FBAR vs. Form 8938: What’s the Difference and Do You Need to File Both?

- What's the Real Difference Between FBAR and FATCA?

- Do I Need to Comply with FBAR Only?

- Do I Need to Comply with FATCA Only?

- Do I Need to Comply with Both FBAR and FATCA?

- What Are the Critical Differences Between FBAR and FATCA?

- How Do I Know Which Requirement(s) I Need to Meet?

- What Happens If I've Already Missed These Requirements?

- What Are the Penalties for FBAR and FATCA Non-Compliance?

- Can I Reduce My U.S. Tax Bill Even If I Meet These Requirements?

- Frequently Asked Questions

- What Should I Do Next?

FBAR and FATCA are two separate U.S. reporting requirements for Americans with foreign financial accounts and assets. Both carry severe penalties for non-compliance, but they have different thresholds, cover different types of assets, and are filed through different systems. According to FinCEN, over 1.2 million FBARs are filed annually, yet many Americans abroad still don’t realize they may need to comply with both.

The FBAR (FinCEN Form 114) requires reporting when your foreign financial accounts exceed $10,000 in aggregate at any point during the year. FATCA (Form 8938) kicks in at higher thresholds and covers a broader range of assets beyond just accounts. The key distinctions are:

- FBAR: Foreign accounts only, $10,000 threshold, filed separately through FinCEN’s BSA E-Filing System

- FATCA: Foreign accounts plus stocks, partnerships, and other assets, $200,000+ threshold for expats abroad, filed with your tax return

- Many expats need both: Complying with one does not satisfy the other

Unsure If You Need to File FBAR, FATCA, or Both?

Here’s how to determine which requirement applies to you, what each one covers, and what happens if you’ve missed prior filings.

What’s the Real Difference Between FBAR and FATCA?

FBAR and FATCA are two distinct reporting requirements for U.S. citizens and residents with foreign financial assets. While they often overlap, they serve different purposes and have different rules.

- FBAR (Foreign Bank Account Report) focuses exclusively on foreign financial accounts you have an interest in or authority over. You report FBAR by filing FinCEN Form 114.

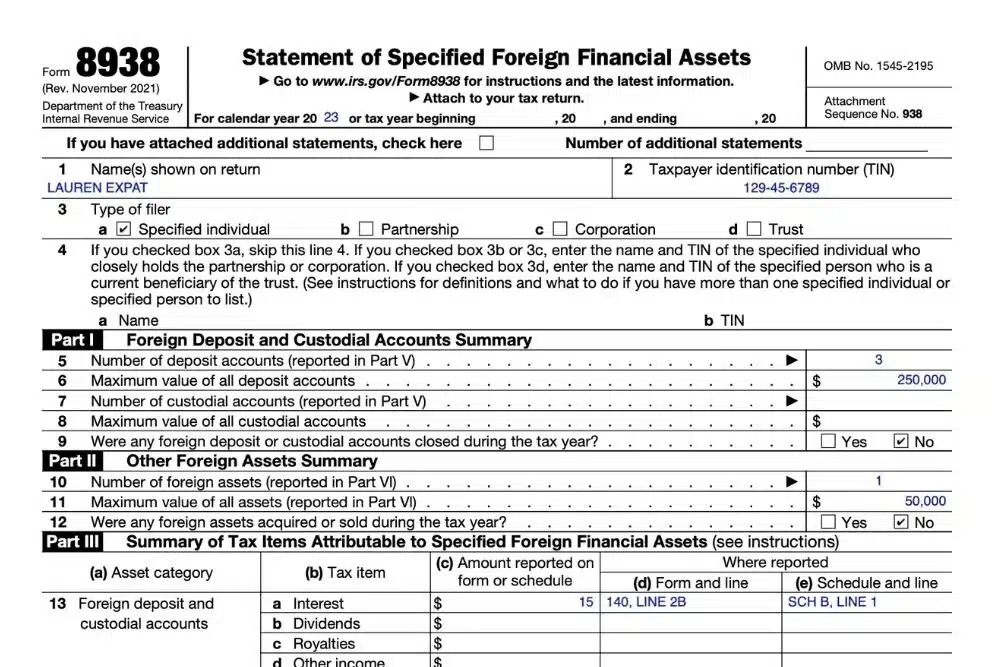

- FATCA (Foreign Account Tax Compliance Act) covers a broader range of foreign financial assets beyond just accounts. FATCA, the Foreign Account Tax Compliance Act, is a U.S. law requiring both foreign financial institutions and U.S. persons to report offshore assets. For a full explanation of what FATCA requires and who it applies to, see our FATCA overview. You comply with FATCA by filing Form 8938 with your tax return.

