FATCA Exemptions: Who Qualifies and How to Avoid Reporting

- How Do FATCA Reporting Thresholds Work?

- Who Qualifies for Individual Exemptions?

- What Assets Are Automatically Exempt?

- Are There Exemptions for Assets Reported Elsewhere?

- Which Financial Institutions Are FATCA-Exempt?

- What About Special Situations and Edge Cases?

- How Do FATCA and FBAR Exemptions Differ?

- What If I Don't Qualify for an Exemption?

- Get Expert Help Determining Your Exemption Status

- Frequently Asked Questions About FATCA Exemptions

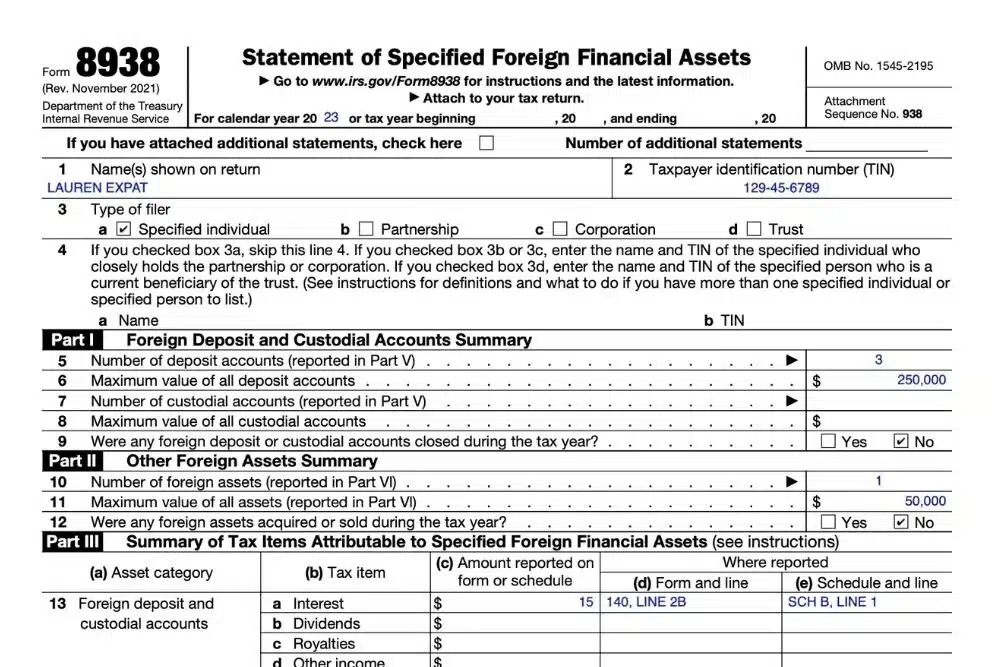

Most Americans with foreign assets qualify for FATCA exemptions and are not required to file Form 8938. According to the IRS, exemptions apply based on asset thresholds, asset types, and whether assets are already reported on other IRS forms. Thresholds are significantly higher for Americans living abroad, reaching up to $400,000 for married filers, meaning many expats with foreign holdings owe no FATCA reporting at all.

Need FATCA basics first? Start with our FATCA guide to learn the foundational requirements.

Ready for the next step? Learn more about our FATCA Reporting services.

How Do FATCA Reporting Thresholds Work?

The most common way to avoid FATCA reporting is to stay below the threshold amounts. If your foreign financial assets remain under these limits, you’re automatically exempt from filing Form 8938, no matter what types of assets you own.

Threshold Amounts for Exemption

For Americans Living Abroad:

- Single filers: Exempt if assets stay under $200,000 on December 31 AND under $300,000 at all times during the year

- Married filing jointly: Exempt if assets stay under $400,000 on December 31 AND under $600,000 at all times during the year

For Americans Living in the United States:

- Single filers: Exempt if assets stay under $50,000 on December 31 AND under $75,000 at all times during the year

- Married filing jointly: Exempt if assets stay under $100,000 on December 31 AND under $150,000 at all times during the year

You must stay below BOTH thresholds to qualify for this exemption. Exceeding either the year-end OR the maximum-during-year amount triggers reporting obligations, even if you drop below the threshold before year-end.

How to Calculate Your Total

Add up all your specified foreign financial assets on:

- The last day of the tax year (December 31)

- The highest point at any time during the year

Use U.S. dollar values. If assets are held in foreign currency, convert using the applicable exchange rates from the U.S. Treasury.

Who Qualifies for Individual Exemptions?

Beyond threshold-based exemptions, specific categories of individuals receive blanket exemptions from FATCA filing requirements.

Government Employees and Military Personnel

Certain U.S. government employees stationed abroad may be exempt from FATCA reporting for specific accounts:

- Military servicemembers with accounts on base

- Diplomatic personnel with host-country accounts required for their position

- Other federal employees with accounts specifically mandated by their employment

This exemption is narrow and applies only to accounts directly required for government service. Personal investment accounts, foreign retirement plans, and other private assets still count toward thresholds.

