Form 8288 and FIRPTA Withholding Explained: Selling U.S. Real Estate

- Who Is Responsible for FIRPTA Withholding?

- What Triggers FIRPTA Withholding?

- What Are the FIRPTA Withholding Rates?

- Can I Reduce or Eliminate FIRPTA Withholding?

- How Is Form 8288 Filed?

- What Happens If Form 8288 Is Not Filed?

- How Does This Affect Expats?

- How Greenback Handles FIRPTA and Form 8288

- Related Resources

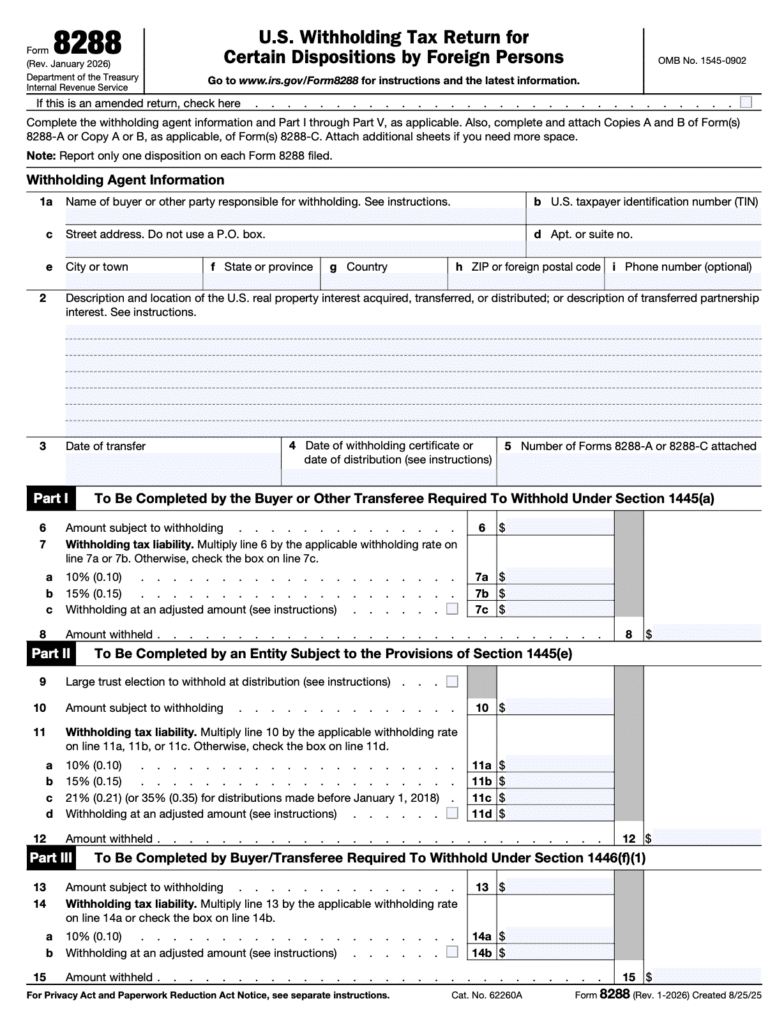

Form 8288 is the IRS withholding tax return that the buyer (or withholding agent) files when a foreign person sells or disposes of U.S. real property. According to the IRS, the buyer must withhold a percentage of the sale price, submit the withheld amount to the IRS, and file Form 8288 within 20 days of the transfer date.

The standard FIRPTA withholding rate is 15% of the total amount realized from the sale. However, reduced rates or exemptions may apply:

- 15% withholding: Default rate for most sales of U.S. real property by foreign persons

- 10% withholding: If the buyer will use the property as a residence and the sale price is between $300,001 and $1,000,000

- 0% withholding: If the buyer will use the property as a residence and the sale price is $300,000 or less

- 21% withholding: For certain corporate distributions of U.S. real property interests

This withholding is not the seller’s final tax bill. It is a prepayment that the foreign seller credits against their actual U.S. tax liability when they file a Form 1040-NR. If the withholding exceeds the actual tax owed, the seller receives a refund. Here is how the process works, who is responsible, and where things get complicated.

Selling U.S. Property as a Nonresident?

Who Is Responsible for FIRPTA Withholding?

The buyer, not the seller, is legally responsible for withholding and remitting FIRPTA tax. The IRS calls the buyer the “withholding agent.” If the buyer fails to withhold the correct amount, the IRS can hold the buyer personally liable for the tax that should have been withheld, plus interest and penalties.

In practice, the withholding responsibility works like this:

| Who | Responsibility |

|---|---|

| Buyer (withholding agent) | Must withhold from the sale proceeds, file Form 8288 and Form 8288-A with the IRS, and remit the withheld amount within 20 days |

| Seller (foreign person) | Receives reduced proceeds at closing; claims credit for the withheld amount on their U.S. tax return |

| Real estate agents /closing agents | May facilitate the process, but are not the withholding agent unless they assume that role; agents can be liable for penalties if they know the buyer did not withhold, and the seller is foreign |

| Seller’s or buyer’s attorney | Agents who represent parties in the transaction have their own liability under Section 1445 if they fail to notify the buyer of withholding requirements |

This is not a situation where the title company or closing attorney automatically handles everything. The buyer must ensure the withholding happens correctly, or the buyer bears the financial consequences.

