Form 843 the Path to COVID-Era Penalty Refunds

A federal court ruling in Kwong v. United States opened a pathway to refunds for taxpayers who paid late-filing penalties on returns due between January 20, 2020, and July 10, 2023. The decision held that automatic late-filing penalties were not properly assessed during the COVID-19 disaster period for affected taxpayers, and that refund claims could be filed on Form 843.

The key deadline is July 10, 2026, the protective-claim deadline for affected taxpayers to file Form 843. The general statute of limitations under IRC Section 6511, 3 years from filing or 2 years from payment, whichever is later, continues to apply.

As of July 2026, individual taxpayers with an existing IRS Online Account can file a Kwong claim for fully paid interest and penalties electronically, rather than mailing the paper form. According to the IRS, this is currently the only reason for filing Form 843 that qualifies for e-filing.

If you paid a late-filing penalty on a return filed during the COVID disaster window, you may be eligible for a refund. Our full Kwong article walks through transcript review, protective claims, and exactly what to write on Line 8.

The Kwong July 10 Deadline Is Close. Did You Pay a COVID-Era Penalty?

Form 843 and Form 1040-X Cover Different Refunds

Form 843 covers a specific lane in the IRS refund-and-abatement system. The most common mix-up is between Form 843 and Form 1040-X, the form you use to amend an income tax return.

| If you want to | Use this form |

|---|---|

| Refund or abate penalties or interest the IRS assessed | Form 843 |

| Refund Social Security or Medicare tax wrongly withheld (and your employer will not refund it) | Form 843 |

| Refund excise tax, employment tax, or certain other non-income taxes | Form 843 |

| Amend your income tax return to claim a refund of income tax | Form 1040-X |

| Extend your filing deadline | Form 4868 (expats can also use Form 2350) |

| Make a voluntary disclosure | Form 14457 |

If your refund relates to income tax shown on your Form 1040 (a missed deduction, a missed credit, an overstated income figure), Form 843 is the wrong form. Use Form 1040-X.

Who Needs to File IRS Form 843?

Form 843 is not tied to one type of filer. It is used by:

- U.S. taxpayers seeking penalty abatement after receiving a notice (CP14, CP501, CP503, CP504, or similar)

- Taxpayers who have already paid a penalty they believe was incorrectly assessed

- Workers requesting a refund of wrongly withheld Social Security or Medicare tax, including F-1 students, J-1 scholars, members of religious orders, and certain foreign workers

- Taxpayers requesting interest abatement due to unreasonable IRS error or delay (a high bar)

- Eligible filers claiming a refund of COVID-era late-filing penalties under the Kwong ruling, with a deadline of July 10, 2026

- U.S. expats asserting reasonable cause for a missed deadline due to expat-specific circumstances, such as a foreign mail disruption, illness abroad, or a tax preparer’s failure

How to File IRS Form 843?

Form 843 is a paper-only filing for nearly every reason for filing. The one exception: individual taxpayers with an IRS Online Account filing a Kwong claim for fully paid penalties or interest can e-file instead. Here is the process for the current Rev. 12-2024 form, in order.

- Check your reason for filing at the top of the form. This checkbox block sits above your name. For a penalty claim, check “Abatement or refund of a penalty or addition to tax due to reasonable cause or other reason allowed under the law.” Check only one box.

- Complete the identifying information: name, address, SSN or EIN, and your spouse’s SSN if the claim relates to a joint return.

- Line 1: Enter the tax period (a beginning date and an ending date).

- Line 2: Enter the dollar amount of the refund or abatement you are requesting.

- Line 3: Enter the date or dates you paid, if you are claiming a refund of something you have already paid. Entering a payment date here is what signals a refund rather than an abatement.

- Line 4: Check the type of tax or fee the claim relates to (Employment, Estate, Gift, Excise, Income, Fee, or Civil penalty).

- Line 5: Check the type of return the item relates to. Box i is 1040.

- Line 6: Enter the Internal Revenue Code section the penalty is based on, if you know it. It is usually shown on the IRS notice.

- Line 7: Check the box for your reason: a interest from IRS error or delay, b a penalty from erroneous IRS written advice, c reasonable cause or other reason allowed under the law, or d none of the above.

