Use IRS Form 1116 to Claim Credit for Foreign Taxes

- When Must You File Form 1116?

- Before You Start: Choose Your Accounting Method

- Part I: Taxable Income or Loss From Foreign Sources

- Part II: Foreign Taxes Paid or Accrued

- Part III: Figuring the Credit

- Part IV: Summary of Credits From All Categories

- Supporting Documentation You'll Need

- Common Form 1116 Mistakes to Avoid

- Form 1116 vs. Foreign Earned Income Exclusion

- Where to Find Form 1116 and Instructions

- Let Greenback Handle Your Form 1116

What is Form 1116?

IRS Form 1116 (sometimes called the Foreign Tax Credit form) is used by U.S. citizens or residents to claim a credit for income taxes paid to a foreign country, thereby avoiding double taxation on the same income. Put another way, it is used for calculating, reporting, and offsetting foreign taxes against U.S. tax liability with the IRS Foreign Tax Credit, which gives the taxpayer a dollar-for-dollar credit for income taxes paid to foreign governments.

Filing Form 1116 correctly is essential to claiming this credit. The form has four main parts:

- Reporting foreign income

- Listing foreign taxes paid

- Calculating your credit limitation

- Summarizing your total credit.

Most expats will need to file a separate Form 1116 for each income category (general, passive, etc.).

You Can Claim the Foreign Tax Credit Correctly

Who needs to file IRS Form 1116?

You’ll need to file Form 1116 if any of these apply to you:

- Your foreign taxes paid exceed $300 (single filers) or $600 (married filing jointly)

- You have foreign-earned income from wages or self-employment

- You’re claiming the Foreign Tax Credit for any taxes to countries designated under Section 901(j)

- You want to carry forward or carry back unused foreign tax credits

You MAY claim the credit without Form 1116 if:

- All foreign income is passive (interest, dividends)

- All income is reported on Form 1099

- Foreign taxes are $300 or less (single) or $600 or less (married filing jointly)

- No foreign-earned income

In this limited “de minimis” exception, you can claim the credit directly on Schedule 3 (IRS Form 1040). However, filing Form 1116 even if you don’t have credits to carry forward or back can be valuable for future tax planning.

You need a separate Form 1116 for each income category. If you have both wages (general category) and dividend income (passive category), you’ll file two Forms 1116.

Before You Start: Choose Your Accounting Method

Form 1116 requires you to indicate your accounting method at the top of the form. This determines when you claim foreign taxes.

Cash Method (Most Common)

- Report income when you actually receive it

- Claim foreign taxes in the year you actually paid them

- Used by most individuals

Accrual Method

- Report income when you earn it (regardless of when paid)

- Claim foreign taxes in the year they accrue (regardless of when paid)

- Often used by businesses or those required to use accrual accounting

If you’re unsure which method applies to you, you’re likely using the cash method. The method you choose must be consistent with how you report income on your entire tax return.

