IRS Form 1099-DA: Digital Asset Proceeds Reported by Your Crypto Broker

- What Is IRS Form 1099-DA?

- Who Receives a Form 1099-DA?

- What Information Does Form 1099-DA Report?

- What Is the Difference Between Covered and Noncovered Digital Assets?

- How Does Form 1099-DA Change the Way You File Your Tax Return?

- What Transition Relief Has the IRS Provided for 1099-DA Reporting?

- Do Expats Have Additional Reporting Obligations for Digital Assets?

- What Should You Do Now to Prepare for Form 1099-DA?

- Frequently Asked Questions

- Related Resources

If you sold cryptocurrency, NFTs, or other digital assets through a custodial exchange in 2025, you may receive a new IRS form this year. Form 1099-DA requires brokers to report the gross proceeds of your digital asset transactions directly to the IRS, starting with sales made on or after January 1, 2025. The IRS finalized these reporting rules under regulations TD 9989, bringing crypto reporting in line with traditional securities reporting on Form 1099-B.

- Gross proceeds reporting began for transactions on or after January 1, 2025

- Cost basis reporting begins for covered digital assets acquired on or after January 1, 2026

- Transition relief under IRS Notice 2025-33 waives penalties for brokers making a good-faith effort to file correctly

- Backup withholding relief extends through 2026, with additional TIN-matching provisions for 2027

Your Broker Is Now Reporting Your Crypto to the IRS. Are You Ready?

This guide covers who receives a Form 1099-DA, what the form reports, how it affects your filing, and what expats with digital assets need to do to stay compliant.

What Is IRS Form 1099-DA?