- Line 8: Explain why the claim should be allowed and show how you computed the amount on Line 2. Cite specific facts and dates. This is the most important section.

- Sign and date the form, and attach supporting documents: a copy of the IRS notice, medical records, mail receipts, professional advice records, or other evidence of reasonable cause.

- Mail it to the IRS address tied to the underlying tax type, listed in the Form 843 instructions. If you are responding to a specific IRS notice, mail it to the address on that notice. For Kwong claims specifically, mail to Internal Revenue Service, 1973 N Rulon White Blvd., Ogden, UT 84201, or file electronically if you have an IRS Online Account.

Keep a copy of everything. Form 843 claims can take 3 to 6 months or longer to process, especially during peak filing periods.

Important: Filing as a Protective Claim

Important: Filing as a Protective ClaimIf you are filing Form 843 to preserve your refund right while a legal or factual contingency is still pending (a court ruling on appeal, awaiting further IRS guidance, or ongoing transcript review), mark the form as a protective claim. Write “PROTECTIVE CLAIM” prominently at the top of the form, above the reason checkboxes, and add one sentence on Line 8 stating that the filing is submitted as a protective claim under Treas. Reg. Section 301.6402-2(b)(1).

For Kwong claims specifically, write “Kwong vs. United States” across the top instead, so the IRS routes the submission correctly, and add the same protective-claim sentence on Line 8.

A protective claim preserves your filing within the statute of limitations and can be supplemented later once the contingency is resolved. This is especially relevant for Kwong COVID-era penalty refund claims filed before the July 10, 2026, deadline.

Penalty Abatement Is the Most Common Use of Form 843

Penalty abatement is the single most common reason to file Form 843. The IRS assesses penalties under several categories, and Form 843 is the vehicle for asking that they be removed. Two pathways matter most.

Reasonable Cause Abatement

The IRS will abate certain penalties if you can show you exercised ordinary business care and prudence but were still unable to meet your tax obligations. The reasonable-cause categories the IRS regularly accepts include:

- Death, serious illness, or unavoidable absence of the taxpayer or an immediate family member

- Fire, casualty, natural disaster, or other disturbance that affected your ability to file or pay

- Inability to obtain records despite reasonable efforts

- Erroneous written advice from the IRS that you relied on in good faith

- Reliance on a qualified tax professional in limited circumstances

Ignorance of the law and simple oversights are rarely accepted. On a reasonable-cause claim, you check box c on Line 7, and the explanation on Line 8 should be specific, factual, and tied to dates.

First-Time Abatement (FTA)

The IRS also offers a separate First-Time Penalty Abatement for a single penalty if you meet three criteria: you filed all required returns for the prior three years, you paid or arranged to pay any tax due, and you have no prior penalties for the three preceding tax years. FTA is the easiest path when you qualify, and Form 843 is one way to claim it (you can also request FTA by phone). Our First-Time Abatement breakdown explains who qualifies and how to ask.

Form 843 Claims Move on a Slower IRS Track

The IRS reviews Form 843 claims on a non-priority track, so processing takes longer than for annual returns. A typical timeline:

- Acknowledgment: 4 to 8 weeks after the IRS receives your filing

- Decision: 3 to 6 months in most cases, sometimes longer

- Approval: the IRS adjusts your account and either refunds the money or removes the penalty

- Denial: the IRS sends a notice explaining the reason, with appeal rights

If your claim is denied, you generally have 2 years from the date of the denial to file a refund suit in U.S. District Court or the Court of Federal Claims. Most taxpayers do not litigate Form 843 denials, but the option exists if the amount at stake justifies the cost.

A Few Common Mistakes Sink Form 843 Claims

- Working from an outdated form. The December 2024 redesign moved the narrative to Line 8 and payment dates to Line 3. Using old line numbers can put your entries in the wrong place. Download Rev. 12-2024 from IRS.gov.

- Using Form 843 to claim an income tax refund. That requires Form 1040-X.

- Skipping the explanation on Line 8. The IRS treats an unsupported claim as a non-claim.