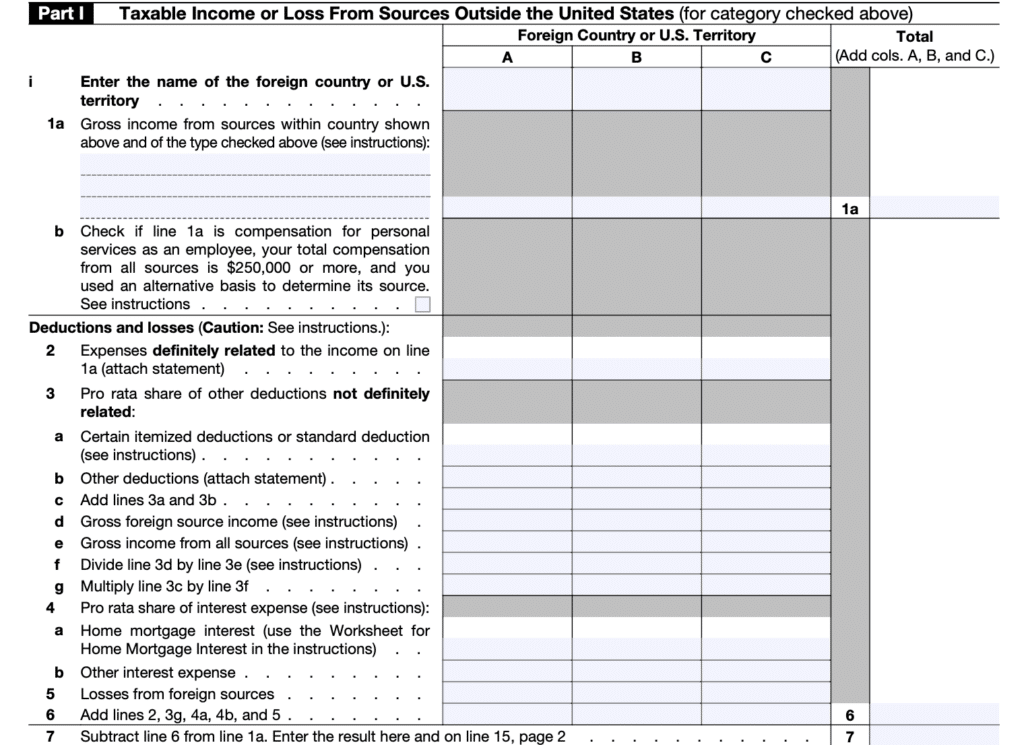

Part I: Taxable Income or Loss From Foreign Sources

This section categorizes your foreign income and calculates how much came from foreign sources versus U.S. sources.

Income Categories on Form 1116

You must check ONE box at the top of Form 1116 to indicate your income category. Each category requires a separate form:

a. Section 951A Category Income (GILTI)

- Income from controlled foreign corporations under global intangible low-taxed income rules

- Required if you own 10%+ of a foreign corporation

- See Form 5471 for related requirements

b. Foreign Branch Category Income

- Income from qualified business units operating as branches abroad

- Must meet specific technical requirements for QBU status

c. Passive Category Income

- Dividends from foreign stocks

- Interest from foreign bank accounts

- Royalties from foreign licenses

- Rental income from foreign property

- Annuity payments

- Capital gains from passive investments

d. General Category Income

- Wages and salaries from foreign employment

- Self-employment income from services performed abroad

- Business income that doesn’t qualify for other categories

- Also includes passive income, “kicked out” to the general category due to high foreign taxes

e. Section 901(j) Income

- Income from countries designated as supporting terrorism or lacking diplomatic relations with the U.S.

- Currently includes Iran, North Korea, Syria, and Cuba

- Special restrictions apply

f. Certain Income Re-sourced by Treaty

- Income treated as foreign-source under a tax treaty but would otherwise be U.S.-source

- Requires Form 8833 to claim treaty position

g. Lump-Sum Distributions

- Distributions from foreign pension plans taken as lump sums

- Subject to special tax treatment

Completing Part I Lines

- Lines 1a-1b: Report your gross income from foreign sources in the category you selected. Separate columns are provided for up to three countries.

- Line 2: List any expenses definitely related to the foreign income (like foreign rental property expenses).

- Lines 3a-3g: Deductions that must be apportioned between foreign and U.S. income (like home mortgage interest, state taxes, charitable contributions).

- Lines 4-7: Additional adjustments for specific situations like losses and other deductions.

The result shows your net foreign income for this category, which flows to Part III for the credit calculation.

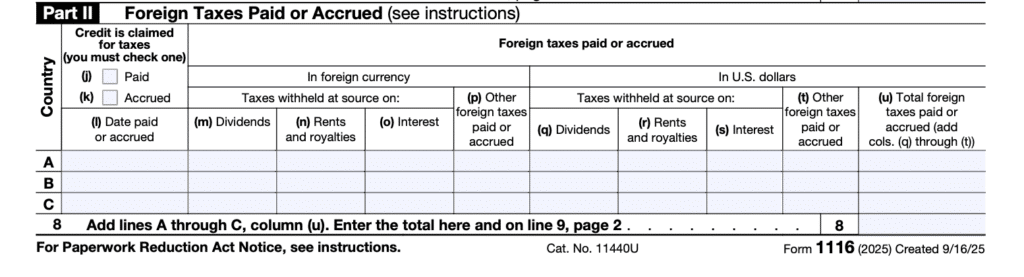

Part II: Foreign Taxes Paid or Accrued

This is where you list the actual foreign taxes you’re claiming as a credit.

Currency Conversion Requirements

You must report foreign taxes in BOTH the foreign currency and U.S. dollars:

- Column (p): Foreign taxes paid in foreign currency

- Column (u): Foreign taxes converted to U.S. dollars

Critical: Use the correct exchange rate for conversion:

- Cash Method: Use the exchange rate on the date you paid the taxes

- Accrual Method: Use the exchange rate on the last day of the tax year in which the taxes accrued

Find historical exchange rates on the IRS website or through OANDA.com. Keep documentation of which rate you used and when.

Reporting Taxes from Multiple Countries

If you paid taxes to more than one country within the same income category:

- Use Line A for the first country

- Use Line B for the second country

- Use Line C for the third country

- Attach additional sheets if you paid taxes to more than three countries

List each country separately, even if they’re in the same income category. Don’t combine countries on a single line.

What Foreign Taxes Qualify for the Credit?

Only include taxes that meet the four requirements for creditable foreign taxes:

- Income tax (or tax in lieu of income tax)

- Legally imposed on you

- Actually paid or accrued

- Paid to a recognized foreign government

Don’t include VAT, sales taxes, property taxes, or penalties and interest. For more details on what qualifies, see our comprehensive Foreign Tax Credit guide.

