Form 5472 for Expats Explained: Avoid $25,000+ Penalties on Foreign-Owned U.S. Corps

- Do I Need to File Form 5472?

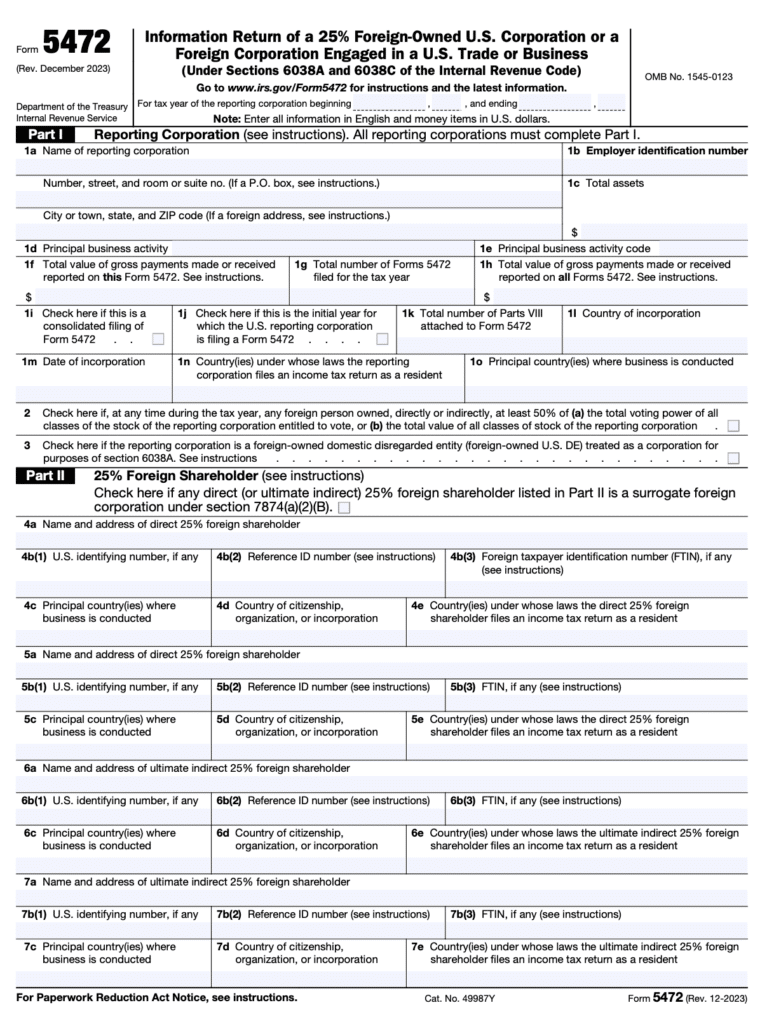

- What Is Form 5472?

- Form 5472 vs Form 5471: What's the Difference?

- Who Must File Form 5472? (Three Categories)

- Understanding the 25% Ownership Threshold

- What Transactions Must Be Reported?

- Form 5472 Filing Requirements and Deadlines

- 2025 Form 5472 Updates

- Penalties for Not Filing Form 5472

- Common Form 5472 Mistakes

- Late Filing: How to Get Back in Compliance

- Form 5472 FAQs

- Need Help Filing Form 5472?

Are you required to file Form 5472? If your U.S. corporation has 25% or more foreign ownership, you’re a foreign corporation doing business in the U.S., or you own a foreign-owned US LLC, the answer is yes.

Form 5472 carries a minimum $25,000 penalty for late filing or incomplete information, with additional $25,000 penalties every 30 days beyond 90 days after IRS notification. There’s no statute of limitations—the IRS can audit and penalize you indefinitely if you fail to file.

Do I Need to File Form 5472?

Start here to determine if you must file:

Step 1: Do you operate a U.S. corporation (including an LLC taxed as a corporation)?

- If YES → Continue to Step 2

- If NO → You likely don’t need Form 5472 (but check if you’re a foreign corporation below)

Step 2: Does any foreign person own 25% or more of your U.S. corporation (directly or indirectly)?

- If YES → You must file Form 5472

- If NO → Continue to Step 3

Step 3: Are you a foreign corporation engaged in U.S. trade or business?

- If YES → You must file Form 5472

- If NO → Continue to Step 4

Step 4: Do you own a US LLC (disregarded entity) and are you a foreign person?

- If YES → You must file Form 5472

- If NO → Form 5472 likely does not apply to you

You do NOT need Form 5472 if:

- Foreign ownership is below 25%

- You’re a U.S. citizen or resident owning a foreign corporation (you need Form 5471 instead)

- Your US LLC is owned by a U.S. person

- You had no reportable transactions during the tax year (rare exception)

Operating a U.S. business with foreign investors? We specialize in helping Americans who own businesses abroad navigate Form 5472 filing requirements, related party reporting, and international tax compliance. Let us handle the complexity while you focus on growing your business.

