Form 8949 for U.S. Expats Explained: Reporting Capital Gains and Losses

- What Is Form 8949?

- When Do I Need to File Form 8949?

- What Changed for 2025 (Filed in 2026)?

- What Is the Difference Between Short-Term and Long-Term Capital Gains?

- How Do I Complete Form 8949 Step by Step?

- What If I Sold Foreign Property?

- How Can I Avoid Double Taxation on Foreign Investment Gains?

- Do I Report Cryptocurrency on Form 8949?

- What Is the Difference Between Form 8949 and FBAR?

- What Mistakes Should I Avoid on Form 8949?

- Frequently Asked Questions

- Get Expert Help With Form 8949

- Related Resources

You need to file Form 8949 whenever you sell, trade, or dispose of a capital asset and realize a gain or loss. This applies to all U.S. citizens and green card holders regardless of where you live, and includes sales of foreign stocks, foreign property, cryptocurrency, and any other investment.

Form 8949 is the detailed transaction log where you list every individual sale. The totals then flow to Schedule D, where your net capital gain or loss is calculated and added to your Form 1040.

For the 2025 tax year, two important changes affect how you complete Form 8949:

- New digital asset boxes (G, H, I, J, K, L): Crypto and digital asset transactions now have their own checkbox categories on Form 8949, separate from traditional securities. Do not use the old Boxes C or F for digital assets.

- Form 1099-DA: Custodial brokers must now report gross proceeds from digital asset sales to the IRS. You must reconcile your Form 8949 entries with any Form 1099-DA you receive.

- Wash sale rule now covers digital assets: Under the One Big Beautiful Bill Act (OBBB), crypto wash sales are disallowed starting in 2025.

The good news for expats: if you paid foreign taxes on your capital gains, the Foreign Tax Credit can offset or eliminate your U.S. tax on those same gains, so you do not pay twice.

Do I Need to File Form 8949 as a U.S. Expat?

Here is how to complete Form 8949 correctly, what the new rules mean for expats, and how to avoid the most common mistakes.

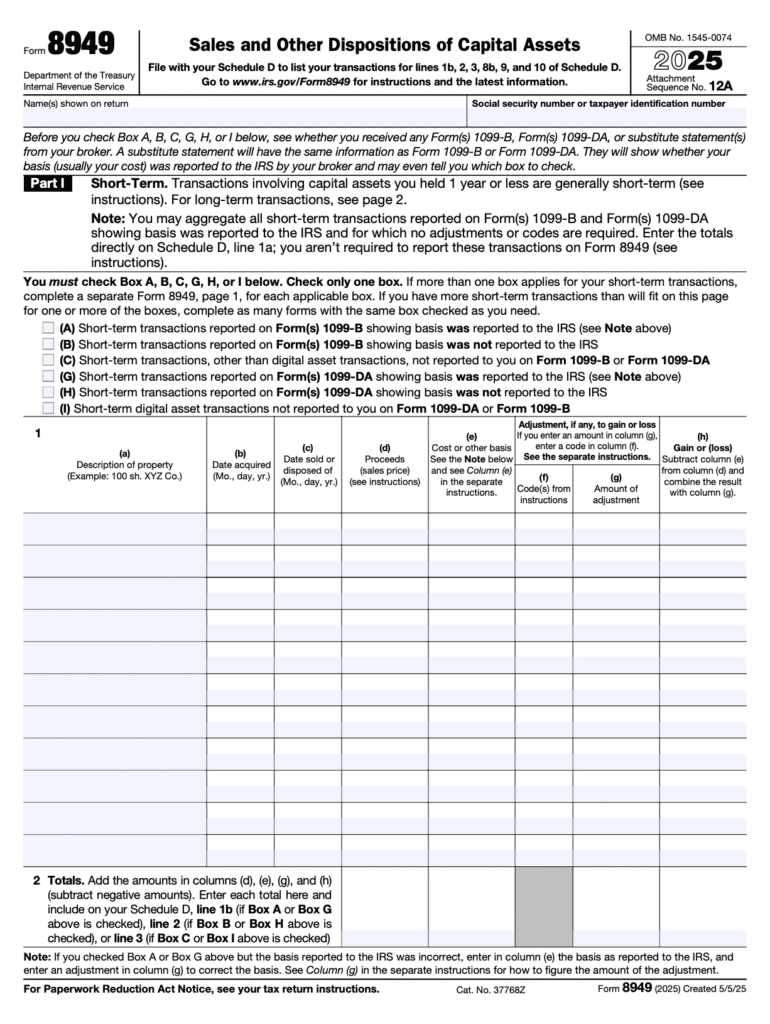

What Is Form 8949?