One Small Error Can Limit Your Credit

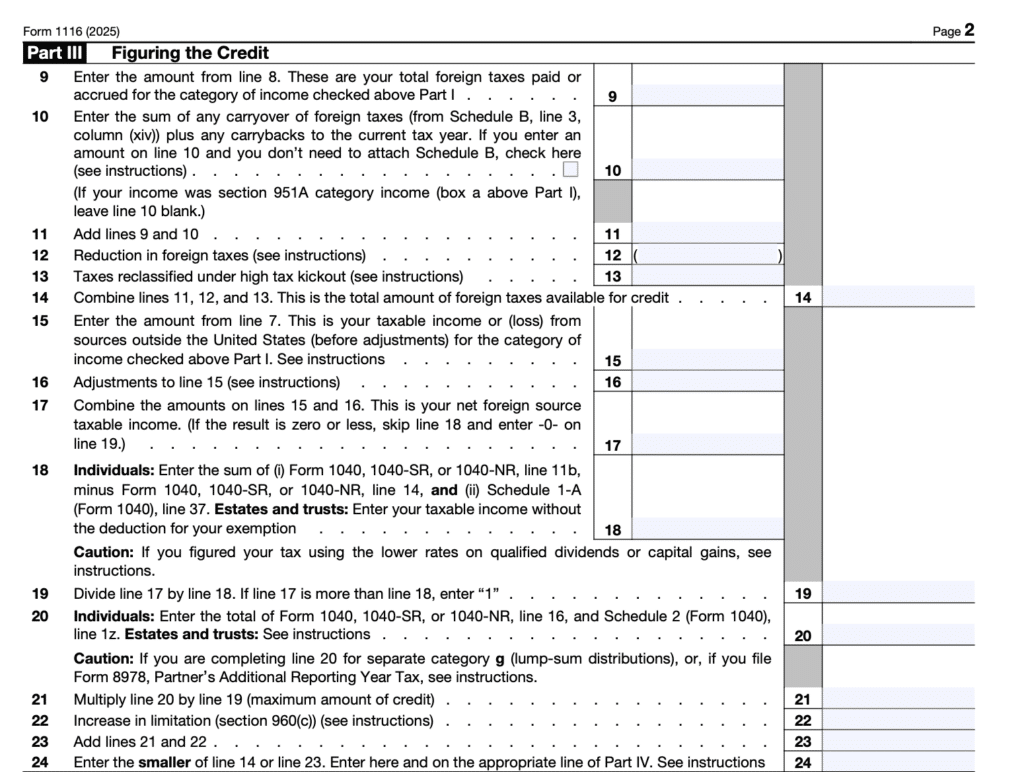

Part III: Figuring the Credit

This is the most technical section, where you calculate the limitation on your foreign tax credit.

The IRS limits your credit to ensure you only get credit for foreign taxes on foreign income. The limitation formula is:

Foreign Tax Credit Limit = U.S. tax liability × (Foreign income ÷ Total worldwide income)

Key Lines in Part III

- Line 9: Total foreign taxes from Part II

- Line 10: Any carryover from prior years or carryback from future years

- Line 11: Combined foreign taxes available

- Line 12: Reduction in foreign taxes (for situations like international boycott operations)

- Line 13: Taxes reclassified under high-tax kickout rules (passive income moved to the general category)

- Lines 14-22: Calculate your taxable income from all sources and the portion that’s foreign

- Line 23: Tentative credit before limitations

- Line 24: Your final credit for this category

The form ensures you don’t claim more credit than the U.S. tax you would have owed on that foreign income.

What If My Credit Exceeds My Tax Liability?

If your Foreign Tax Credit is larger than your U.S. tax liability, you don’t lose the excess. You can carry back 1 year to the previous tax year or carry forward up to 10 years to future tax years.

This Foreign Tax Credit carryover ensures you get full value from foreign taxes paid, even if you can’t use them all in the current year.

Exception: GILTI income (Section 951A) does NOT allow carryovers.

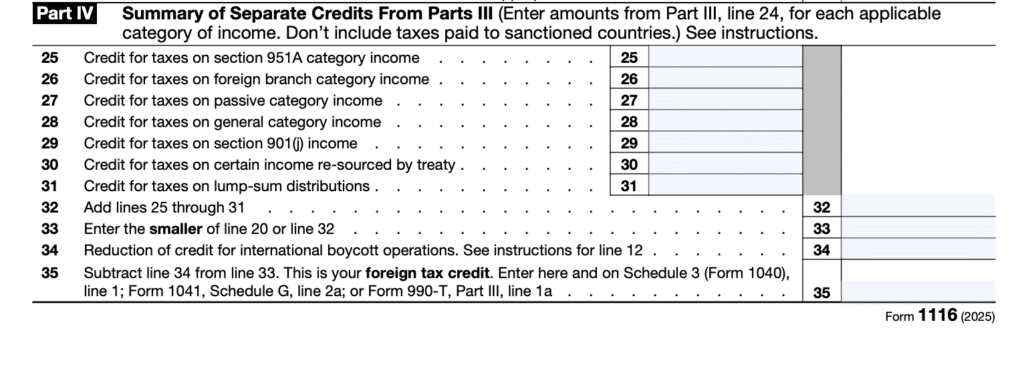

Part IV: Summary of Credits From All Categories

If you filed multiple Forms 1116 for different income categories, this section totals them.

