The IRS COVID Refund Deadline Is July 10, 2026 – Here’s Who Qualifies

The National Taxpayer Advocate estimates that tens of millions of taxpayers, including U.S. citizens living abroad, may be entitled to file a protective refund claim for late-filing penalties, late-payment penalties, and underpayment interest the IRS assessed during the COVID-19 federal disaster period. In Kwong v. United States (Nov. 25, 2025), the U.S. Court of Federal Claims held that IRC Section 7508A(d) automatically postponed every federal tax filing and payment deadline from January 20, 2020, through July 10, 2023. The IRS is appealing the decision, and the issue is unlikely to be finally resolved for years. The IRS is not currently issuing refunds. To preserve your right to one if the IRS ultimately loses, Form 843 must be filed with the IRS by July 10, 2026.

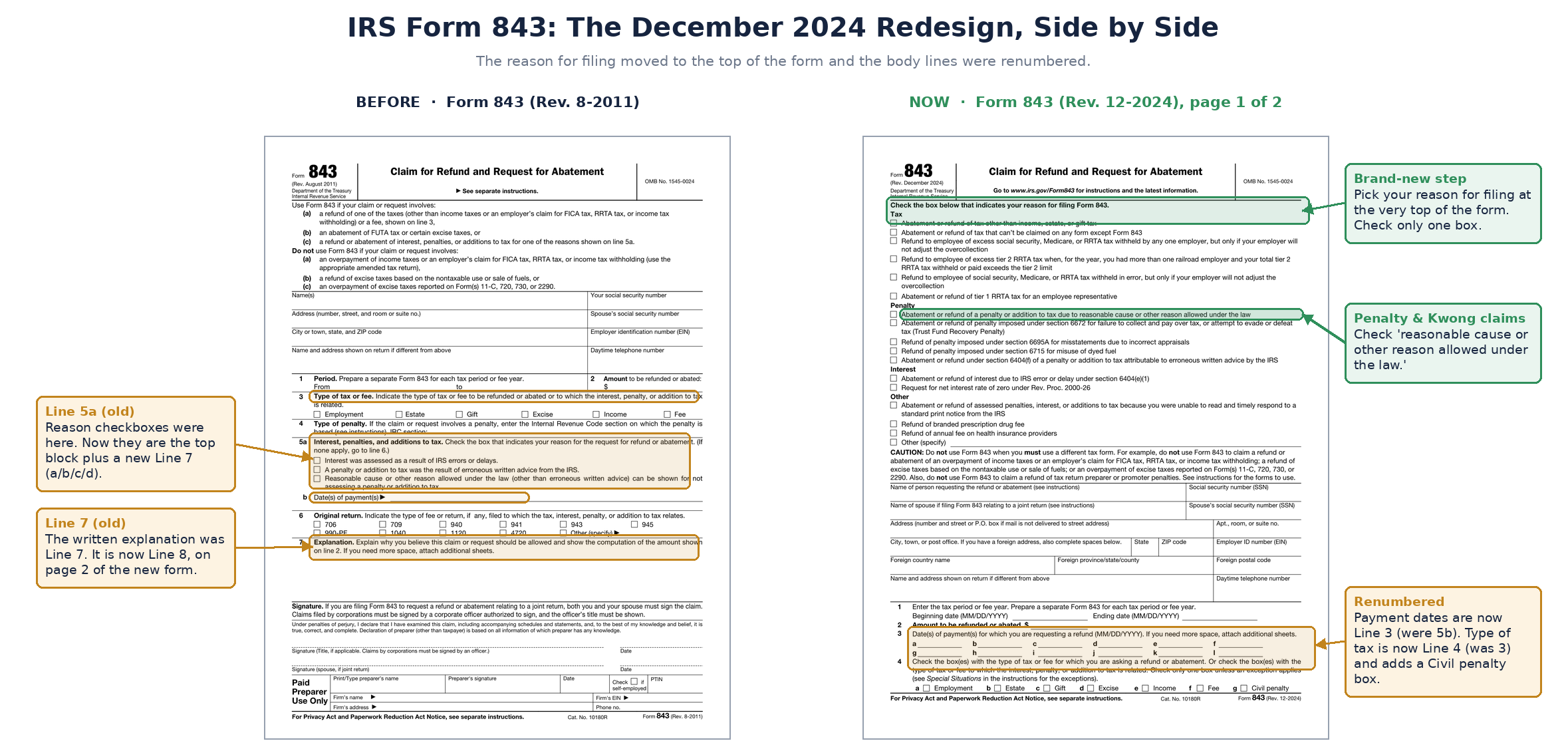

One practical note before you start: the IRS redesigned Form 843 in December 2024, so the current version is Form 843 (Rev. 12-2024). The line numbers and checkboxes differ from those in older copies you may find online. This article points you to the right entries on the current form.