Here’s the essential difference: FBAR catches foreign accounts. FATCA catches foreign accounts AND other foreign assets like stocks, partnerships, and investments held outside accounts.

| Comparison Point | FBAR | FATCA |

| What you report | Foreign financial accounts only | Foreign financial accounts AND other foreign assets |

| Filing form | FinCEN Form 114 | Form 8938 |

| Who receives it | FinCEN (Treasury Department) | IRS (with your tax return) |

| Threshold | $10,000 aggregate at any time | $50,000-$600,000 depending on status |

| Where filed | BSA E-Filing System (separate) | Attached to Form 1040 |

| Deadline | April 15 (auto-extension to October 15) | April 15 (auto-extension to October 15) |

| Penalties | Up to $16,536 per non-willful violation | $10,000 initial, up to $50,000 continued |

Do I Need to Comply with FBAR Only?

You’ll need FBAR compliance, but not FATCA, when your foreign accounts exceed $10,000, but your total foreign assets stay below the FATCA threshold.

Example: Digital nomad with basic banking

Marcus is single and travels full-time. He has $35,000 in a Thai bank account and $15,000 in a Mexican account. His total foreign accounts ($50,000) exceed the FBAR threshold but fall below the $200,000 FATCA threshold for single expats abroad.

Marcus needs: FBAR only.

Example: Married couple with modest savings

Jennifer and Tom reside in Spain and file their taxes jointly. They have €45,000 ($49,000 USD) in a Spanish savings account. This exceeds the $10,000 FBAR threshold but stays well below the $400,000 FATCA threshold for married expats filing jointly abroad.

Jennifer and Tom need: FBAR only.

Do I Need to Comply with FATCA Only?

You’ll need FATCA compliance, but not FBAR, when you have specified foreign financial assets that aren’t foreign accounts, or when your foreign assets exceed FATCA thresholds, but you never had $10,000 in foreign accounts.

Example: Stock investor living in the U.S.

Rachel lives in California and directly owns shares in a German company (not held in any brokerage account) worth $85,000. She has no foreign bank accounts. She exceeds the $50,000 FATCA threshold for U.S. residents but doesn’t meet the $10,000 FBAR threshold because she has no foreign accounts.

Rachel needs: FATCA only.

This scenario is relatively rare. Most expats who exceed FATCA thresholds also have foreign bank accounts that trigger FBAR requirements.

Do I Need to Comply with Both FBAR and FATCA?

This is the most common situation for expats with substantial foreign holdings. You’ll need both when your foreign accounts exceed $10,000, AND your total foreign assets exceed the FATCA threshold.

Example: Corporate expat with comprehensive finances

Sarah is single and works in London. She has:

- £120,000 in a UK bank account ($156,000 USD)

- £80,000 in a UK investment account ($104,000 USD)

- Company stock options worth $55,000

Her total foreign assets ($315,000) exceed both the $10,000 FBAR threshold and the $200,000 FATCA threshold for single expats abroad.

Sarah needs: Both FBAR and FATCA compliance.

Example: Retired couple with foreign pension

David and Linda retired to Portugal and filed jointly. They have:

- €180,000 in Portuguese bank accounts ($196,000 USD)

- €220,000 in a Portuguese private pension ($240,000 USD)

Their total foreign assets ($436,000) exceed both the $10,000 FBAR threshold and the $400,000 FATCA threshold for married expats filing jointly abroad.

David and Linda need to comply with both FBAR and FATCA.