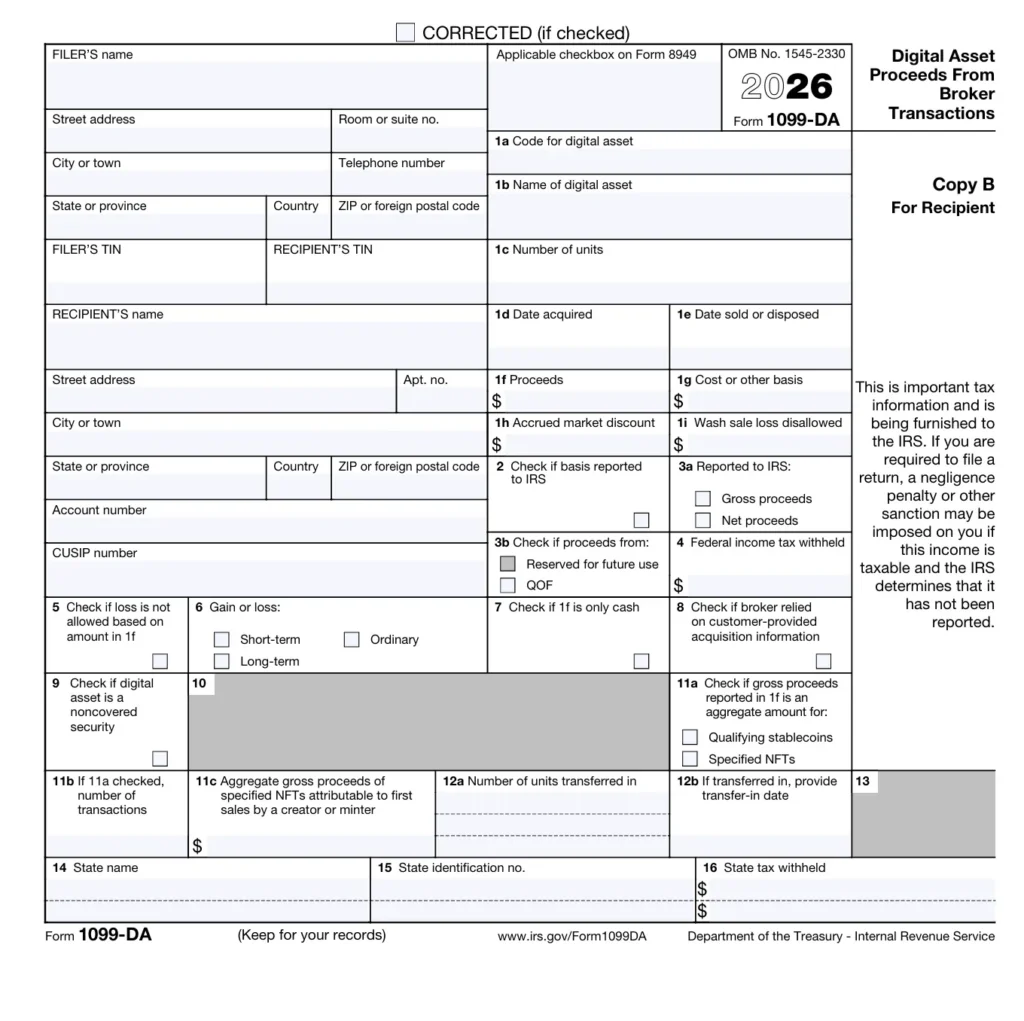

Form 1099-DA, titled “Digital Asset Proceeds From Broker Transactions,” is the IRS information return that custodial brokers use to report the proceeds from your cryptocurrency and digital asset sales to both you and the IRS. It works much like the Form 1099-B you might receive from a stock brokerage, except it applies specifically to digital assets such as Bitcoin, Ethereum, stablecoins, and NFTs.

The form was created as part of the Infrastructure Investment and Jobs Act of 2021, which expanded the definition of “broker” to include custodial digital asset trading platforms, hosted wallet providers, digital asset kiosks (like Bitcoin ATMs), and certain processors of digital asset payments (PDAPs). If you used a centralized exchange such as Coinbase, Kraken, Gemini, or Fidelity Crypto to make trades in 2025, that exchange is required to file a Form 1099-DA with the IRS and send you a copy.

For the 2025 tax year, brokers report gross proceeds only. Starting with transactions made on or after January 1, 2026, brokers must also report cost basis for covered digital assets (those acquired and held within the same broker account). This phased approach gives both brokers and taxpayers time to adapt to the new reporting framework.

Who Receives a Form 1099-DA?

You will receive a Form 1099-DA if you sold, exchanged, or disposed of digital assets through a custodial broker during the 2025 tax year. This includes trades made on any centralized exchange where the platform takes custody of your assets.

Brokers were required to furnish you with a copy by February 17, 2026. However, many exchanges have experienced delays, and the IRS has confirmed it will not penalize brokers for late filing during this first year, provided they are making a good-faith effort.

Who Will Not Receive a 1099-DA

Not every digital asset transaction triggers a Form 1099-DA. You will not receive one if you only held digital assets without selling or exchanging them, transacted exclusively through decentralized platforms (DEXs) or non-custodial wallets, or transferred digital assets between your own wallets without a sale or exchange. Even if you do not receive a Form 1099-DA, you are still required to report all taxable digital asset transactions on your return. The IRS uses the digital asset question on Form 1040 to flag filers who may have unreported crypto activity.

What Information Does Form 1099-DA Report?

Form 1099-DA collects transaction-level data similar to what you would see on a Form 1099-B for stock sales. For the 2025 tax year, brokers are required to report only gross proceeds. Cost basis reporting begins with transactions made on or after January 1, 2026.

Here is a breakdown of the key fields on the form:

| Box | Field | What It Reports |

|---|---|---|

| Box 1a | Description of property | Type of digital asset (e.g., 0.5 BTC) |

| Box 1b | Date acquired | Date you originally acquired the asset (if known) |

| Box 1c | Date of sale or disposition | Date the transaction occurred |

| Box 1f | Gross proceeds | Total value received from the sale |

| Box 1g | Cost or other basis | Your adjusted cost basis (blank for 2025 transactions) |

| Box 5 | Transaction type | Whether the transaction was a sale, exchange, or other disposition |

| Box 9 | Noncovered security | Checked if the broker is not required to report basis |

For the 2025 tax year, expect Box 1g (cost basis) to be blank in most cases. Brokers are not required to report the basis for transactions made before January 1, 2026. You will need to determine your own cost basis using your personal records.

What Is the Difference Between Covered and Noncovered Digital Assets?

This distinction matters for how much information your broker reports to the IRS and how much recordkeeping falls on you.