Think a COVID-Era Penalty Applies to You?

Filing has to happen before July 10, so the sooner you have your transcripts, the better.

The Kwong Ruling Reopened COVID-Era Penalties and Interest

The U.S. Court of Federal Claims ruled in Kwong v. United States that IRC Section 7508A(d), the federal disaster postponement statute, mandatorily extended every tax deadline that fell during the COVID-19 federal disaster declaration. The court held that the IRS lacked authority to assess failure-to-file penalties, failure-to-pay penalties, or underpayment interest for obligations due in that period.

The U.S. Tax Court reached the same statutory conclusion in Abdo v. Commissioner, 162 T.C. No. 7 (2024), holding that Section 7508A(d) is mandatory and self-executing. Abdo addressed Tax Court petition filing deadlines; Kwong extends the reasoning to penalties and interest.

How the COVID Disaster Postponement Works

The federal disaster declaration ran from January 20, 2020, through May 11, 2023. Section 7508A(d) extends the postponement an additional 60 days, pushing the effective deadline to July 10, 2023. The three-year statute of limitations on a refund claim, measured from the extended deadline, closes on July 10, 2026.

What the Taxpayer Advocate Is Saying

In April 2026, National Taxpayer Advocate Erin Collins issued a public alert urging affected taxpayers to file refund or abatement claims using Form 843, Claim for Refund and Request for Abatement, by July 10, 2026.

Where the Case Stands Now

The IRS is appealing the decision and has not begun issuing refunds. A protective refund claim filed now is what locks in your right to a refund if the IRS ultimately loses the case. Without a timely filing, the statute of limitations closes, and the refund window is gone, regardless of how the appeal turns out. Form 843 has never been e-fileable, and it still isn’t for most reasons on the form. As of July 2026, the IRS opened a narrow exception: individual taxpayers with an existing IRS Online Account can now file a Kwong-related claim for fully paid interest and penalties electronically. Business taxpayers, and individuals who prefer not to e-file, still submit the form on paper.

A Wide Range of U.S. Taxpayers Should Consider Filing

The ruling affects many U.S. taxpayers, including a large number who live abroad. You should consider filing a protective claim if you fall into one of these situations:

- Anyone who paid a failure-to-file or failure-to-pay penalty on a Form 1040 for tax years 2019 through 2022 that was filed or paid late during the COVID disaster window

- Anyone assessed a failure-to-file penalty on a zero-tax-due return filed during the disaster window. Under the Kwong logic, the return was not technically late until July 10, 2023, so the penalty may be refundable

- Americans abroad who received late-filing penalties because of embassy closures, postal delays, or accountant unavailability between 2020 and 2023

- Self-employed expats who paid underpayment interest on quarterly estimated tax shortfalls during the disaster period

- Streamlined filers who paid late-filing or late-payment penalties on income tax owed alongside their compliance submission, separate from any miscellaneous offshore penalty

- Owners of U.S.-based small businesses operated from overseas assessed pandemic-era failure-to-file or failure-to-pay penalties

- Retirees abroad who paid late-payment interest on tax owed for 2019 through 2022 returns

- Expats who received late-filing penalties on international information returns (Form 5471, Form 3520, or Form 8938) for filings due between January 20, 2020, and July 10, 2023. The NTA’s May 2026 guidance states these filers may qualify for refunds under the same disaster postponement logic.

Penalties on FBAR (FinCEN Form 114) rest on Title 31 authority and are outside the Kwong ruling. For Form 5471, Form 3520, and Form 8938, the guidance indicates these late filers may qualify, but the analysis is more complex than for income tax penalties and requires a professional review before you file.