Although some assets must be reported under both requirements, you must file both forms separately. Complying with one doesn’t exempt you from the other.

What Are the Critical Differences Between FBAR and FATCA?

Assets Covered: Accounts vs. Broader Assets

FBAR only reports foreign financial accounts, including checking, savings, and investment accounts, as well as certain pensions and life insurance policies.

FATCA reports all specified foreign financial assets, including:

- Everything FBAR covers, plus

- Foreign stocks and securities held directly (not in an account)

- Foreign partnership interests

- Foreign hedge fund and private equity fund interests

- Foreign options and derivatives

- Beneficial interests in foreign trusts

Why this matters: You might have foreign stocks purchased directly from a company that needs FATCA reporting but not FBAR reporting.

Signature Authority: A Key FBAR Distinction

FBAR requires reporting accounts where you have signature authority, even if you don’t own them. This commonly affects:

- Business owners who can sign on the company’s foreign accounts

- Employees with signing authority on employer accounts

- Adult children who can sign on to their elderly parents’ accounts

- Executors managing estate accounts

FATCA only requires reporting assets you own or have an interest in, not accounts where you merely have signature authority.

Example:

Maria works for a U.S. company with a German subsidiary. She can sign on the subsidiary’s German bank account (with a €200,000 balance), but she has no ownership interest. She also has her personal German account with €8,000.

Maria’s requirements: FBAR (reports both the company account and her personal account, totaling over $10,000). No FATCA (she doesn’t own the company account, and her personal assets are below the threshold).

Thresholds: Fixed vs. Variable

Form 8938 thresholds vary based on where you live and your filing status, ranging from $50,000 for U.S.-based single filers to $600,000 for Americans living abroad who are married. FBAR has a single fixed threshold: $10,000 combined across all foreign accounts at any point during the year — no exceptions for filing status or location.

For the complete Form 8938 threshold table broken out by residency and filing status, see our Form 8938 filing thresholds guide.

Filing Location: Separate Systems

This is where many expats make mistakes. FBAR and FATCA go to entirely different places:

- FBAR: Filed electronically through the BSA E-Filing System at fincen.gov. It’s never attached to your tax return. FinCEN (Financial Crimes Enforcement Network) receives it, not the IRS.

- FATCA: Filed as Form 8938 attached to your regular tax return (Form 1040) with the IRS. If you e-file your return, FATCA reporting is included electronically. If you have a paper file, it’s physically attached.

What this means: Even if you file FATCA reporting with your tax return, you still need to file the FBAR online through FinCEN if you meet that requirement separately. They don’t communicate with each other.

How Do I Know Which Requirement(s) I Need to Meet?

Use this decision tree to determine your requirements:

Step 1: Did your foreign financial accounts exceed $10,000 in aggregate at ANY point during the year?

- Yes → You need FBAR. Continue to Step 2.

- No → No FBAR required. Continue to Step 2.

Step 2: Are you required to file a U.S. tax return?

- Yes → Continue to Step 3.

- No → No FATCA required (even if your assets exceed thresholds). Stop here.

Step 3: What’s your filing status, and where do you live?

- Single, abroad: Assets exceed $200,000 year-end OR $300,000 anytime? → Need FATCA

- Single, U.S: Assets exceed $50,000 year-end OR $75,000 anytime? → Need FATCA

- Married filing jointly, abroad: Assets exceed $400,000 year-end OR $600,000 anytime? → Need FATCA

- Married filing jointly, U.S: Assets exceed $100,000 year-end OR $150,000 anytime? → Need FATCA

Your result: You now know if you need FBAR only, FATCA only, both, or neither.

What Happens If I’ve Already Missed These Requirements?

If you realize you should have been complying with FBAR or FATCA in previous years, relief programs are available. The approach depends on your specific situation:

For late FBAR only: The Delinquent FBAR Submission Procedures may eliminate penalties if your tax returns are current and your failure was non-willful.

For both late tax returns and FBAR/FATCA: The Streamlined Filing Compliance Procedures allow you to catch up with reduced or eliminated penalties. This program was specifically designed for expats who were unfamiliar with their filing requirements.