What Triggers FIRPTA Withholding?

FIRPTA, the Foreign Investment in Real Property Tax Act, applies whenever a “foreign person” disposes of a “U.S. real property interest” (USRPI). Both terms are defined broadly by the IRS.

Who Is a “Foreign Person”?

A foreign person for FIRPTA purposes is anyone who is not a U.S. person. This includes:

- Non-resident aliens (individuals without a green card who do not meet the substantial presence test)

- Foreign corporations

- Foreign partnerships, trusts, and estates

U.S. citizens living abroad are not foreign persons, even if they have been out of the country for decades. Green card holders are also not foreign persons, regardless of where they live. FIRPTA withholding applies only when the seller is a non-U.S. person.

What Is a “U.S. Real Property Interest”?

A USRPI is broader than just a house or piece of land. It includes:

- Real property located in the United States or U.S. Virgin Islands (residential, commercial, land)

- Mines, wells, and natural resource deposits

- Certain personal property associated with the use of real property

- Interests in U.S. real property holding corporations (domestic corporations where 50%+ of assets are U.S. real property)

- Options, contracts, or rights to acquire U.S. real property

The “disposition” that triggers FIRPTA is also broad. It covers sales, exchanges, gifts, liquidations, and transfers. Essentially, whenever ownership of a USRPI changes from a foreign person to another party, FIRPTA withholding may apply.

What Are the FIRPTA Withholding Rates?

The withholding rate depends on the type of transaction and the sale price. Here are the rates that apply for the 2025 tax year:

| Situation | Withholding Rate | Applies To |

|---|---|---|

| Standard sale of USRPI by a foreign person | 15% of the amount realized | Most residential and commercial property sales |

| Buyer will use as a residence, and the sale price is $300,001 to $1,000,000 | 10% of the amount realized | Only if the buyer is an individual who will occupy the property at least 50% of the days it is in use over the next 2 years |

| Buyer will use as a residence, and the sale price is $300,000 or less | 0% (no withholding) | Same residency requirement as above |

| Sale price exceeds $1,000,000 | 15% of the amount realized | Regardless of the buyer’s intended use |

| Domestic corporation distributing USRPI to foreign shareholders | 21% of the gain recognized | Corporate distributions under Section 1445(e) |

| Transfer of partnership interest under Section 1446(f) | 10% of the amount realized | Non-publicly traded partnership interests with effectively connected income |

The “amount realized” is the total of cash paid, the fair market value of other property transferred, and any liabilities assumed by the buyer. This is typically the full sale price as stated on the closing documents.

Important: The withholding amount is often more than the seller’s actual tax liability. This is by design. The IRS collects upfront and refunds the difference when the seller files a tax return. For example, a foreign person selling a $500,000 property at the 15% rate would have $75,000 withheld, even if their actual capital gains tax is only $20,000.

Can I Reduce or Eliminate FIRPTA Withholding?

Yes. There are several ways to reduce or avoid FIRPTA withholding, but most require action before or at closing.

Withholding Certificate (Form 8288-B)

If the seller expects their actual tax liability to be less than the standard withholding amount, either the buyer or the seller can apply to the IRS for a withholding certificate using Form 8288-B. The IRS reviews the application and, if approved, authorizes withholding at a reduced rate or amount that matches the anticipated tax liability.

The IRS typically processes withholding certificate applications within approximately 90 days. During this period, the buyer must still withhold the full amount at closing. However, the buyer can delay filing Form 8288 and remitting the withholding until 20 days after the IRS approves or denies the certificate. If approved, the buyer sends only the reduced amount and refunds the balance to the seller.

This is one of the most valuable tools available to foreign sellers, particularly when the gain on the sale is small relative to the sale price. Without the certificate, 15% of the sale price is held by the IRS until the seller files a return and receives a refund, which can take months.

Seller Provides Certification of Non-Foreign Status

If the seller is actually a U.S. person (citizen, green card holder, or resident alien), they can provide a certification of non-foreign status to the buyer. This written statement, signed under penalties of perjury, includes the seller’s name, U.S. taxpayer identification number, and a declaration that they are not a foreign person. If the buyer receives this certification, no FIRPTA withholding is required.

Other Exceptions

FIRPTA withholding is not required when:

- The seller realizes $0 on the transaction (such as a gift with no consideration)

- The property is acquired by the U.S. government or a state or local government

- The IRS issues a withholding certificate, eliminating the requirement

- The transaction involves certain publicly traded stock of a REIT (different rules apply)

Need Help With Form 8288 and 8288-A?

How Is Form 8288 Filed?

Form 8288 must be filed by the 20th day after the date of transfer. The “date of transfer” is the first date on which consideration is paid or a transfer takes place, typically the closing date.

The buyer files Form 8288 along with:

- Form 8288-A (one for each foreign seller): Reports the seller’s information, the amount withheld, and the property details. The IRS stamps Copy B and returns it to the seller, who needs it to claim the withholding credit on their tax return.