What the Ruling Means for Americans Abroad

1. No money is moving right now

The IRS is appealing the Kwong decision and has not begun issuing refunds. The case is likely to take years to fully resolve through the appellate courts, and the final outcome is not certain. What you can do today is preserve a place in line, in case the IRS ultimately loses.

2. File the claim as a protective claim by July 10, 2026

For paper filings, write “Kwong vs. United States” across the top of Form 843 so the IRS routes it correctly, and add one sentence on Line 8 stating the filing is a protective claim under Treas. Reg. § 301.6402-2(b)(1). That combination is what signals to the IRS that you are filing to preserve your rights pending the appeal, and it stops the three-year statute of limitations from closing your window before the case is finally decided. Miss the July 10 deadline, and your claim is gone, regardless of how the appeal turns out.

3. Your current filing obligations have not changed

Tax year 2025 returns, FBAR, and information return obligations remain in full effect. The Kwong ruling addresses penalties and interest already assessed during the historical disaster window. It is not a holiday for present-year compliance.

4. International information return penalties are a separate question

If you paid penalties on Form 5471, Form 3520, or Form 8938 for filings due between January 20, 2020, and July 10, 2023, the NTA’s May 2026 guidance states you may qualify for a refund under the same disaster postponement logic. This analysis is more complex than for standard income tax penalties, and you should have a qualified international tax professional review your file before filing. The July 10, 2026, deadline applies equally, so do not assume you are out of scope without checking.

FBAR penalties (FinCEN Form 114) rest on Title 31 authority, which is outside the scope of Section 7508A(d), and are not covered by the Kwong ruling.

Your Next Steps Before the July 10 Deadline

The mechanics of the filing are simple. The path you take depends on which penalties you paid and where you stand with the IRS.

1. Start With Your IRS Account Transcripts

Request transcripts for tax years 2019 through 2022 before doing anything else. They list every penalty and interest assessment by date and amount, and they are the cleanest way to identify what may be refundable. Use the IRS account transcript walkthrough if you are pulling them from overseas.

Once you have your transcripts, the NTA’s Part II guidance recommends three steps to identify what may be refundable:

- Look for penalty or interest entries: these include failure-to-file, failure-to-pay, and estimated tax penalties.

- Note the dates on those entries.

- Check whether those dates fall on or before July 10, 2023, and no earlier than January 20, 2020. (The Taxpayer Advocate phrases this as “before July 11, 2023,” which is the same cutoff.) If they do, the penalties may have been incorrectly assessed under the COVID-19 disaster postponement and could be eligible for a refund.

You do not need to decode every line on your transcript. If you want more details on IRS transaction codes, IRS Document 6209 (ADP and IDRS Information Reference Guide) explains each code. Use the version that matches the tax year you are reviewing.

2. File Form 843 Correctly on the Current (Rev. 12-2024) Form

If you paid a failure-to-file or failure-to-pay penalty on a 2019, 2020, 2021, or 2022 Form 1040, a few details matter. The IRS redesigned Form 843 in December 2024, so make sure you are working from the current version.

- Decide between e-filing and paper. As of July 2026, individual taxpayers with an existing IRS Online Account can file a Kwong claim for fully paid interest and penalties electronically via the new tool on the IRS.gov Mobile-friendly forms page. On the “Why You’re Here” screen, choose “Protective claim based on mandatory COVID-19 disaster tax relief and/or Kwong v. United States.” On the “Reason For Filing” screen that follows, choose “Refund of assessed penalties and interest based on pending litigation.” Both selections are required; selecting one does not automatically select the other. Business taxpayers, and anyone who prefers not to e-file, can mail the paper form instead.

- If filing on paper, use the right header language. Write “Kwong vs. United States” across the top of the form, above the reason checkboxes, so the IRS routes the claim correctly. Add one sentence on Line 8 stating the filing is a protective claim under Treas. Reg. § 301.6402-2(b)(1).

- Check the penalty reason box at the top of the form. On Rev. 12-2024, your reason for filing is a checkbox block above your name. Check “Abatement or refund of a penalty or addition to tax due to reasonable cause or other reason allowed under the law,” then check box c on Line 7.

- Enter the penalty amount on Line 2 and your payment date on Line 3. A protective claim does not require an exact dollar figure, so if the refundable amount may change depending on how the appeal resolves, you can enter the specific amount you paid or write “In excess of $10.00” on Line 2 to claim the full penalty assessed. Entering your payment date on Line 3 is what marks the claim as a refund.