Form 8949 (Sales and Other Dispositions of Capital Assets) is the IRS form where you report every individual sale of stocks, bonds, real estate, cryptocurrency, and other investments. It reconciles amounts reported to you (and to the IRS) on Form 1099-B, Form 1099-DA, or Form 1099-S with the amounts you report on your return.

The form has two parts:

- Part I reports short-term transactions (assets held one year or less)

- Part II reports long-term transactions (assets held more than one year)

For each transaction, you list the description of the property sold, the date acquired, and date sold, sales proceeds, cost basis (what you originally paid), and the resulting gain or loss. The totals from Form 8949 then carry over to Schedule D, where your overall capital gain or loss is calculated.

When Do I Need to File Form 8949?

You must file Form 8949 whenever you sell or exchange a capital asset and realize a gain or loss. Common scenarios for expats include:

- Selling shares in a foreign company through a non-U.S. brokerage

- Trading or selling cryptocurrency (including crypto-to-crypto swaps)

- Selling foreign rental property or vacation homes

- Selling foreign mutual funds or ETFs (which may also trigger PFIC reporting)

- Trading stocks through a U.S. brokerage while living abroad

- Selling inherited property located outside the U.S.

Even if you did not receive a Form 1099-B or Form 1099-DA (common with foreign brokers), you must still report every sale on Form 8949. The absence of a broker reporting form does not eliminate your reporting obligation.

What Changed for 2025 (Filed in 2026)?

New Digital Asset Checkbox Categories

For the 2025 tax year, Form 8949 has six new checkbox categories specifically for digital asset transactions reported on Form 1099-DA:

| Box | Description | Holding Period |

|---|---|---|

| G | Short-term digital asset transactions, basis reported to IRS | Short-term |

| H | Short-term digital asset transactions, basis not reported to IRS | Short-term |

| I | Short-term digital asset transactions, not reported on Form 1099-DA | Short-term |

| J | Long-term digital asset transactions, basis reported to IRS | Long-term |

| K | Long-term digital asset transactions, basis not reported to IRS | Long-term |

| L | Long-term digital asset transactions, not reported on Form 1099-DA | Long-term |

Do not use Boxes C or F for digital asset transactions. Box C is now reserved for short-term transactions of non-digital assets not reported on Form 1099-B or 1099-DA. Box F applies to long-term non-digital assets.

For most expats using foreign crypto exchanges that do not issue Form 1099-DA, you will check Box I (short-term) or Box L (long-term).

Form 1099-DA Integration

Starting with 2025 transactions, custodial brokers must report gross proceeds from digital asset sales to the IRS on Form 1099-DA. For 2025, brokers report gross proceeds only (not cost basis). Beginning in 2026, brokers must also report cost basis for “covered” digital assets.

What this means for you: the IRS will match your Form 8949 against the broker’s Form 1099-DA. Discrepancies will trigger automated notices. Always report proceeds exactly as shown on the 1099-DA, and use columns (f) and (g) on Form 8949 to make any necessary adjustments.

Wash Sale Rule Now Applies to Digital Assets

Under the OBBB, the wash sale rule now applies to digital assets starting in 2025. If you sell crypto at a loss and buy the same or substantially identical asset within 30 days (before or after the sale), the loss is disallowed. Report the disallowed loss on Form 8949 using adjustment code “W” in column (f).

Wallet-by-Wallet Basis Tracking

As of January 1, 2025, you must track your cost basis on a wallet-by-wallet and account-by-account basis. You can no longer use a “universal” approach that pools cost basis across multiple exchanges and wallets.

What Is the Difference Between Short-Term and Long-Term Capital Gains?

The length of time you hold an asset determines your tax rate:

| Holding Period | Classification | Tax Rate |

|---|---|---|

| One year or less | Short-term | Ordinary income rates (10% to 37%) |

| More than one year | Long-term | Preferential rates: 0%, 15%, or 20% |

2025 Long-Term Capital Gains Brackets

| Tax Rate | Single | Married Filing Jointly |

|---|---|---|

| 0% | Up to $47,025 | Up to $96,700 |

| 15% | $47,026 to $518,900 | $96,701 to $600,050 |

| 20% | Above $518,900 | Above $600,050 |

Expat tip: Capital gains are unearned income. The Foreign Earned Income Exclusion (FEIE) does not apply to capital gains. If you paid foreign capital gains tax, use the Foreign Tax Credit (FTC) on Form 1116 to offset your U.S. tax liability dollar-for-dollar.

How Do I Complete Form 8949 Step by Step?

Step 1: Gather Your Transaction Records

Collect all documentation for investment sales during the tax year: Form 1099-B from U.S. brokers (if applicable), Form 1099-DA from digital asset brokers, foreign broker statements showing buy and sell transactions, real estate closing statements, and records of purchase dates, amounts, and improvement costs.

Step 2: Categorize Your Transactions

Separate transactions into the appropriate checkbox categories based on holding period (short-term or long-term), asset type (traditional securities or digital assets), and whether the basis was reported to the IRS.