What Is Form 5472?

Form 5472 (Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business) is an IRS information return used to report financial transactions between U.S. corporations and their foreign shareholders or related parties.

The purpose is to ensure transparency in dealings between U.S. entities and foreign interests, helping the IRS monitor for tax avoidance and enforce transfer pricing rules under Sections 6038A and 6038C of the Internal Revenue Code.

Key point: Form 5472 is an information return, not a tax return. You don’t pay tax directly on this form, but it reports transactions that may affect your tax liability.

Not Sure If Form 5472 Applies to Your Business?

Form 5472 vs Form 5471: What’s the Difference?

Many business owners confuse these two forms. Here’s how they differ:

| Feature | Form 5472 | Form 5471 |

|---|---|---|

| Who Files | U.S. corporations with 25%+ foreign ownership OR foreign corporations in U.S. business | US corporations with 25%+ foreign ownership OR foreign corporations in U.S. business |

| Direction | U.S. persons owning 10%+ of foreign corporations | Foreign person owns U.S. entity |

| Purpose | Report transactions with foreign owners | Report ownership of controlled foreign corporations |

| Attached To | U.S. person owns foreign entity | Form 1040 (individual return) or Form 1120 |

| Deadline | March 15 (April 18 if extended) | June 15 for expats, October 15 with extension |

| Penalty | $25,000 per form | $10,000 per form |

Example:

- Need Form 5472: German investor owns 30% of your Delaware LLC

- Need Form 5471: You’re a U.S. citizen owning 15% of a UK limited company

For a detailed comparison: Form 5471 vs Form 5472: Complete Guide

Related: Form 5471 filing guide | Controlled foreign corporations

Who Must File Form 5472? (Three Categories)

1. 25% Foreign-Owned US Corporations

If any foreign person owns 25% or more of a U.S. corporation (directly or indirectly), the corporation must file Form 5472.

- Direct ownership example: Canadian investor owns 30% → Must file Form 5472

- Indirect ownership example: UK Corp A owns 60% of US Corp B, which owns 100% of US Corp C → Corp C must file (60% indirect foreign ownership)

2. Foreign Corporations Engaged in U.S. Trade or Business

Any foreign corporation conducting business in the United States must file Form 5472.

Example: A Japanese software company sells services to U.S. clients and maintains a U.S. sales office must file Form 5472 annually.

3. Foreign-Owned US Disregarded Entities (LLCs)

Foreign-owned US LLCs (disregarded entities) must file Form 5472 even without regular corporate tax returns.

How it works: Foreign person owns US LLC → LLC files pro forma Form 1120 with Form 5472 attached

Example: French entrepreneur owns Delaware LLC for U.S. real estate → Must file pro forma 1120 + Form 5472 annually

Important: Cannot e-file; must use special mailing/fax instructions.

Foreign-owned LLC causing compliance headaches? We help expat entrepreneurs understand pro forma 1120 filings, determine reportable transactions, and ensure you meet all U.S. reporting obligations without missing critical deadlines.

Understanding the 25% Ownership Threshold

The 25% threshold includes direct and indirect ownership, calculated on voting power OR total stock value.

Related party attribution rules: Count ownership by the shareholder’s family members and controlled entities.

Example: Foreign Individual A owns 15% + spouse owns 12% = 27% combined → Must file Form 5472

What Transactions Must Be Reported?

Form 5472 requires reporting all transactions between the U.S. corporation and foreign related parties, including:

Monetary transactions:

- Sales of inventory or tangible property

- Rents paid or received

- Royalties paid or received

- Interest on loans

- Service fees

- Commissions

Nonmonetary transactions:

- Loans or advances (even if interest-free)

- Use of tangible property

- Performance of services

- Cost-sharing arrangements

- Contributions to the entity

- Distributions from the entity

There is no de minimis threshold. Even small transactions must be reported.

Example: Your UK parent company lends your U.S. subsidiary $10,000, interest-free, to cover short-term cash flow needs. This must be reported on Form 5472 even though no interest was charged.