- Put your explanation on Line 8. The written narrative tying the penalty to the Kwong ruling now goes on Line 8 of the redesigned form. Our Line 8 walkthrough shows exactly what to write.

- If mailing, send it Certified Mail with Return Receipt Requested to Internal Revenue Service, 1973 N Rulon White Blvd., Ogden, UT 84201. This gives you documented proof of timely filing. From overseas, use a trackable international service. The deadline is July 10, 2026.

- File a separate Form 843 for each tax year. Even if the same penalty was assessed across multiple years, a 2020 claim and a 2021 claim are two filings, not one. Mail them together if you like, but they should be separate forms.

3. Address Special Situations Before You File

- If you still owe back taxes from those years, bring those returns up to date first. The Streamlined Filing Procedures and back tax catch-up paths are designed for U.S. taxpayers abroad who fell behind during this period.

- If you paid penalties under Form 5471, Form 3520, or Form 8938 during the January 20, 2020, to July 10, 2023, window, the NTA’s guidance says you may qualify for a refund.

- If you paid FBAR penalties, those fall under Title 31 authority and are outside the scope of the Kwong ruling.

- If the IRS has already opened an examination of those years, stop and have a qualified international tax professional review your file before submitting Form 843. The interaction between an open exam and a protective refund claim requires careful sequencing.

A specialist who handles these claims for U.S. taxpayers abroad can review the transcripts you provide, confirm which penalties fall in the window, and prepare Form 843 with the correct protective language well before the July 10 deadline.

Think You Qualify? File a Protective Refund Claim Before July 10.

The Kwong Logic Opens Three More Refund Possibilities

The Kwong reasoning extends beyond the most common penalty refunds. Three additional opportunities are worth flagging before the July 10 deadline.

1. Failure-to-File Penalties on Zero-Tax-Due Returns

If the IRS assessed a failure-to-file penalty on a return that showed no tax owed, the penalty may be refundable under the Kwong logic. The argument: the return was not technically late until July 10, 2023, because Section 7508A(d) postponed the original due date.

2. Refund Windows You Thought Had Closed

The same statute that postponed filing deadlines may have suspended the three-year window for claiming refunds. If your refund window for a 2019 or 2020 return appeared to expire during the disaster declaration, the postponement may have kept it open. Refund claims that taxpayers believed were lost may still be alive. This is a more complex argument, but the possibility is real.

3. Additional Overpayment Interest From the IRS

When the IRS holds onto a refund longer than it should, it owes the taxpayer interest on the delay. Some practitioners argue that under the Kwong reasoning, the IRS may owe additional overpayment interest for delay periods affected by the postponement. The answer depends on how the appeal plays out and how the IRS interprets the postponement on the back end. Worth flagging if you had a sizable refund that was significantly delayed during the disaster window.

If any of these apply to you, treat them as part of the same protective filing window. The July 10, 2026, deadline applies to these arguments, too.

Frequently Asked Questions about the Kwong Ruling

Form 843, Claim for Refund and Request for Abatement, is the IRS form used to request a refund or abatement of certain penalties, interest, and additions to tax. In the context of the Kwong ruling, it is the form used to claim refunds of failure-to-file and failure-to-pay penalties, as well as underpayment interest assessed during the COVID-19 disaster period.

If you would like us to prepare and certified-mail it for you, the fee is $250 per form, and a separate Form 843 is required for each tax year you are claiming. Claiming penalties across 2020, 2021, and 2022, for example, means three forms. The fee covers preparing the form on the current Rev. 12-2024 layout, adding the protective-claim language where it applies, and handling the certified mailing so you have proof of timely filing.

Yes. The IRS redesigned Form 843 in December 2024. On the current version (Rev. 12-2024), your reason for filing is a checkbox block at the top of the form, the amount goes on Line 2, payment dates go on Line 3, and the written explanation goes on Line 8. Download the current form directly from IRS.gov so your entries land in the right place.