For most expats using foreign brokers that do not report to the IRS, you will use Box C or Box F for traditional securities, and Box I or Box L for digital assets.

Step 3: Complete Each Column

For each transaction, enter the description in column (a) (such as “100 shares XYZ Corp” or “0.5 BTC”), the date acquired in column (b), the date sold in column (c), sales proceeds in USD in column (d), cost basis in USD in column (e), any adjustment codes in column (f), the adjustment amount in column (g), and the gain or loss in column (h).

Step 4: Handle Currency Conversions

Convert all foreign currency amounts to U.S. dollars using the exchange rate on the transaction date. The U.S. Treasury publishes historical exchange rates. Use the purchase date rate for cost basis and the sale date rate for proceeds.

Document every exchange rate used. The IRS may request this documentation during an audit. Create a spreadsheet to track each transaction, including dates, foreign-currency amounts, exchange rates, and USD equivalents.

Step 5: Apply Adjustment Codes (If Needed)

Common adjustment codes for expats:

- Code B: Incorrect cost basis on Form 1099-B or 1099-DA

- Code W: Wash sale loss disallowed

- Code H: Exclusion of gain from sale of primary residence (Section 121)

- Code E: Selling expenses not reflected on Form 1099-B or 1099-S

Step 6: Transfer Totals to Schedule D

Add up all gains and losses on each Form 8949 page, then transfer these totals to the corresponding lines on Schedule D. The net result from Schedule D flows to your Form 1040.

What If I Sold Foreign Property?

When you sell foreign property, report the capital gain or loss on Form 8949 and Schedule D. The calculation follows the same structure as other investments:

- Determine your cost basis (original purchase price in USD on the purchase date, plus improvement costs)

- Calculate the gain or loss (sale price in USD on the sale date, minus cost basis and selling expenses)

- Determine if the gain is short-term or long-term based on the ownership period

Additional considerations for foreign real estate:

- Primary residence exclusion: If the property was your primary residence and you meet the IRS requirements (lived in it two of the last five years), you may exclude up to $250,000 of gain ($500,000 married filing jointly)

- Rental property depreciation: Rental properties require depreciation recapture calculations using the Alternative Depreciation System (30 years for foreign residential property)

- FBAR and FATCA: If you deposit sale proceeds into a foreign bank account, you may need to file an FBAR if your total foreign accounts exceed $10,000, and Form 8938 if you exceed FATCA thresholds

How Can I Avoid Double Taxation on Foreign Investment Gains?

The Foreign Tax Credit (FTC) prevents double taxation on capital gains. If you paid capital gains tax to a foreign country, you can claim a dollar-for-dollar credit against your U.S. tax liability using Form 1116.

Example: James, an American expat living in the UK, sold shares in a British company for a $10,000 long-term capital gain. He paid approximately $2,400 in UK capital gains tax.

- His Form 8949 reports the $10,000 gain

- His U.S. tax at the 15% long-term rate would be $1,500

- He claims a Foreign Tax Credit of $1,500 on Form 1116

- Result: $0 additional U.S. tax because the UK tax paid ($2,400) exceeds his U.S. liability ($1,500)

The FTC ensures you are never taxed twice on the same investment income. However, you must file Form 1116 to claim the credit. For a full comparison of the FTC and FEIE, see FEIE vs. Foreign Tax Credit.

Do I Report Cryptocurrency on Form 8949?

Yes. The IRS treats cryptocurrency as property, meaning every disposition is a capital gain or loss event that requires Form 8949 reporting.

You must report selling crypto for fiat currency, exchanging one crypto for another, and using crypto to purchase goods or services. Each transaction requires the date acquired, the date sold, the cost basis in USD, the fair market value in USD at disposal, and the resulting gain or loss.

For 2025, use the new digital asset boxes (G, H, I for short-term; J, K, L for long-term) instead of the traditional boxes. If you use a foreign exchange that does not issue Form 1099-DA, check Box I or Box L and maintain your own records.

For a complete guide to crypto taxes for expats, including FBAR/FATCA implications and the wash sale rule, see our cryptocurrency tax guide.

What Is the Difference Between Form 8949 and FBAR?

Form 8949 and the FBAR serve completely different purposes:

| Feature | Form 8949 | FBAR (FinCEN Form 114) |

|---|---|---|

| Purpose | Reports capital gains and losses from selling investments | Reports foreign financial account balances |

| Filed with | IRS (attached to your tax return) | FinCEN (filed separately from your tax return) |

| Determines taxes owed? | Yes | No (informational only) |

| Threshold | Any capital gain or loss | Foreign accounts exceeding $10,000 aggregate |

| Deadline | April 15 (June 15 for expats) | April 15 (automatic extension to October 15) |

You may need both forms if you sold investments held in foreign brokerage accounts (Form 8949) and have foreign accounts totaling over $10,000 (FBAR). If your foreign financial assets exceed FATCA thresholds, you may also need Form 8938. See our FBAR vs. FATCA comparison for details on when each applies.