U.S. Territory Residents

Bona fide residents of U.S. territories may qualify for FATCA exemptions under specific circumstances:

- Puerto Rico residents

- U.S. Virgin Islands residents

- Guam residents

- American Samoa residents

- Northern Mariana Islands residents

Territory-based exemptions depend on tax home status and the source of income. This is a complex area that often requires professional guidance to determine eligibility correctly.

What Assets Are Automatically Exempt?

Even when you exceed reporting thresholds, certain asset types receive automatic exemptions and never need disclosure on Form 8938.

Physical Assets and Non-Financial Property

The following categories are NOT considered specified foreign financial assets:

Cash and Commodities:

- Physical currency held outside bank accounts

- Gold, silver, platinum, and other precious metals (physical holdings only)

- Cryptocurrency held in private wallets (though this remains an evolving area)

Real Property:

- Foreign real estate titled in your individual name

- Foreign vacation homes owned directly

- Rental properties abroad held in personal name

Real estate held through a foreign corporation, partnership, or trust is NOT exempt. The entity ownership itself must be reported, even though direct real estate ownership is exempt.

Personal Effects:

- Vehicles registered abroad

- Jewelry and collectibles

- Artwork and antiques

- Personal possessions and household items

Foreign Retirement and Social Security Accounts

Certain retirement and social benefit accounts qualify for exemptions:

Foreign Social Security Equivalents:

- Australian Superannuation

- UK State Pension

- Canadian Pension Plan (CPP)

- Other foreign government pension programs are similar to the U.S. Social Security program.

Government-Sponsored Retirement Plans: These typically don’t require Form 8938 disclosure when they’re mandatory government programs, such as U.S. Social Security.

Private foreign retirement accounts (like Canadian RRSPs) may require reporting on other forms, creating a different type of exemption discussed in the next section.

Are There Exemptions for Assets Reported Elsewhere?

Yes. One of the most valuable FATCA exemptions applies when you’ve already reported an asset on another IRS form. Assets disclosed elsewhere don’t require duplicate reporting on Form 8938.

Assets Reported on Specialized Forms

Foreign Corporation Ownership:

- Disclosed on Form 5471 (controlled foreign corporations)

- Covers ownership of 10% or more in foreign companies

Foreign Partnership Interests:

- Disclosed on Form 8865

- Includes both operating partnerships and investment partnerships

Foreign Trust Involvement:

- Disclosed on Form 3520 (foreign trusts and gifts)

- Covers both grantor and beneficiary relationships

PFIC Holdings:

- Disclosed on Form 8621

- Includes foreign mutual funds meeting passive income tests

Foreign Disregarded Entities:

- Disclosed on Form 8858

- Single-member LLCs and other entities are treated as disregarded for tax purposes

How the Alternative Form Exemption Works

Here’s the critical part many people miss:

Step 1: Calculate your total specified foreign financial assets (including assets that will be reported on other forms)

Step 2: Determine if you exceed the reporting threshold

Step 3: If yes, file Form 8938 but exclude assets already disclosed on Forms 5471, 8865, 3520, 8621, or 8858

The key is that these assets still count toward your threshold calculation. They are not listed again on Form 8938 itself.

Which Financial Institutions Are FATCA-Exempt?

Some financial institutions qualify as FATCA-exempt, which can impact your disclosure obligations:

Types of Exempt Institutions

Government Financial Institutions:

- National central banks (Bank of Canada, Bank of England, etc.)

- Government-owned investment funds

- Sovereign wealth funds

Qualified Retirement Plan Providers:

- Institutions offering government-approved retirement accounts

- Plans meet the treaty requirements for retirement savings

Charitable Organizations:

- Foreign non-profits holding funds exclusively for charitable purposes

- Religious organizations with qualifying accounts

Why Institution Exemptions Matter

If an institution is FATCA-exempt, it may not report your account to the IRS under institutional FATCA requirements. However, this doesn’t automatically exempt you from individual reporting obligations on Form 8938. You still need to evaluate whether your assets exceed the thresholds.

What About Special Situations and Edge Cases?

How Do Joint Accounts Work?

Holding foreign accounts jointly with a non-US spouse or family member doesn’t create an exemption. However, you only count your ownership percentage when calculating whether you exceed thresholds.

Example: A $300,000 joint account with a non-US spouse counts as $150,000 of your specified foreign financial assets (assuming 50/50 ownership).

Do Small Accounts Count?

Yes. Accounts under $10,000 still need to be included in threshold calculations. While small individually, multiple small accounts can collectively trigger reporting requirements.

Remember: FATCA looks at your total foreign assets across all accounts and investments, not individual account sizes.

What Happens with Inherited Foreign Assets?

Receiving an inheritance doesn’t create an automatic exemption. Inherited foreign accounts and investments count toward FATCA thresholds and may require reporting.

Special consideration: Large inheritances may also trigger Form 3520 filing requirements for foreign gifts, thereby creating the alternative-form exemption discussed earlier.