Form 5472 Filing Requirements and Deadlines

How to file:

- Determine eligibility using the decision guide above

- Gather information about all foreign shareholders and reportable transactions

- Complete Form 5472 (separate form for each foreign related party)

- Attach to Form 1120 (U.S. corporate tax return)

Deadline:

Same as your corporate tax return

- C Corporations: April 15 (can extend to October 15 with Form 7004)

- Note: Expats do NOT receive an automatic June 15 extension for corporate returns

Special rules for foreign-owned disregarded entities:

- Must file pro forma Form 1120 with limited information

- Cannot file electronically

- Must use special IRS mailing address or fax: 855-887-7737

- Write “Foreign-owned U.S. DE” at the top of Forms 1120 and 7004

Pro forma Form 1120 requirements:

- Name, address, and EIN of the disregarded entity

- Check the box indicating disregarded entity status

- Attach Form 5472 (for each foreign owner/transaction)

- No other schedules required

2025 Form 5472 Updates

Part VII line changes (December 2025):

- Line 39: Must complete Part VIII if answered “yes”

- Line 41a: Updated from “foreign corporation” to “foreign related party”

- Lines 42a-42b: New safe-haven interest rate questions

- Line 43a: Clarified covered debt instrument reporting

Penalties confirmed: $25,000 base + additional $25,000 per 30-day period beyond 90 days

Filing: Most can e-file; foreign-owned DEs must mail/fax

Penalties for Not Filing Form 5472

- Base penalty: $25,000 for failure to file, filing an incomplete form, or not maintaining required records

- Continuing penalties: Additional $25,000 for each 30-day period beyond 90 days after IRS notice (no maximum)

- No statute of limitations: Failing to file keeps your entire tax return open indefinitely

- Consolidated groups: Each member is subject to a separate $25,000 penalty

Example: Failed to file in 2023, IRS notice March 1, 2026, filed September 1, 2026 → Penalty: $25,000 + $75,000 (three 30-day periods) = $100,000

Facing Form 5472 penalties or worried about late filing? We help expat business owners catch up on missed filings, prepare reasonable cause statements, and work with the IRS to minimize or eliminate penalties. The key is addressing it before penalties escalate.

Common Form 5472 Mistakes

- Not filing for disregarded entities: Foreign-owned LLCs MUST file pro forma 1120 + Form 5472, regardless of tax liability.

- Missing nonmonetary transactions: Interest-free loans, use of property, and services must all be reported.

- Ignoring attribution rules: Include spouse, children, and controlled entities in 25% ownership calculations.

- Single form for multiple shareholders: File SEPARATE Form 5472 for each qualifying foreign shareholder.

- Electronic filing for DEs: Foreign-owned disregarded entities must mail or fax—cannot e-file.

Late Filing: How to Get Back in Compliance

If you’ve missed filing Form 5472, you can still come into compliance:

- File missing forms immediately for all missed years

- Include a reasonable cause statement: Explain why you didn’t file (didn’t know the requirement, relied on bad advice, administrative error)

- Maintain required records: Keep all transaction documentation for 3 years after filing

Related: Filing late business tax returns | Streamlined filing

Behind on Form 5472 filing? Don’t let penalties escalate. We’ve helped hundreds of foreign business owners catch up on years of unfiled forms with reasonable cause statements that often result in penalty relief. We’ll guide you through the entire catch-up process.

Form 5472 FAQs

Can I file Form 5472 electronically?

Most corporations can e-file. Exception: Foreign-owned US disregarded entities must mail to: Internal Revenue Service, 1973 Rulon White Blvd, M/S 6112, Attn: PIN Unit, Ogden, UT 84201 or fax: 855-887-7737

Do I need Form 5472 if my foreign owner is from a treaty country?

Yes, Form 5472 is required regardless of tax treaties.

What if I have multiple foreign shareholders?

File a separate Form 5472 for each foreign related party meeting the 25% threshold.

Can I get an extension to file Form 5472?

Yes. File Form 7004 by your corporate return deadline.

What’s the difference between Form 5472 and FBAR?

Form 5472: Reports transactions with foreign owners | FBAR: Reports foreign bank accounts over $10,000

Can penalties be waived for first-time filers?

Yes, with reasonable cause. Filing before the IRS contact increases the chances of a penalty waiver.

Need Help Filing Form 5472?

Form 5472 filing requirements are complex, and severe penalties apply for late or incomplete filings. Our team of expert CPAs and Enrolled Agents has deep expertise in helping Americans who own businesses abroad navigate international tax compliance.

We handle:

- Form 5472 preparation for all three filing categories

- Pro forma Form 1120 for foreign-owned disregarded entities

- Multiple foreign shareholder scenarios

- Related party transaction reporting

- Late filing and penalty abatement requests

- Form 1120 corporate tax returns

- Coordination with Form 5471 when applicable

Confused about foreign business reporting? Whether you need Form 5472, Form 5471, or both, our expat business specialists will determine your exact filing requirements, prepare all necessary forms, and ensure full compliance with U.S. tax law.

No matter how late, messy, or complex your return may be, we can help. You’ll have peace of mind, knowing that your taxes were done right.

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on US expat taxes or working with Greenback, contact our Customer Champions.

Ready to File Form 5472 Correctly?

This article provides general information and should not be construed as tax advice. Every business situation is unique, and tax laws change frequently. Consult with a qualified tax professional for advice specific to your circumstances.

Featured In