- Filing past the statute of limitations. The general rule is 3 years from the filing date or 2 years from the payment date, whichever is later.

- Mailing to the wrong IRS address. The correct address depends on the tax or notice involved. Check the instructions or the notice you received.

- Forgetting to attach the IRS notice copy. Including it speeds processing.

- Trying to e-file. Form 843 cannot be e-filed for most reasons on the form. The only current exception is a Kwong claim for fully paid penalties or interest, filed by an individual with an IRS Online Account. Attempting to e-file outside that exception means the claim does not exist for IRS purposes.

The Line 8 Narrative Is What Wins or Loses Your Form 843 Claim

Frequently Asked Questions About Form 843

The general rule is 3 years from the date you filed the original return, or 2 years from the date you paid the tax or penalty, whichever is later, under IRC Section 6511. For specific situations, such as the Kwong COVID-era penalty refunds, separate deadlines may apply. Always check the deadline tied to the specific penalty or refund you are claiming.

For most reasons on the form, no. Form 843 must be submitted on paper, and it cannot be e-filed through tax software. As of July 2026, one exception exists: individual taxpayers with an IRS Online Account can e-file a Kwong v. United States claim for fully paid interest and penalties through the new tool on IRS.gov’s Mobile-friendly forms page. Business taxpayers, and individuals who prefer not to e-file, still mail the completed form, with all supporting documents, to the IRS address tied to the underlying tax type or notice.

The IRS redesigned the form. Your reason for filing is now a checkbox block at the top, above your name. Payment dates moved to Line 3, the type of tax moved to Line 4, the type of return moved to Line 5, a new reason checkbox sits at Line 7, and the written explanation is now Line 8. The old “credit” option was removed.

Form 1040-X amends an income tax return to correct income, deductions, credits, or filing status, usually to claim an income tax refund. Form 843 claims refunds of non-income taxes, penalties, interest, and fees, or asks the IRS to abate penalties that have been assessed. They cover different lanes and use different mailing addresses.

No. FBAR civil penalties are assessed under Title 31 (the Bank Secrecy Act), not the Internal Revenue Code. They have a separate process administered by FinCEN, not the IRS. Form 843 covers only IRS-administered penalties under Title 26.

Most claims take 3 to 6 months. Complex or high-dollar claims, or those filed during peak season, can take longer. The IRS does not provide a status portal for Form 843 the way it does for income tax refunds. If you have not heard back within 6 months, you can call the IRS or your local Taxpayer Advocate Service office.

You can file Form 843 on your own, especially for a straightforward first-time abatement request. For reasonable-cause claims, complex penalty disputes, or large-dollar refunds, working with a tax professional improves your odds, because the explanation on Line 8 is the determining factor. A self-prepared filing can also become evidence in any later dispute, so the wording matters.

Yes. Form 843 covers both refunds of penalties already paid and abatement of penalties assessed but not yet paid. If you have already paid, enter your payment date on Line 3 and check the box for the refund-related reason at the top of the form. If the penalty is still outstanding, you are requesting an abatement and leaving Line 3 blank. The supporting facts on Line 8 work the same way for both.

The information in this article is for general informational purposes only and does not constitute tax, legal, or financial advice. IRS rules are complex and change over time, and the right form to file depends on the specific facts of your situation. Consult a qualified tax professional before submitting Form 843 for a high-dollar or complex matter.

Related Resources

- What to Write on Form 843 for a Kwong Penalty Refund

- New Court Ruling Opens Door for COVID-Era Penalty Refunds: Kwong and Form 843

- IRS First-Time Abatement: Who Qualifies for Penalty Relief

- Amending Your U.S. Tax Return with Form 1040-X

- Late Expat Tax Filing: Penalties, Extensions, and Catch-Up Options

- Streamlined Filing Procedures Explained: How U.S. Expats Catch Up Penalty-Free

- Form 1040 for U.S. Expats Explained: Who Must File, How to File, and How to Owe $0

- IRS Form 4868 for Expats: How to Extend Your Tax Deadline

- FBAR Penalties Explained: Non-Willful, Willful, and How to Avoid Them

- U.S. Expat Tax Deadlines for Americans Living Abroad