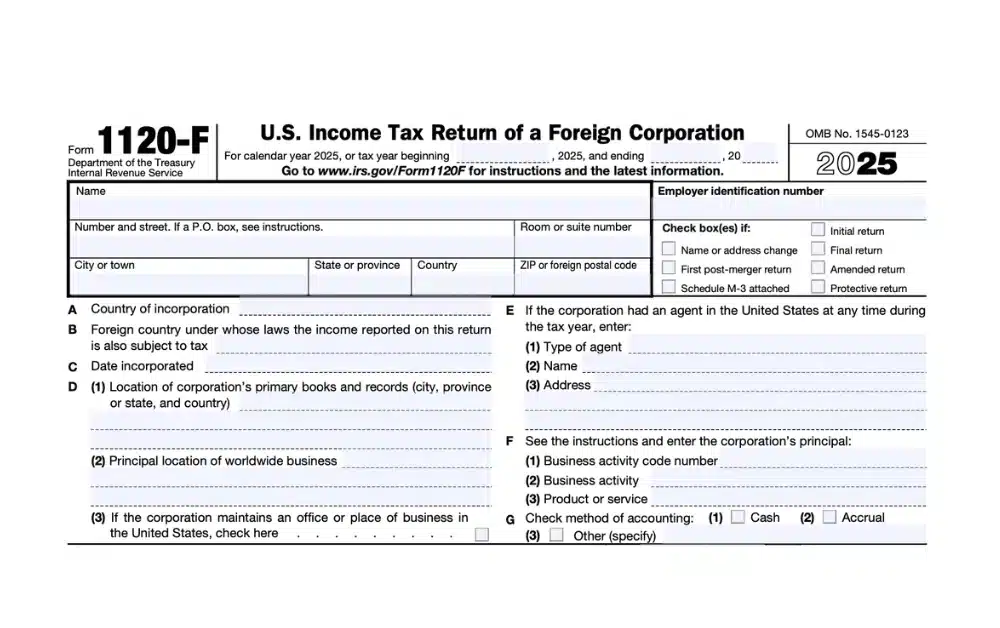

Form 1120-F Explained: U.S. Tax Return for Foreign Corporations

If your foreign corporation earns income connected to a U.S. trade or business, or receives certain types of U.S.-source income, it likely needs to file Form 1120-F. This is the U.S. income tax return for foreign corporations, and the IRS requires it even if no tax is owed.

According to the IRS, a foreign corporation must file Form 1120-F if it was engaged in a trade or business in the United States at any time during the tax year, or had U.S.-source income that was not fully covered by withholding. Common situations that trigger a Form 1120-F filing requirement include:

- Effectively connected income (ECI) from a U.S. office, warehouse, or employee

- U.S.-source income such as interest, dividends, rents, or royalties not fully withheld at source

- Treaty benefit claims that require disclosure on Form 8833

- Refund claims for overpaid U.S. taxes during the year

Unsure If Your Foreign Corporation Has a U.S. Filing Obligation?

Here’s what you need to know about Form 1120-F and why getting it filed correctly is critical for protecting your corporation’s ability to claim deductions and credits.

How Is Form 1120-F Different From Form 1120?

The distinction is straightforward: Form 1120 is filed by domestic U.S. corporations. Form 1120-F is filed by foreign corporations (those incorporated outside the United States) that have U.S. tax obligations.

| Feature | Form 1120 | Form 1120-F |

|---|---|---|

| Who files | Domestic U.S. corporations | Foreign corporations with U.S. income |

| Income reported | Worldwide income | Only U.S.-source and effectively connected income |

| Tax rate | Flat 21% on all taxable income | 21% on ECI; 30% (or treaty rate) withholding on passive U.S. income |

| Deadline (with U.S. office) | April 15 | April 15 |

| Deadline (no U.S. office) | N/A | June 15 |

| Extension | 6 months (Form 7004) | 6 months (Form 7004) |

Other variants in the 1120 family include Form 1120-S for S corporations, Form 1120-L for life insurance companies, Form 1120-REIT for real estate investment trusts, and Form 1120-C for cooperative associations. Each is tailored to a specific entity type.

Who Must File Form 1120-F?

A foreign corporation must file Form 1120-F if any of the following apply during the tax year:

- The corporation was engaged in a U.S. trade or business: This generally means the corporation had a physical presence in the U.S., such as an office, employees, a warehouse, or a dependent agent acting on its behalf. Income earned through this presence is called “effectively connected income” (ECI) and is taxed at the standard 21% corporate rate after deductions.

- The corporation had U.S.-source income not subject to full withholding: Even without a U.S. presence, income like interest, dividends, rents, and royalties from U.S. sources may trigger a filing requirement if U.S. withholding tax was not properly applied at source.

- The corporation is claiming a treaty benefit: If the foreign corporation is relying on an income tax treaty to reduce or eliminate U.S. tax, Form 1120-F must be filed along with Form 8833 to disclose the treaty position.

- The corporation overpaid U.S. taxes and is claiming a refund: If withholding at source resulted in more tax being collected than is owed, Form 1120-F is the mechanism for claiming that refund.

The concept of “effectively connected income” is one of the most complex areas of U.S. international tax. Whether your foreign corporation’s activities rise to the level of a U.S. trade or business depends on factors like the type of activity, frequency, regularity, and where key decisions are made. This determination has significant tax consequences, and getting it wrong can be costly. We strongly recommend working with a tax specialist on this analysis.