- Payment of the withheld amount

The form is mailed to the IRS Ogden Service Center at P.O. Box 409101, Ogden, UT 84409. The January 2026 revision of Form 8288 added new sections for partnership interest transfers under Section 1446(f), expanding the form from its original FIRPTA-only scope.

Each Form 8288 should report only one disposition. If multiple properties are sold in the same transaction, separate forms are required.

What Happens If Form 8288 Is Not Filed?

The consequences for failing to file Form 8288 or failing to withhold the required amount are serious and fall primarily on the buyer:

- Personal liability: If the buyer fails to withhold the required tax, the IRS can collect the full amount, plus interest. This is the buyer’s liability, separate from and in addition to any tax the seller may owe.

- Late filing penalties: Under Section 6651, failure to file Form 8288 on time or failure to pay the withheld tax on time results in penalties. The late filing penalty is 5% of the unpaid tax per month, up to 25%. The late payment penalty is 0.5% per month, up to 25%.

- Willful failure penalty: Under Section 7202, willfully failing to collect or pay withholding tax can result in a fine of up to $10,000.

- Agent liability: Real estate agents, attorneys, or other agents involved in the transaction can also be held liable if they knew the buyer was required to withhold and failed to ensure compliance.

If you have already closed on a transaction and realize the withholding was not handled correctly, filing Form 8288 late is far better than not filing at all. The IRS may waive penalties if you can demonstrate reasonable cause for the delay.

How Does This Affect Expats?

FIRPTA and Form 8288 intersect with expat taxes in two common scenarios:

Scenario 1: You Are Buying U.S. Property from a Foreign Seller

If you are a U.S. citizen or green card holder purchasing property from a non-U.S. person, you are the withholding agent. You must withhold the correct percentage, file Form 8288 within 20 days, and remit the withheld tax to the IRS. This responsibility exists regardless of whether you live in the U.S. or abroad.

Scenario 2: You Gave Up Your Green Card and Are Selling U.S. Property

If you were a green card holder who relinquished your status and later sold U.S. property, you are now a non-resident alien. The buyer must withhold under FIRPTA, and you will need to file Form 1040-NR to report the sale and claim credit for the amount withheld. If you are a covered expatriate, additional rules may apply.

For U.S. citizens living abroad who own U.S. property, FIRPTA does not apply to your sale because you are not a foreign person. However, you still need to report the sale on your U.S. tax return and may owe capital gains tax. See our guide on selling U.S. property as an expat for details.

How Greenback Handles FIRPTA and Form 8288

FIRPTA transactions involve tight deadlines, specific withholding calculations, and coordination between buyers, sellers, and the IRS. Getting any part wrong can result in penalties for the buyer or months of delayed refunds for the seller.

- Determining whether FIRPTA applies: Your Greenback accountant reviews the transaction to confirm whether the seller is a foreign person, whether the property qualifies as a USRPI, and whether any exceptions eliminate the withholding requirement.

- Calculating the correct withholding rate: The rate depends on the sale price, the buyer’s intended use of the property, the type of entity involved, and whether a withholding certificate has been issued. Your accountant ensures the right rate is applied so neither party faces unexpected liability.

- Preparing and filing Form 8288 within the 20-day deadline: The tight filing window leaves little room for error. Your accountant prepares Form 8288 and Form 8288-A, coordinates with closing agents, and ensures the withheld amount is remitted on time.

- Applying for a withholding certificate (Form 8288-B). If the seller’s actual tax liability is significantly less than the standard withholding, your accountant prepares the withholding certificate application to reduce the amount locked up with the IRS and free up funds for the seller sooner.

- Filing the seller’s tax return to recover excess withholding. For foreign sellers, the withheld amount is credited on Form 1040-NR. Your accountant prepares the return to claim the refund for any amount withheld in excess of the actual tax due.

No matter how late, messy, or complex your real property transaction may be, we can help. You will have peace of mind, knowing that your taxes were done right.

If you are ready to be matched with a Greenback accountant, click the get started button below. For questions about FIRPTA withholding or Form 8288, contact us, and one of our Customer Champions will be happy to help.

Get FIRPTA Done Right the First Time

This article is for informational purposes only and does not constitute tax, legal, or accounting advice. FIRPTA rules are complex and transaction-specific. For guidance on your specific real property transaction, contact Greenback to speak with a tax specialist.

Related Resources

- Selling U.S. Property as a Foreign Resident or Expat

- Can Foreigners Buy Property in the U.S.?

- U.S. Taxes on Foreign Property: Buying and Selling Real Estate Abroad

- Capital Gains Tax for Non-Residents Selling U.S. Property

- Investing in U.S. Property as a Foreigner: Tax Implications

- How to Minimize Capital Gains Tax on Foreign Property

- Selling Your House While Living Abroad

- Green Card Holder Selling Foreign Property: Tax Questions Answered

- What Is the Exit Tax for U.S. Expatriates?

- Form 1040 for U.S. Expats: Filing Made Simple