- A covered digital asset is one acquired on or after January 1, 2026, in an account where the broker provides custodial services. For covered assets, your broker must report both gross proceeds and adjusted cost basis to the IRS on Form 1099-DA.

- A noncovered digital asset is one acquired before January 1, 2026, or transferred into a broker account from an external wallet. For non-covered assets, the broker is only required to report gross proceeds. Box 9 on your Form 1099-DA will be checked, and Box 1g will likely be blank.

| Category | Acquired | Broker Reports | Your Responsibility |

|---|---|---|---|

| Covered | On or after Jan. 1, 2026, in the same broker account | Gross proceeds and cost basis | Verify accuracy |

| Noncovered | Before Jan. 1, 2026, or transferred from an external wallet | Gross proceeds only | Calculate and report your own cost basis |

If you have been buying crypto across multiple exchanges or wallets over several years, most of your 2025 holdings are non-covered. This means the burden of tracking and reporting cost basis is on you.

How Does Form 1099-DA Change the Way You File Your Tax Return?

The introduction of Form 1099-DA does not change your underlying tax obligations. You have always been required to report digital asset gains and losses. What changes is the information flow: the IRS now receives the same gross proceeds data your broker sends you, making it easier for the IRS to flag discrepancies.

When you file your return, you still report digital asset transactions on Form 8949 and carry the totals to Schedule D. The data from your Form 1099-DA feeds directly into Form 8949.

Here is the general reporting flow:

- Receive your Form 1099-DA from each broker you used

- Reconcile the gross proceeds with your own records

- Determine your cost basis for each transaction (especially for non-covered assets)

- Report each transaction on Form 8949, categorized by short-term or long-term holding period

- Transfer the totals to Schedule D of your Form 1040

- Answer “Yes” to the digital asset question on your Form 1040

If you are living abroad, the reporting process is the same, but you may need to consider additional factors. Crypto held on foreign exchanges may also trigger FBAR reporting if the aggregate value of your foreign financial accounts exceeds $10,000 at any point during the year. Depending on your total foreign financial asset values, you may also need to file Form 8938 under FATCA.

What Transition Relief Has the IRS Provided for 1099-DA Reporting?

The IRS recognizes that Form 1099-DA is brand new, and both brokers and taxpayers need time to adjust. Several relief provisions are in place:

- Penalty relief for 2025 filings: Under IRS Notice 2024-56 and extended by Notice 2025-33, the IRS will not impose penalties on brokers for incorrect or late Forms 1099-DA filed for the 2025 tax year, as long as the broker made a good-faith effort to comply.

- Backup withholding relief: Normally, brokers must withhold 24% of proceeds if a taxpayer fails to provide a valid TIN. Notice 2025-33 extends relief from backup withholding liability for digital asset transactions through 2026. For 2027, brokers can avoid withholding requirements if they verify your name and TIN through the IRS TIN Matching Program.

- Digital asset identification relief: The IRS has also extended temporary relief, allowing taxpayers to use their own books and records to identify which specific units of broker-held digital assets they sold. This relief, which was set to expire January 1, 2026, has been extended through December 31, 2026.

Do Expats Have Additional Reporting Obligations for Digital Assets?

Yes. If you are a U.S. citizen or Green Card holder living abroad, your worldwide income is subject to U.S. taxation regardless of where you live or where your exchange is based. This means your digital asset transactions are reportable even if you traded on a non-U.S. platform.

Beyond the standard Form 8949 and Schedule D reporting, expats with digital assets should be aware of several additional requirements:

- FBAR (FinCEN Form 114): If you hold crypto on a foreign exchange and the aggregate value of all your foreign financial accounts exceeds $10,000 at any point during the year, you must file an FBAR. The IRS and FinCEN have indicated that cryptocurrency held on foreign exchanges may qualify as a reportable foreign financial account.

- FATCA (Form 8938): If your foreign financial assets exceed certain thresholds (ranging from $50,000 to $600,000 depending on your filing status and whether you live in the U.S. or abroad), you may need to file Form 8938. Digital assets held on foreign platforms may count toward these thresholds.