Why Is Protective Filing Important?

Even if you believe your foreign corporation is not required to file Form 1120-F, there is a strong strategic reason to file anyway. This is called a “protective return.”

Here’s why it matters: if the IRS later determines that your foreign corporation did have effectively connected income, the corporation can only claim deductions and credits against that income if Form 1120-F was timely filed. Filing a protective return preserves your right to those deductions and credits, even if the return itself shows zero taxable income.

The IRS generally considers Form 1120-F to be timely filed if it is submitted no later than 18 months after the original due date. However, filing proactively eliminates the risk entirely.

A protective return is essentially an insurance policy. It costs relatively little to prepare but can save your corporation significant money if the IRS ever reclassifies your income as effectively connected.

When Is Form 1120-F Due?

The filing deadline depends on whether your foreign corporation has a U.S. office or place of business:

| Situation | Deadline | Extended Deadline |

|---|---|---|

| Foreign corporation with a U.S. office or place of business | April 15, 2026 | October 15, 2026 |

| Foreign corporation without a U.S. office or place of business | June 15, 2026 | December 15, 2026 |

In either case, you can request an automatic six-month extension by filing Form 7004 by the original due date.

An extension to file is not an extension to pay. If your foreign corporation owes U.S. tax, the payment is still due by the original deadline to avoid interest and penalties.

What Are the Penalties for Not Filing?

The IRS takes Form 1120-F compliance seriously. Penalties for late filing start at 5% of the unpaid tax per month, up to a maximum of 25%. For returns filed more than 60 days late, the minimum penalty for tax years filed in 2026 is the lesser of the tax due or $525.

Beyond monetary penalties, the most significant risk of not filing is losing the right to claim deductions and credits. Without a timely Form 1120-F on record, the IRS can tax your effectively connected income at the gross amount, with no offsets for business expenses. For corporations with substantial U.S. operations, this can result in dramatically higher tax bills.

What Makes Form 1120-F So Complex?

Form 1120-F is eight pages long, with multiple sections covering different types of income and tax calculations. The IRS estimates it takes more than 70 hours to complete. Key areas of complexity include:

- Income classification: The form requires you to separate income into three distinct sections: U.S.-source income not effectively connected with a U.S. trade or business (Section I), effectively connected income (Section II), and branch profits tax calculations (Section III). Each section has different tax rates and rules.

- Branch profits tax: In addition to regular corporate income tax on ECI, foreign corporations may owe a 30% branch profits tax (or a reduced treaty rate) on earnings that are deemed repatriated to the home country. This is calculated in Section III of Form 1120-F and functions similarly to a dividend withholding tax.

- Treaty coordination: If your corporation is claiming treaty benefits, you must properly disclose treaty positions using Form 8833 and ensure the treaty provisions are applied correctly across multiple income categories.

- Additional reporting: Foreign corporations with U.S. operations may also need to file Form 5472 (for reportable transactions with related parties), FBAR (for foreign bank accounts), and various information returns depending on the corporate structure. If the foreign corporation owns U.S. subsidiaries or is part of a controlled foreign corporation structure, the reporting obligations increase further.

Can I E-file Form 1120-F?

Yes. Most foreign corporations can file Form 1120-F electronically, along with related forms, schedules, and attachments. In some cases, e-filing is mandatory. Corporations with total assets of $10 million or more that file at least 250 returns per year are generally required to e-file, though waivers may be available.

Let Greenback Handle Your Form 1120-F

Form 1120-F sits at the intersection of U.S. corporate tax law and international tax provisions, making it one of the most complex returns in the tax code. Between ECI classification, branch profits tax, treaty coordination, and protective filing strategy, the stakes are high and the margin for error is small.

Greenback’s CPAs and Enrolled Agents specialize in international business tax reporting for Americans abroad. We handle Form 1120-F, Form 1118 (Foreign Tax Credit for corporations), GILTI calculations, and the full range of corporate reporting requirements for foreign entities with U.S. tax obligations.

No matter how late, messy, or complex your return may be, we can help. You’ll have peace of mind, knowing that your taxes were done right.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on taxes or working with Greenback, contact us, and one of our Customer Champions will happily address all your concerns.

Foreign Corporations With U.S. Activity Must Take Form 1120-F Seriously

This article is intended for informational purposes only and does not constitute legal or tax advice. While Greenback makes every effort to ensure the information is accurate and up-to-date, every tax situation is unique. For advice tailored to your specific situation, consult one of our expat tax professionals.

Related Resources

- Form 1120: Does My Corporation Need to File?

- Form 1118: Claiming the Foreign Tax Credit for Corporations

- Foreign Tax Credit: How Expats Can Reduce U.S. Taxes

- What Is a Controlled Foreign Corporation (CFC)?

- What Is GILTI? Guide for Expat Business Owners

- Form 5472: Who Must File and How to Avoid $25,000+ Penalties

- What Tax Forms Do I Need to File for My Foreign Business?

- FBAR: What It Is, Who Must File, and How to Report Foreign Accounts

- Form 4868 for U.S. Expats: Extension Filing Explained

- Small Business Tax Return Preparation for U.S. Expats