- Line 33: Add up the credits from line 24 of all your Forms 1116

- Line 34: Reduction for international boycott operations or other special situations

- Line 35: Your total Foreign Tax Credit, which transfers to Schedule 3 (Form 1040)

This final number is your dollar-for-dollar reduction in U.S. tax liability.

Supporting Documentation You’ll Need

When filing Form 1116, attach or be prepared to provide:

Form 1116 Explanation Statement

The statement should show:

- How you calculated the foreign tax credit

- Currency conversion rates used and dates

- Breakdown of foreign taxes by country

- Any adjustments or special calculations

Learn more about Form 1116 explanation statements and what to include.

Foreign Tax Documents

- Foreign tax returns showing taxes paid

- Withholding statements from foreign employers

- Bank statements showing tax payments

- Foreign 1099-equivalent forms (like UK P60, German Lohnsteuerbescheinigung)

Income Documentation

- Foreign payslips or earnings statements

- Foreign bank interest statements

- Dividend statements from foreign investments

- Rental income records for foreign property

Common Form 1116 Mistakes to Avoid

- Using the wrong income category: Putting wages in the passive category or dividends in the general category will trigger IRS questions. Each income type has a specific category.

- Not filing separate forms for each category: If you have both wages and investment income, you need two Forms 1116—one for the general category, one for the passive category.

- Incorrect currency conversion: Using year-end rates instead of the rate on the payment date (cash method) is a common error that will affect your credit amount.

- Forgetting to check the box: The income category checkbox at the top of Part I must be checked, or the IRS won’t know which limitation rules to apply.

- Combining multiple countries on one line: Each country needs its own line in Part II, even if they’re in the same category.

- Not carrying forward unused credits: If your foreign taxes exceed your U.S. tax liability, track the excess on Schedule B (Form 1116) for use in future years. The carryover can be used for up to 10 years.

Form 1116 vs. Foreign Earned Income Exclusion

Many expats wonder whether to use Form 1116 for the Foreign Tax Credit or Form 2555 for the Foreign Earned Income Exclusion. The answer depends on your situation:

Form 1116 works best when:

- You live in a high-tax country (Germany, France, the UK, Canada)

- You earn more than $130,000 (the 2025 FEIE limit)

- You have passive income, like dividends or rental income

- You want to contribute to U.S. retirement accounts

Form 2555 (FEIE) works best when:

- You live in a low-tax or no-tax country

- Your foreign-earned income is below $130,000

- You meet the physical presence or bona fide residence tests

You cannot use both on the same income, but many expats use the FEIE for their first $130,000 of salary and Form 1116 for income above that or for passive income. For a detailed comparison, see FEIE vs FTC.

Where to Find Form 1116 and Instructions

Download the current Form 1116 from the IRS website. The official IRS instructions for Form 1116 provide line-by-line guidance.

Form 1116 is filed as an attachment to your Form 1040. The credit amount from Part IV, Line 35 flows to Schedule 3 (Form 1040), Line 1.

Filing Deadlines

- June 15 for expats abroad (automatic extension)

- October 15 with additional extension (must file Form 4868 or Form 2350)

Even with an extension to file, pay any estimated taxes by April 15 to avoid interest charges.

Let Greenback Handle Your Form 1116

Form 1116 requires precise calculations, correct categorization, and proper documentation. One small error can delay your refund or trigger an IRS inquiry.

Greenback Expat Tax Services has deep expertise in expat taxes and in preparing Form 1116. We’re an American company founded in 2009 by U.S. expats for expats. We’ve helped 23,000+ expats file 71,000+ returns while maintaining a 4.9-star rating across 1,200+ TrustPilot reviews.

Our CPAs and Enrolled Agents live in 14 time zones, and many are expats themselves. They’ll complete Form 1116 correctly, attach all required documentation, and ensure you get the maximum Foreign Tax Credit you’re entitled to. You’ll have peace of mind knowing that your taxes were done right.

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on U.S. expat taxes or working with Greenback, contact our Customer Champions.

Make Sure Form 1116 Is Actually Reducing Your Taxes

Disclaimer: This article provides general information about Form 1116. Tax laws are complex and subject to change. For advice specific to your situation, consult with a qualified tax professional.