GILTI and Form 8992 Explained: Tax Rules for Expat Business Owners With Foreign Corporations

- What is GILTI Tax?

- How Do GILTI Tax Rates Work?

- Am I Subject to GILTI Tax?

- What Are My GILTI Strategy Options?

- When Should I Consider Disregarded Entity Status?

- How Is GILTI Calculated? A Step-by-Step Example

- What Forms Do I Need to File for GILTI?

- How Does the GILTI High Tax Exception Work?

- Should I Use GILTI Elections or Foreign Tax Credit Strategies?

- What Should I Know About Upcoming GILTI Changes?

- What Common GILTI Mistakes Should I Avoid?

- What Are My Next Steps?

- Related Resources

GILTI (Global Intangible Low-Taxed Income) is a U.S. tax on certain foreign corporation profits that applies to any U.S. shareholder who owns at least 10% of a controlled foreign corporation (CFC). For the 2025 tax year, GILTI is taxed at an effective rate of 10.5% for C corporations (with a 50% deduction under IRC Section 250) and at ordinary income rates for individuals. GILTI is reported on Form 8992 and flows through to your Form 1040 or corporate return.

Starting January 1, 2026, the One Big Beautiful Bill Act replaces GILTI with the Net CFC Tested Income (NCTI) regime, which increases the effective corporate rate to 12.6% and eliminates the prior QBAI (Qualified Business Asset Investment) exclusion that allowed businesses to shelter income based on tangible asset values. For the 2025 return you’re filing now, the prior GILTI rules still apply.

The good news for most American expat business owners: the High Tax Exception can eliminate GILTI entirely if your foreign corporation pays a local tax rate of at least 18.9% (2025) or approximately 14% (2026 under NCTI). Many expats working in countries such as the UK, Germany, France, Japan, and Australia already exceed this threshold. Here’s how GILTI works, who it affects, and how to minimize the impact.

What is GILTI Tax?

GILTI stands for “Global Intangible Low-Taxed Income,” but don’t let the complex name worry you. Starting next year, it will be renamed “Net CFC Tested Income” to better reflect what it covers.

Here’s what GILTI means for your situation: If you own at least 10% of a foreign corporation, the IRS taxes you annually on the corporation’s income, whether or not you receive dividends. This prevents U.S. shareholders from deferring taxes indefinitely on foreign business profits.

What income counts as GILTI?

Almost everything your foreign corporation earns, except:

- Subpart F income (taxed under different rules)

- Income is already highly taxed abroad (through the high tax exception)

- Income connected to U.S. business operations

- Certain oil and gas extraction income

Good news: The same 10% ownership threshold that triggers GILTI also requires Form 5471 filing, so if you’re already filing this form, you’re likely aware of your obligations.

See If GILTI Applies to Your Business

How Do GILTI Tax Rates Work?

Current Tax Year (Filed in 2026):

- Corporate GILTI rate: 10.5% effective rate

- Individual rate: Your regular income tax rate (10%-37%)

- Foreign tax credit: Up to 80% of foreign taxes paid

- Threshold to eliminate U.S. tax: Approximately 13.125% foreign tax rate

Starting Next Year:

The One Big Beautiful Bill permanently changes GILTI by reducing the Section 250 deduction from 50% to 40%, increasing the effective rate to 12.6%. The foreign tax credit improves from 80% to 90%, meaning you need foreign taxes of at least 14% to offset the U.S. GILTI tax completely.

Additionally, the 10% qualified business asset investment (QBAI) deduction is eliminated, so GILTI will apply to all returns, including those from tangible assets.

Am I Subject to GILTI Tax?

You’re subject to GILTI if you’re a U.S. person (citizen or resident) owning at least 10% of a controlled foreign corporation (CFC). This applies regardless of where you live—your U.S. tax status matters, not your residence location.

Important: The same ownership threshold that requires Form 5471 filing also triggers GILTI obligations, so most affected taxpayers already know they have reporting requirements for their foreign businesses.

What Are My GILTI Strategy Options?

Should I Choose Individual Taxation?

This is the default treatment where your CFC’s GILTI gets taxed at your regular income tax rates.

- When this works well: If your foreign corporation pays minimal taxes and you’re in a lower U.S. tax bracket

- When to avoid: If you’re in high tax brackets or your foreign corporation pays significant taxes

- Example: Sarah owns a UK consulting company generating $100,000 in profit. In the 24% tax bracket, she pays $24,000 in U.S. tax on GILTI, even though the UK corporation already paid corporate taxes.

Is the Section 962 Election Right for Me?

The Section 962 election lets you be taxed at the corporate rate (21%) instead of the individual rate, often providing substantial savings.