Don’t attempt to “quietly” file past forms without using these procedures. The IRS and FinCEN coordinate data, and filing late without protection can trigger audits and full penalties.

What Are the Penalties for FBAR and FATCA Non-Compliance?

Both requirements carry severe penalties, but the penalty structures differ significantly.

FBAR penalties can be assessed per account or per form, depending on whether the violation was willful. Non-willful violations can result in a penalty of up to $16,536 per violation (2025 amount). Willful violations can result in the greater of $165,353 or 50% of the account balance per account. Criminal penalties may also apply.

FATCA penalties start at $10,000 for failure to file. If you don’t file within 90 days of receiving IRS notification, you will face an additional $10,000 per month, up to a maximum of $50,000. There’s also a 40% penalty on any underpayment of tax related to undisclosed foreign assets.

Can I Reduce My U.S. Tax Bill Even If I Meet These Requirements?

Yes! The good news is that FBAR and FATCA compliance doesn’t mean you’ll owe U.S. taxes. These are purely informational requirements. Most expats can eliminate or automatically reduce their U.S. tax liability using:

- The Foreign Earned Income Exclusion (FEIE): Excludes up to $130,000 of earned income from U.S. taxation (2025 tax year). This is ideal for expats in low-tax countries such as the UAE, Singapore, or Portugal.

- The Foreign Tax Credit (FTC): Provides a dollar-for-dollar credit for foreign taxes paid. This works best for expats in high-tax countries like Germany, France, or the UK.

Many expats use these benefits to reduce their U.S. tax bill to $0 while still meeting all reporting requirements for FBAR and FATCA.

Frequently Asked Questions

Yes. FBAR and FATCA are independent requirements with separate thresholds. If your foreign accounts exceed $10,000 but your total foreign assets fall below the FATCA threshold for your filing status (for example, under $200,000 for single expats abroad), you only need to file FBAR. You do not need to file Form 8938.

No. Even though both forms report similar information, they are routed to different agencies via different systems. FATCA (Form 8938) goes to the IRS with your tax return. FBAR (FinCEN Form 114) is filed with FinCEN through the BSA E-Filing System. You must file both separately if you meet both thresholds.

In most cases, yes. Foreign pension accounts, provident funds (like Singapore’s CPF), and similar retirement savings vehicles generally count as foreign financial accounts for FBAR purposes and as specified foreign financial assets for FATCA purposes. The rules can vary depending on the structure of the account and the country, so consult a tax professional if you’re unsure whether a specific foreign retirement account triggers either requirement.

You still need to file FBAR. The $10,000 FBAR threshold is based on the maximum aggregate value of all your foreign accounts at any point during the year, even if the balance exceeded $10,000 for just one day. A common trigger is receiving a large deposit (like a paycheck or tax refund) that temporarily pushes your combined balances over the threshold.

Yes, penalties for FBAR and FATCA non-compliance apply regardless of whether you owe U.S. taxes. These are informational reporting requirements, not tax payments. However, the IRS offers relief through the Streamlined Foreign Offshore Procedures, which can eliminate penalties for expats who were non-willfully non-compliant. The sooner you catch up, the better your position.

What Should I Do Next?

The distinction between FBAR and FATCA compliance trips up even sophisticated investors. Here’s what you should do:

- Calculate carefully: Review your foreign account statements for the entire year. The FBAR threshold applies if you exceeded $10,000 for even one day.

- Include everything reportable: Don’t forget to include signature authority accounts for FBAR and non-account assets for FATCA.

- Use the correct exchange rate: convert the December 31 currency to USD using the Treasury’s exchange rate as of that date.

- File separately: Please note that FBAR and FATCA are submitted to different agencies through separate systems.

Need help determining your filing requirements? Contact us, and one of our Customer Champions will be happy to help. Ready to be matched with a Greenback accountant? Click the get started button below.

Stay Compliant With FBAR and FATCA Reporting

The information provided here is for general guidance only. Foreign account reporting requirements can be complex and vary based on individual circumstances. For specific advice on your situation, consult with a qualified tax professional.