Schedule D Form 1040: How to Report Capital Gains and Losses on Your Tax Return

- What Is Schedule D?

- How Does Schedule D Work with Form 8949?

- When Do I Need to File Schedule D?

- How Do I Complete Schedule D?

- What If I Have Capital Losses?

- How Can I Reduce My Capital Gains Tax as an Expat?

- What's the Difference Between Schedule D and FBAR?

- What Mistakes Should I Avoid on Schedule D?

- What If I Made Mistakes or Missed Previous Years?

- Get Expert Help with Schedule D and Investment Reporting

Schedule D (Form 1040) is where you calculate your net capital gain or loss from selling investments like stocks, bonds, cryptocurrency, and real estate. According to IRS data, hundreds of thousands of Americans living abroad file Schedule D annually, and here’s the reassuring news: most expats end up owing little to no US tax on their investment gains after applying the Foreign Tax Credit for foreign taxes already paid.

Whether you sold foreign stocks, cryptocurrency, or property abroad, we’ll walk you through exactly what Schedule D is, how it works with Form 8949, and how to report your capital gains correctly.

You’ll have peace of mind knowing your investment reporting is accurate, and you’re not paying more US tax than necessary.

What Is Schedule D?

Schedule D (Capital Gains and Losses) is the IRS form that summarizes all your capital gains and losses for the year and calculates your net result. Think of it as the final scorecard that combines information from Form 8949 and other sources to determine your total taxable capital gains or deductible capital losses.

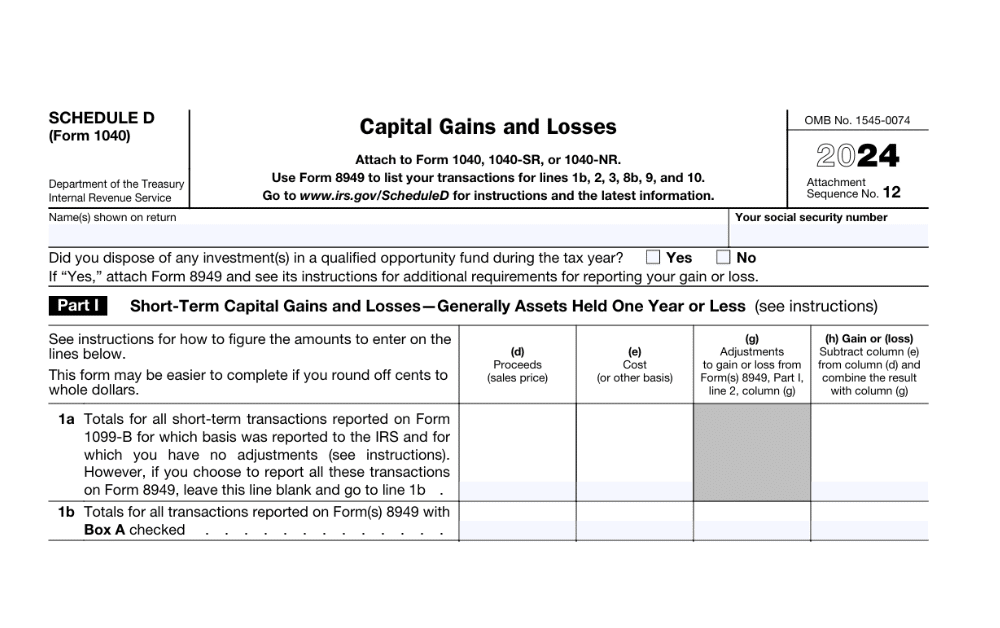

Schedule D has three parts:

- Part I: Short-term capital gains and losses (assets held one year or less)

- Part II: Long-term capital gains and losses (assets held more than one year)

- Part III: Summary section that calculates your net capital gain or loss and determines your tax

The final number from Schedule D flows to your Form 1040, where it becomes part of your total income calculation. If you have a net capital gain, Part III helps you determine whether to use the preferential long-term capital gains rates (0%, 15%, or 20%) or your ordinary income tax rates.

How Does Schedule D Work with Form 8949?

Schedule D and Form 8949 work together as a required two-step process for reporting investment sales:

- Step 1: Form 8949 lists every individual transaction with complete details, including dates, proceeds, cost basis, and gain or loss. This is where you report each stock sale, crypto transaction, or property sale separately.

- Step 2: Schedule D takes the totals from all your Form 8949 pages and combines them with other capital gain sources (like capital gain distributions from mutual funds or gains passed through from partnerships). Schedule D then calculates your overall net capital gain or loss.