What Mistakes Should I Avoid on Form 8949?

- Failing to report foreign transactions: Just because a foreign broker did not send you a 1099-B does not mean you can skip reporting. The IRS requires reporting of all worldwide capital gain and loss transactions.

- Incorrect currency conversions: Always use the exchange rate on the transaction date, not year-end rates or approximations. Document every rate used.

- Using the wrong boxes for digital assets. For 2025, crypto transactions must use the new Boxes G through L, not the traditional Boxes A through F.

- Missing the wash sale rule on crypto: As of 2025, if you sell crypto at a loss and repurchase the same asset within 30 days, the loss is disallowed. Use adjustment code “W” on Form 8949.

- Not claiming the Foreign Tax Credit: If you paid foreign capital gains tax, claim the FTC on Form 1116 to avoid double taxation.

- Mixing up short-term and long-term: Assets held exactly one year are short-term. Assets held one year or more are long-term. One day can change your tax rate from 37% to 15%.

- Forgetting the cost basis step-up on inherited property: When you inherit property, your cost basis is stepped up to the fair market value on the date of death, which can significantly reduce your gain.

- Omitting crypto-to-crypto trades: Every swap between cryptocurrencies is a taxable event. This is one of the most commonly missed transactions.

Frequently Asked Questions

Yes. You must report all capital gain and loss transactions on Form 8949 regardless of whether you received a 1099-B or 1099-DA. Foreign brokers typically do not report to the IRS, which means you are responsible for tracking and reporting every transaction. Use Box C or F (for traditional securities) or Box I or L (for digital assets) to indicate these were not reported on a broker form.

No. The Foreign Earned Income Exclusion applies only to earned income (wages, salaries, self-employment income). Capital gains are unearned income and cannot be excluded using the FEIE. Use the Foreign Tax Credit instead if you paid foreign taxes on the gains.

Use the exchange rate on the date of each transaction. For the purchase, use the rate on the date you acquired the asset (this determines your cost basis in USD). For the sale, use the rate on the date you sold the asset (this determines your proceeds in USD). The U.S. Treasury publishes historical exchange rates you can reference.

For 2025, Form 8949 has six new checkbox categories: Boxes G, H, and I for short-term digital asset transactions, and Boxes J, K, and L for long-term digital asset transactions. These correspond to whether the basis was reported to the IRS on Form 1099-DA (G/J), was not reported (H/K), or the transaction was not reported on any broker form (I/L).

Yes. Every exchange of one cryptocurrency for another (such as trading Bitcoin for Ethereum) is a taxable event. You must calculate the gain or loss based on the fair market value of the crypto received versus your cost basis in the crypto you sold. Report each swap as a separate transaction on Form 8949.

Yes. Report the sale on Form 8949 and Schedule D. If the home was your primary residence and you lived in it for at least two of the past five years, you may exclude up to $250,000 of gain ($500,000 married filing jointly) using the Section 121 exclusion. Use adjustment code “H” in column (f). See our guide on capital gains tax on foreign property for details.

Yes. If your total capital losses exceed your total capital gains for the year, you can deduct up to $3,000 of net capital loss against ordinary income ($1,500 if married filing separately). Any remaining losses are carried forward indefinitely to future years. This calculation is done on Schedule D, not on Form 8949 itself.

You can file an amended return (Form 1040-X) to correct errors. Common reasons expats amend include unreported foreign investment sales, incorrect currency conversions, missed Foreign Tax Credits, and miscalculated cost basis. If you have multiple years of unfiled or incorrect returns, our Streamlined Filing Compliance Services may help you catch up without penalties.

Get Expert Help With Form 8949

Form 8949 can become complex quickly when you are dealing with foreign brokers, multiple currencies, digital assets, and potential tax credits. Many of our expat clients at Greenback come to us after attempting to file on their own and realizing they are over their heads.

If you are ready to be matched with a Greenback accountant, get started here. For general questions about expat taxes or working with Greenback, contact our Customer Champions.

Make Sure Your Investment Sales Are Reported Correctly

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently, and individual circumstances vary. Always consult with a qualified tax professional about your specific situation.

Related Resources

- Schedule D (Form 1040) for Expats

- Foreign Tax Credit Guide

- Form 1116: How to Claim the Foreign Tax Credit

- Cryptocurrency Taxes for U.S. Expats

- Capital Gains Tax on Foreign Property

- Capital Gains Tax on Inherited Property

- FEIE vs. Foreign Tax Credit

- FBAR Filing Requirements

- FBAR vs. FATCA Comparison

- Form 8621: PFIC Reporting