Key benefits:

- Lower effective tax rate (10.5% currently, 12.6% starting next year)

- Can claim foreign tax credit for up to 80% of foreign corporate taxes (90% starting next year)

- Often eliminates U.S. tax entirely in higher-tax countries

Trade-off: Future dividends are taxable as regular income, not previously taxed income

Example: Mark owns a German corporation paying 26% corporate tax. With a Section 962 election, the foreign tax completely eliminates his U.S. GILTI tax since it exceeds the required threshold.

When Should I Consider Disregarded Entity Status?

Available only for single-owner CFCs, this treats your corporation as a sole proprietorship for U.S. tax purposes using Form 8832.

- Primary benefit: Can use the Foreign Earned Income Exclusion to exclude up to $130,000 (current tax year) or $132,900 (next tax year) and avoid GILTI entirely

- Downside: Subject to 15.3% self-employment tax unless protected by a totalization agreement

- Example: John’s Irish company earns $80,000. With disregarded-entity status, he excludes the full amount under the Foreign Earned Income Exclusion and owes $0 in U.S. income tax.

Should I Form a U.S. Corporation Structure?

Creating a U.S. C-corporation to hold foreign shares works well for larger operations.

- Advantages: Lowest GILTI rate with Section 250 deduction and maximum foreign tax credit benefits

- Disadvantages: Multiple taxation layers and higher compliance costs

- Best for: Larger businesses with substantial revenue and complex operations

How Is GILTI Calculated? A Step-by-Step Example

Let’s walk through Sarah’s UK marketing consultancy to show how GILTI calculations work:

Current Calculation:

- UK company gross income: $150,000

- Operating expenses: $30,000

- UK tested income: $120,000

- Less: 10% of QBAI (no qualifying assets): $0

- GILTI inclusion: $120,000

Without Section 962 Election:

- U.S. tax at 24% rate: $28,800

- No foreign tax credit for corporate taxes paid

With Section 962 Election:

- GILTI taxed at 10.5% effective rate: $12,600

- UK corporate tax paid (19%): $22,800

- Foreign tax credit (80% of $22,800): $18,240

- Net U.S. tax: $0 (foreign tax credit eliminates entire obligation)

Starting next year: You’ll need foreign tax rates of at least 14% to completely eliminate U.S. tax, up from the current 13.125% threshold.

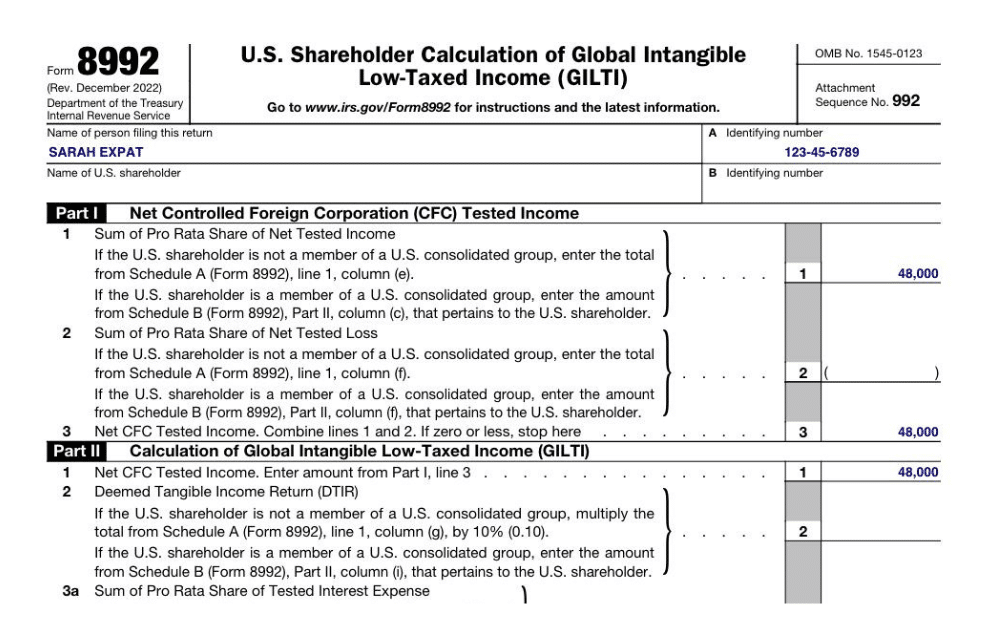

Here is an example of the Form 8992 used for GILTI calculation:

What Forms Do I Need to File for GILTI?

If you’re subject to GILTI, you’ll need these expat tax forms:

- Form 5471 (Information Return for Foreign Corporations)

- Form 8992 (GILTI Calculation)

- Form 8865 (if applicable for partnerships)

The filing deadline for expats is June 15 (with an automatic extension), which can be extended to October 15 if needed.