You must complete Form 8949 before filling out lines 1b, 2, 3, 8b, 9, or 10 on Schedule D. The only exception is if you have simple transactions where:

- You received Form 1099-B showing that the basis was reported to the IRS

- You have no adjustments to make

- You had no wash sales

In these limited cases, you can report totals directly on Schedule D lines 1a or 8a without using Form 8949.

When Do I Need to File Schedule D?

You must file Schedule D whenever you have capital gains or losses to report. This requirement applies regardless of where you live or where your investments are located.

Typical situations requiring Schedule D for expats include:

- Sold stocks, bonds, or mutual funds (US or foreign)

- Disposed of cryptocurrency or NFTs

- Sold foreign rental property or vacation homes

- Sold your primary residence with gains exceeding the exclusion amount

- Received capital gain distributions from mutual funds

- Had gains or losses passed through from partnerships or S corporations (reported on Schedule K-1)

- Need to carry forward capital losses from previous years

- Sold inherited property

Even if you’re certain your investment sales won’t result in US taxes (perhaps because you paid higher foreign taxes), you still must report these transactions on Form 8949 and Schedule D.

How Do I Complete Schedule D?

Here’s how to work through Schedule D step by step:

Part I: Short-Term Capital Gains and Losses

- Line 1a: Report short-term transactions that don’t require Form 8949 (very rare for most expats).

- Line 1b: Total short-term gains and losses from all Form 8949, Part I pages. This includes stocks, crypto, or other assets you held for one year or less.

- Line 2: Short-term capital gain distributions from Form 1099-DIV (from mutual funds or REITs).

- Line 3: Short-term gains from installment sales (Form 6252) or other specialized situations.

- Lines 4-5: Add lines 1a through 3, then enter any short-term capital loss carryover from previous years.

- Line 6: Your short-term capital loss carryover (if any) from the prior year.

- Line 7: Net short-term capital gain or loss. This is the combination of all your short-term transactions.

Part II: Long-Term Capital Gains and Losses

- Line 8a: Report long-term transactions that don’t require Form 8949 (uncommon for expats).

- Line 8b: Total long-term gains and losses from all Form 8949, Part II pages. This includes investments you held for more than one year.

- Line 9: Long-term capital gain distributions from Form 1099-DIV.

- Line 10: Long-term gains from other sources like Form 4797 or partnerships.

- Lines 11-14: Add your long-term transactions and subtract any long-term capital loss carryover.

- Line 15: Net long-term capital gain or loss.

Part III: Summary and Tax Calculation

Line 16: Combine your net short-term result (line 7) and net long-term result (line 15).

If line 16 is a gain, you’ll continue through Part III to calculate your tax using the preferential capital gains rates if you qualify. You may need to complete the Qualified Dividends and Capital Gain Tax Worksheet or the Schedule D Tax Worksheet (both found in the Form 1040 instructions).

If line 16 is a loss, you can deduct up to $3,000 of that loss against your other income ($1,500 if married filing separately). Any loss exceeding this amount carries forward to future years.

Line 21: Your capital gain tax (if applicable) or the amount of loss you can deduct this year.

What If I Have Capital Losses?

Capital losses provide valuable tax benefits. Here’s how they work:

- Losses offset gains first: Your capital losses first offset capital gains of the same type (short-term losses offset short-term gains, long-term losses offset long-term gains). Any excess losses then offset the opposite kind of gain.

- Deduct up to $3,000 from other income: After offsetting all gains, you can deduct up to $3,000 of remaining capital losses ($1,500 if married filing separately) against your ordinary income, like wages or self-employment income.

- Carry forward unlimited losses: Capital losses that exceed the $3,000 annual limit carry forward indefinitely to future tax years. You report these carryover losses on line 6 (short-term) or line 14 (long-term) of next year’s Schedule D.

Example: Maria, an expat in Singapore, incurred a $15,000 long-term capital loss when she sold foreign stocks at a loss; however, she also realized a $5,000 long-term gain from the sale of cryptocurrency. Her net loss is $10,000 ($15,000 loss minus $5,000 gain). She can deduct $3,000 against her other income this year and carry forward $7,000 to future years.

How Can I Reduce My Capital Gains Tax as an Expat?

Most expats can significantly reduce or eliminate the US capital gains tax using these strategies:

Foreign Tax Credit

The Foreign Tax Credit provides dollar-for-dollar credits for foreign taxes paid on investment income. This is the most powerful tool for expats in high-tax countries.