Are Business Assets Different?

Foreign assets held for use in an active trade or business (not for investment) may not qualify as “specified foreign financial assets.” This creates a potential exemption, but the distinction is highly fact-specific and requires careful analysis.

Example: A foreign business bank account used solely for active business operations might not be reportable, while the same business’s investment account would be.

What If I Closed Accounts During the Year?

Closing a foreign account before year-end doesn’t create an exemption if you exceeded thresholds at any point during the year. The maximum value at any time determines reporting obligations, not the year-end balance.

How Do FATCA and FBAR Exemptions Differ?

FATCA exemptions differ significantly from FBAR exemptions, and you must evaluate each filing requirement separately:

| Factor | FATCA Exemption | FBAR Exemption |

|---|---|---|

| Reporting threshold | $200,000 to $600,000 depending on filing status and residency | $10,000 aggregate across all accounts at any point during the year |

| Real estate | Direct ownership always exempt | Not applicable, FBAR covers financial accounts only |

| Retirement accounts | Some exempt via alternative forms | Generally reportable |

| Filing deadline | Tax return due date | October 15 annually |

| Where to file | IRS with tax return | FinCEN (separate system) |

Common situation: Many Americans abroad must file FBAR but qualify for FATCA exemption due to the higher thresholds.

For a detailed comparison, read our FBAR vs Form 8938 guide.

What If I Don’t Qualify for an Exemption?

When your assets exceed thresholds and no exemptions apply, Form 8938 filing becomes mandatory. Non-compliance carries substantial penalties:

- $10,000 initial penalty per unfiled form

- Up to $50,000 additional penalties for continued failure after IRS notice

- 40% penalty on any tax understatement related to undisclosed assets

How to Catch Up Without Penalties

If you missed previous filings, the Streamlined Filing Procedures offer penalty relief for non-willful failures to file.

Qualification requirements:

- Your failure to file was unintentional (non-willful)

- You initiate the process before the IRS contacts you

- You file three years of returns and six years of FBARs

This program has helped thousands of Americans get back into compliance without facing the usual penalties.

Get Expert Help Determining Your Exemption Status

Determining whether you qualify for FATCA exemptions requires careful analysis of your specific assets, residency, and tax situation. Greenback Expat Tax Services helps Americans abroad work through these complex exemption rules.

Our team can:

- Determine if you qualify for FATCA exemptions

- Calculate your total specified foreign financial assets correctly

- Identify which assets need reporting and which are exempt

- Coordinate FATCA and FBAR requirements

- File Form 8938 when necessary

- Help you catch up through Streamlined Procedures if needed

Ready to get started? Click below to be matched with a Greenback accountant. For questions, contact our Customer Champions.

Frequently Asked Questions About FATCA Exemptions

Do I need a FATCA exemption code?

No. FATCA doesn’t use exemption codes. If you qualify for an exemption (through threshold amounts or asset types), you don’t file Form 8938. There’s no form to claim the exemption.

Who is exempt from FATCA reporting?

Individuals whose foreign assets stay below reporting thresholds are entirely exempt. Additionally, certain U.S. government employees abroad and residents of U.S. territories may qualify for special exemptions in specific situations.

Are foreign retirement accounts exempt from FATCA?

It depends. Foreign social security equivalents are exempt. Private foreign retirement plans may be exempt if reported on Forms 3520, 5471, or other specialized forms. However, they still count toward your threshold calculation.

What are the FATCA reporting thresholds?

Thresholds range from $50,000 to $75,000 for single filers in the U.S., up to $400,000 to $600,000 for married filers abroad. Staying below these amounts exempts you from filing. See the FATCA threshold details.

Is my foreign home exempt from FATCA?

Yes. Foreign real estate owned directly in your name is always exempt from FATCA reporting. However, property held through foreign entities requires reporting of the ownership of those entities.

Can I avoid FATCA if I already filed FBAR?

No. FBAR and FATCA are separate requirements with different rules. Filing one doesn’t exempt you from the other. You must evaluate each requirement independently based on your assets and circumstances.

What assets are exempt from FATCA reporting?

Physical cash, precious metals, directly-owned real estate, personal property, and foreign social security equivalents are exempt. Assets reported on Forms 5471, 8865, 3520, or 8621 are also exempt from Form 8938 (though they count toward thresholds).

How do joint accounts affect FATCA exemptions?

Joint accounts with non-US persons don’t create exemptions, but you only count your ownership share when calculating if you exceed thresholds. A $400,000 joint account with 50/50 ownership counts as $200,000 for your FATCA calculation.

Are there FATCA exemptions for small accounts?

There’s no per-account exemption. All foreign financial accounts count toward your total when determining if you exceed reporting thresholds, regardless of individual account size.

What if I’m just under the FATCA threshold?

If you stay below both the year-end AND maximum-during-year thresholds, you’re exempt from filing Form 8938. The thresholds are firm cutoffs with no filing required when you’re under them, even by $1.