Critical: These forms carry significant penalties for late filing, up to $60,000 for Form 5471 alone. Don’t risk the penalties; file on time or request proper extensions.

Important Update: The IRS updated Form 8992 instructions in December 2024. If you’re in a domestic partnership, you no longer complete Form 8992 directly. Instead, use Schedule K-2 (Form 1065), Part VI, and Schedule K-3 (Form 1065), Part VI to report GILTI. Consolidated groups should use Schedule B (Form 8992) for combined reporting.

How Does the GILTI High Tax Exception Work?

Income taxed at foreign rates exceeding 90% of the U.S. corporate tax rate (currently 18.9%) can be excluded from GILTI calculations under the high-tax exception.

Countries where this often applies:

- Germany (26-33% rates)

- France (25-28% rates)

- Belgium (25% rate)

- Austria (25% rate)

This election must be applied consistently across all CFCs and can affect your Foreign Tax Credit availability.

Should I Use GILTI Elections or Foreign Tax Credit Strategies?

The best approach depends on your specific situation:

Choose Section 962 Election when:

- Your foreign corporation pays meaningful taxes (above 14% starting next year)

- You’re in a high U.S. tax bracket

- You don’t need current income distributions

Choose the disregarded entity when:

- Corporate income is below the Foreign Earned Income Exclusion limit ($130,000 for the current tax year, $132,900 for next year)

- You’re in a low-tax foreign jurisdiction

- You qualify for self-employment tax exemptions under totalization agreements

Choose Foreign Tax Credit when:

- You have significant passive income

- Foreign tax rates are very high

- You need flexibility in claiming different benefits for different income types

What Should I Know About Upcoming GILTI Changes?

The One Big Beautiful Bill introduces permanent changes starting 2026:

Key updates:

- Higher effective rates: From 10.5% to 12.6%

- Better foreign tax credit: From 80% to 90% of foreign taxes

- Elimination of QBAI deduction: All income is subject to GILTI

- Ownership timing change: U.S. shareholders owning CFC stock at any time during the tax year must include their pro rata share of Net CFC Tested Income, not just those owning on the last day of the year

- New name: “Net CFC Tested Income” replaces “GILTI”

Action needed: Review your current structure before year-end to ensure your strategy remains optimal under the new rules.

What Common GILTI Mistakes Should I Avoid?

Mistake 1: Assuming the Foreign Earned Income Exclusion protects against GILTI

The FEIE applies only to employment income, not to corporate distributions or deemed distributions.

Mistake 2: Not making beneficial elections

Many expats pay unnecessary taxes by defaulting to individual treatment instead of electing corporate rates.

Mistake 3: Poor timing of corporate distributions

Taking dividends in years with GILTI inclusions can create double taxation without proper planning.

Mistake 4: Ignoring upcoming changes

Current planning decisions should account for higher rates and eliminate deductions starting next year.

What Are My Next Steps?

GILTI planning doesn’t have to be overwhelming. Here’s your clear action plan:

- Determine your GILTI exposure by reviewing foreign corporation ownership percentages

- Calculate tax under different elections to identify your optimal strategy

- Consider upcoming changes in current planning decisions

- Implement proper elections before relevant deadlines

- Maintain compliance with all required forms and deadlines

With proper planning, most expat business owners can significantly reduce or eliminate their GILTI tax liability. The key is choosing and implementing the right strategy for your situation correctly.

No matter how late, messy, or complex your return may be, we can help. You’ll have peace of mind, knowing that your taxes were done right.

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on US expat taxes or working with Greenback, contact our Customer Champions.

Get Expert Help With GILTI Reporting

This article is for informational purposes only and does not constitute tax advice. Individual circumstances vary, and you should consult with a qualified tax professional regarding your specific situation. Tax laws and procedures are subject to change.

All dollar amounts, thresholds, rates, and regulatory updates have been verified against current IRS sources as of January 2026. Sources include IRS Instructions for Form 8992 (December 2024), IRS Notice 2025-75 (OBBBA implementation guidance), One Big Beautiful Bill Act provisions, Section 951A regulations, and IRS.gov GILTI guidance.

Related Resources

- Controlled Foreign Corporation (CFC): What You Need to Know

- Form 5471: Filing Requirements with Your Expat Taxes

- Section 962 Election: Tax Strategy for Expat Business Owners

- GILTI High Tax Exception: Exclude High-Taxed Foreign Income

- Section 250 Deduction for Expat Business Taxes

- Foreign Tax Credit: How Expats Can Reduce U.S. Taxes

- Foreign Business Tax Reporting: Forms and Requirements

- Foreign Earned Income Exclusion Guide

- Totalization Agreements: Avoid Double Social Security Tax

- Small Business Tax Return Prep for Americans Living Abroad