Example: James sold shares in a UK company for a $20,000 long-term capital gain. He paid £3,800 (approximately $4,800) in UK capital gains tax. On his US return:

- Schedule D shows his $20,000 gain

- His US tax at 15% would be $3,000

- He claims a $3,000 Foreign Tax Credit on Form 1116

- Result: He owes $0 in US taxes, with $1,800 in unused credits to carry forward

Primary Residence Exclusion

If you sold your main home, you may exclude up to $250,000 of gain ($500,000 married filing jointly) using the Section 121 exclusion. You must have:

- Owned the home for at least 2 years in the 5-year period before the sale

- Lived in it as your primary residence for at least 2 of those 5 years

- Not used the exclusion in the past 2 years

This exclusion works for expats who sell their homes abroad or in the US.

Tax-Loss Harvesting

Strategically selling investments at a loss to offset gains can reduce your current-year tax bill. This strategy works particularly well in volatile markets or when you need to rebalance your portfolio anyway.

Long-Term Capital Gains Rates

Hold investments for more than one year to qualify for preferential long-term capital gains rates (0%, 15%, or 20%) instead of paying ordinary income tax rates (up to 37%) on short-term gains.

For the 2025 tax year, the long-term rates are:

- 0% rate: Single filers with taxable income up to $47,025 (married filing jointly up to $96,700)

- 15% rate: Single filers with taxable income $47,026 to $518,900 (married filing jointly $96,701 to $600,050)

- 20% rate: Single filers above $518,900 (married filing jointly above $600,050)

What’s the Difference Between Schedule D and FBAR?

Schedule D and FBAR serve completely different purposes:

- Schedule D reports capital gains and losses from investment sales, calculating what you owe in taxes. It’s part of your Form 1040 tax return.

- FBAR (FinCEN Form 114) reports foreign financial accounts with aggregate balances exceeding $10,000 at any time during the year. It’s purely informational and doesn’t calculate taxes. FBAR is filed separately with FinCEN, not with your tax return.

You might need both if you:

- Sold investments held in foreign brokerage accounts (Form 8949 and Schedule D)

- Have foreign accounts totaling over $10,000 (FBAR)

- Have foreign financial assets exceeding certain thresholds (Form 8938 / FATCA)

These are separate requirements with different deadlines and filing locations.

What Mistakes Should I Avoid on Schedule D?

Watch out for these common Schedule D errors:

- Forgetting Form 8949: You almost always need Form 8949 before completing Schedule D. Don’t try to skip this step.

- Miscalculating holding periods: Assets held exactly one year are short-term. Assets held for one year or more are considered long-term. This one-day difference can significantly affect your tax rate.

- Not claiming carryover losses: If you had capital losses in previous years that exceeded $3,000, make sure you carry them forward to the current year’s Schedule D.

- Missing the Foreign Tax Credit: If you paid foreign taxes on investment gains, claim the credit on Form 1116. This is how most expats avoid double taxation.

- Incorrect currency conversions: Convert all foreign currency amounts to US dollars using the exchange rate on the transaction date, not year-end rates.

- Not reporting losses: You must report capital losses even though they reduce your taxable income. The IRS requires disclosure of all transactions, gains, and losses.

What If I Made Mistakes or Missed Previous Years?

If you discover errors on previously filed Schedule D returns or forgot to report investment sales in past years, you have options:

- Amend recent returns: File Form 1040-X to correct errors on returns filed within the last three years.

- Catch up on multiple years: If you haven’t filed Schedule D for foreign investment sales in multiple years, the Streamlined Filing Compliance Procedures may help you catch up with reduced or eliminated penalties if your failure to file was non-willful.

The key is addressing errors proactively before the IRS contacts you. Once they initiate contact, your options for penalty relief become more limited.

Get Expert Help with Schedule D and Investment Reporting

Schedule D becomes complex quickly when you’re dealing with foreign investments, multiple currencies, and international tax credits. Many of our expat clients at Greenback come to us after attempting to file themselves and realizing they need expert guidance.

We’ve prepared Schedule D for thousands of expats with foreign investments, from simple mutual fund sales to complex portfolios involving foreign stocks, cryptocurrency, real estate, and partnership interests. Our CPAs and Enrolled Agents know how to maximize your Foreign Tax Credit, ensure all transactions are reported correctly, and keep you compliant with both Schedule D and related requirements like FBAR and/or FATCA.

No matter how complex your investment situation may be, we can help. You’ll work directly with a dedicated accountant who knows foreign investments and will prepare your Schedule D right.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

Foreign investment gains on your tax return? Our expat tax experts handle Schedule D so you pay only what you owe.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently, and individual circumstances vary. Please consult with a qualified tax professional regarding your specific situation.