- Capital gains treatment: Your crypto gains are taxed as capital gains, with the rate depending on how long you held the asset. Short-term gains (held one year or less) are taxed at ordinary income rates, while long-term gains (held more than one year) are taxed at preferential rates of 0%, 15%, or 20%.

For a deeper look at how crypto is taxed for Americans abroad, see our cryptocurrency tax guide for expats.

What Should You Do Now to Prepare for Form 1099-DA?

Whether you have already received a Form 1099-DA or are still waiting, here are the steps you should take:

- Gather your records: Collect transaction histories from every exchange and wallet you used during the tax year. Because cost basis is not reported for 2025 transactions, you will need your own purchase records to accurately calculate gains and losses.

- Reconcile your 1099-DA: Compare the gross proceeds on your Form 1099-DA with your own records. Discrepancies can occur if the broker used a different valuation method, missed transactions, or reported transfers as sales.

- Check the digital asset question: Make sure you answer “Yes” to the digital asset question on Form 1040 if you sold, exchanged, received, or otherwise disposed of digital assets during the year.

- Review your foreign account obligations: If you held crypto on a foreign exchange, determine whether you need to file an FBAR or Form 8938.

- Get professional help if needed: Digital asset reporting is one of the most error-prone areas of tax filing, especially for expats managing transactions across multiple exchanges and countries. Working with a tax professional who handles both expat taxes and crypto reporting can save you from costly mistakes.

If you are a U.S. citizen or Green Card holder with crypto investments, you do not have to figure this out alone. Our team works with expats every day to report digital asset income correctly, claim all available benefits, and keep you in good standing with the IRS.

Crypto Reporting Just Got More Visible. Your Return Should Reflect That.

Frequently Asked Questions

Yes. Even if your broker did not send you a Form 1099-DA, you are required to report all taxable digital asset transactions on your tax return. This applies whether you traded on a decentralized exchange, used a non-custodial wallet, or simply did not receive the form due to broker delays. The IRS expects you to track and report your own transactions using your personal records. If you have unreported crypto from prior years, the Streamlined Procedures may be an option.

No. For the 2025 tax year, brokers are only required to report gross proceeds. Cost basis reporting begins with transactions made on or after January 1, 2026. For any digital assets you sold in 2025, you will need to calculate your own cost basis using purchase records from your exchanges and wallets.

Yes. Each custodial broker you traded through during the tax year is required to file its own Form 1099-DA with the IRS and send you a copy. If you used three different exchanges, you should expect three separate forms. You will need to consolidate all of them when reporting on Form 8949.

No. Moving digital assets between wallets you own is not a taxable event and should not be reported on a Form 1099-DA. However, some brokers may struggle to distinguish transfers from sales, leading to incorrect reporting. Always reconcile your 1099-DA against your own records.

It depends on the tax laws of your country of residence. As a U.S. citizen or Green Card holder, your worldwide income, including crypto gains, is always reportable to the IRS. Many countries also tax crypto transactions under their own rules. If you pay foreign tax on your crypto gains, you may be able to claim a credit on your U.S. return to avoid double taxation. See our cryptocurrency tax guide for expats for more details.

The IRS and FinCEN have indicated that cryptocurrency held on foreign exchanges may qualify as a reportable foreign financial account. If the aggregate value of all your foreign financial accounts, including crypto accounts, exceeds $10,000 at any point during the year, you should file an FBAR. Depending on the total value of your foreign assets, you may also need to file Form 8938.

Tax rules and regulations change, and this information may not reflect the most current legislation. Please consult a qualified tax professional for advice specific to your situation. This article is intended for informational purposes only and should not be taken as tax, legal, or financial advice.

Related Resources

- How Is Cryptocurrency Taxed for U.S. Expats Abroad?

- Virtual Currency on Form 1040: Digital Asset Checkbox Guide

- IRS Extends Crypto Identification Relief for Brokers

- Form 8949 for U.S. Expats: Report Foreign Capital Gains

- Schedule D: Capital Gains and Losses for Expats

- FBAR for Expats: Who Must File, Deadlines, and Penalties

- FATCA for U.S. Expats

- Form 8938 for Expats

- 1099 Forms for U.S. Expats Explained

- U.S. Expat Taxes: Filing Guide for Americans Abroad