Any taxpayer who paid a failure-to-file penalty, failure-to-pay penalty, or underpayment interest on a federal tax obligation due between January 20, 2020, and July 10, 2023, could qualify if the Kwong decision survives the IRS’s appeal. The court’s reasoning rests on IRC Section 7508A(d), which postponed all federal tax deadlines during the COVID-19 federal disaster declaration. Tens of millions of taxpayers, including U.S. citizens living abroad, fall within this window. None of them have received refunds yet.

No. The IRS is appealing the Kwong decision and has not yet begun issuing refunds based on it. The case is expected to take years to fully resolve, and the IRS may ultimately prevail. Filing Form 843 now does not produce a refund check today. It preserves your right to one if the IRS loses.

Because the IRS is appealing the Kwong decision, you file Form 843 to preserve your right to a refund. For paper filings, the IRS asks you to write “Kwong vs. United States” across the top so the claim is routed correctly, and to note on Line 8 that the filing is a protective claim under Treas. Reg. Section 301.6402-2(b)(1). That combination locks in your filing date and stops the three-year statute of limitations from closing your window before the case is finally decided.

For most reasons on the form, no, Form 843 must be filed on paper. As of July 2026, the IRS has opened one narrow exception: individual taxpayers with an existing IRS Online Account can file a Kwong-related claim for fully paid interest and penalties electronically through the new tool on the IRS.gov Mobile-friendly forms page. Business taxpayers and individuals who prefer not to e-file still submit on paper. If you mail it, the National Taxpayer Advocate recommends sending it certified mail, return receipt requested, so you have proof of the filing date if the claim is misplaced.

Request your IRS account transcripts for tax years 2019 through 2022. The transcripts list every penalty and interest assessment by date and amount, which is the clearest way to identify what may be refundable.

For Form 5471, Form 3520, and Form 8938: possibly yes. The NTA’s May 2026 guidance states that late filers of international information returns penalized during the January 20, 2020, to July 10, 2023, disaster window may qualify for refunds under the same §7508A(d) postponement logic. The analysis is more complex than for income tax penalties and requires professional review. If you paid these penalties during that window, the July 10, 2026, deadline applies, and you should not rule out filing a protective claim without consulting a specialist.

You generally lose your right to claim a refund of penalties or interest assessed during the COVID-19 disaster period. The three-year window measured from the extended July 10, 2023, deadline closes on July 10, 2026, and once it closes, the statute of limitations on the refund claim is gone, even if the IRS later loses the Kwong appeal and the underlying legal position is finally accepted.

No. The National Taxpayer Advocate has explicitly stated that this relief is not automatic. The IRS will not adjust your account on its own, and the IRS is currently appealing the Kwong decision. You must file Form 843 by July 10, 2026, to preserve a claim that may pay out only if the IRS ultimately loses on appeal.

Yes. If you have an existing IRS Online Account, you can now file a Kwong claim for fully paid penalties and interest electronically, which avoids international mail entirely. If you file on paper, Form 843 can be mailed to the IRS from any country. The mailing address depends on the type of tax and penalty involved; for Kwong claims, mail to Internal Revenue Service, 1973 N Rulon White Blvd., Ogden, UT 84201. From overseas, allow extra time for international postal delivery and use a trackable, certified, or international-tracked service to ensure a verifiable filing date.

No. File a separate Form 843 for each tax year. Even if the same penalty type was assessed across multiple years, each year is its own claim. Mail them together if you like, but they should be separate forms.

Possibly. When the IRS holds onto a taxpayer’s refund longer than the law allows, it must pay overpayment interest for the delay. Some practitioners argue that under the Kwong reasoning, the IRS may owe additional overpayment interest for delay periods affected by the COVID-19 postponement. This is a more complex technical argument, and the answer will depend on how the appeal plays out and how the IRS interprets the postponement on the back end. If you had a sizable refund that was significantly delayed during the disaster window, raise it with a qualified tax professional before filing.

The information in this article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules are complex and change frequently. Consult a qualified tax professional regarding your specific situation before taking any action.

Related Resources

- Form 843 Explained: How to Claim a Refund or Penalty Abatement

- What to Write on Line 8 Form 843 for a Kwong Penalty Refund

- How to Get Your IRS Account Transcript From Abroad

- Streamlined Filing Procedures Explained: How U.S. Expats Catch Up Penalty-Free

- Back Taxes for U.S. Expats: How to Catch Up With the IRS

- IRS First-Time Abatement: Who Qualifies for Penalty Relief