Form 8621 for Expats Explained: PFIC Reporting for Foreign Mutual Funds

- Who Needs to File Form 8621?

- How Do Most Expats End Up Filing Form 8621?

- What Does Form 8621 Look Like?

- Why Is Form 8621 So Difficult to File?

- What Happens If I Do Not File Form 8621?

- What Other Forms Do I Need Alongside Form 8621?

- What If I Am Behind on Form 8621 Filings?

- Do I Need to File Form 8621 Every Year?

- What Is the Difference Between FBAR and Form 8621?

- How Greenback Handles Form 8621

- Related Resources

Form 8621 is the IRS information return you file when you own shares in a Passive Foreign Investment Company (PFIC) or Qualified Electing Fund (QEF). According to the IRS, you must file a separate Form 8621 for each PFIC you own, whether you received distributions or not. For most Americans living abroad, this means a separate form for each foreign mutual fund, ETF, or REIT in your portfolio.

If your combined PFIC holdings are small, you may qualify for simplified reporting:

- Single or married filing separately: Year-end value of all PFICs under $25,000

- Married filing jointly: Year-end value of all PFICs under $50,000

- Any distribution or sale: Must file regardless of value

Own Foreign Mutual Funds or ETFs? Don’t Guess on Form 8621.

The form is notoriously complex, and mistakes can be costly. This is one of the areas where professional help makes the biggest difference. Here is what the form requires, why it matters, and what happens if you get it wrong.

Who Needs to File Form 8621?

You must file Form 8621 if you are a U.S. person (citizen, green card holder, or resident alien) who is a direct or indirect shareholder of a PFIC. The IRS defines this broadly. You are considered a shareholder if you:

- Own PFIC shares directly in a foreign brokerage or investment account

- Own PFIC shares through a pass-through entity such as a partnership, S-corp, trust, or estate

- Own shares in a PFIC that itself owns another PFIC (creating a chain of ownership requiring multiple forms)

- Own 50% or more of a foreign corporation that is not a PFIC but that owns shares in a PFIC

The most common trigger for Americans abroad is investing in local funds. That foreign mutual fund your UK financial advisor recommended, the unit trust your Australian broker set up, or the ETF you bought on the Toronto Stock Exchange are almost certainly PFICs. Even some foreign pension funds and insurance products with investment components can qualify.

For a detailed breakdown of what qualifies as a PFIC and how the IRS classifies foreign investments, see our complete PFIC tax rules guide.

How Do Most Expats End Up Filing Form 8621?

Most Americans abroad do not set out to invest in PFICs. They open a local investment account, follow the advice of a local financial advisor, or participate in an employer-sponsored savings plan. Then, at tax time, they discover that their perfectly normal foreign investments trigger one of the most complex forms in the U.S. tax code.

Common scenarios that require Form 8621:

| How You Got the PFIC | Example | Forms Needed |

|---|---|---|

| Local financial advisor recommendation | British ISA holding foreign funds, Australian superannuation with managed fund options | One Form 8621 per fund |

| Employer savings plan | Company-sponsored investment plan with foreign fund options | One Form 8621 per fund in the plan |

| Foreign bank investment product | Bank-offered money market or balanced fund in Canada, Germany, or Singapore | One Form 8621 per product |

| Self-directed foreign brokerage | Buying ETFs on a foreign stock exchange (LSE, TSX, ASX) | One Form 8621 per ETF |

| Inherited foreign investments | Receiving foreign mutual funds from a relative’s estate | One Form 8621 per fund inherited |

If you own 10 foreign mutual funds, you need 10 separate Form 8621 filings. This is one reason the form is so time-consuming and why small portfolios with many funds can generate enormous compliance burdens.

Check the International Securities Identification Number (ISIN) on your investment statements. If the ISIN begins with “US,” the fund is registered in the United States and is not a PFIC. Any other country code (such as “GB” for the UK, “CA” for Canada, or “AU” for Australia) likely means the investment is a PFIC.

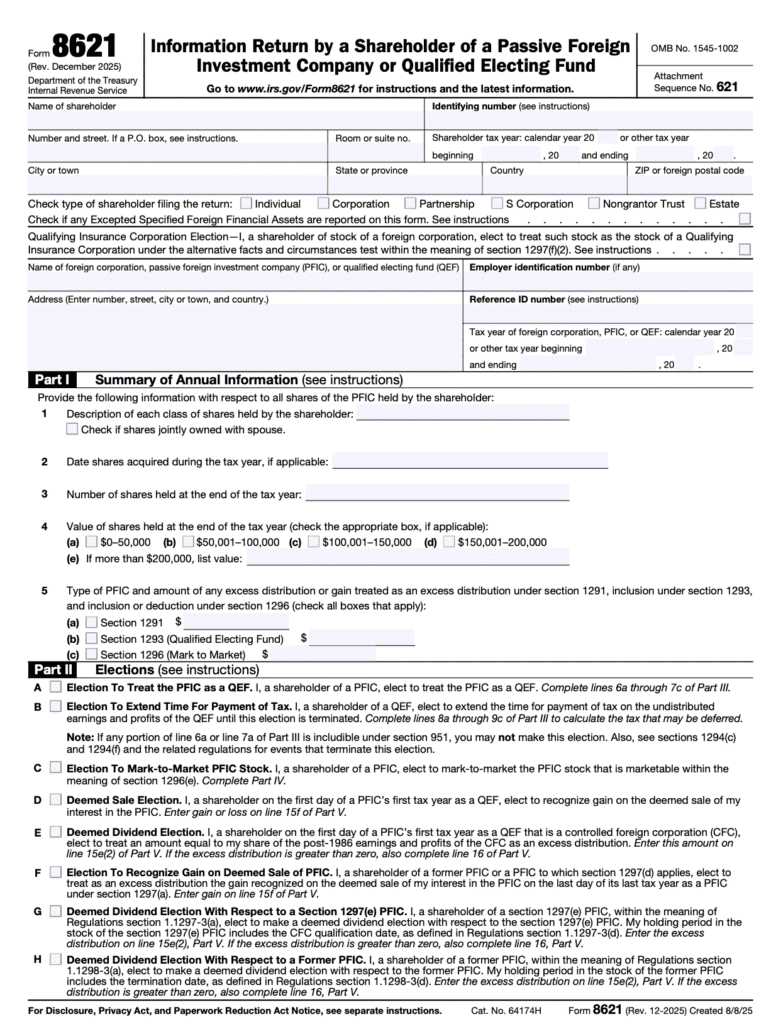

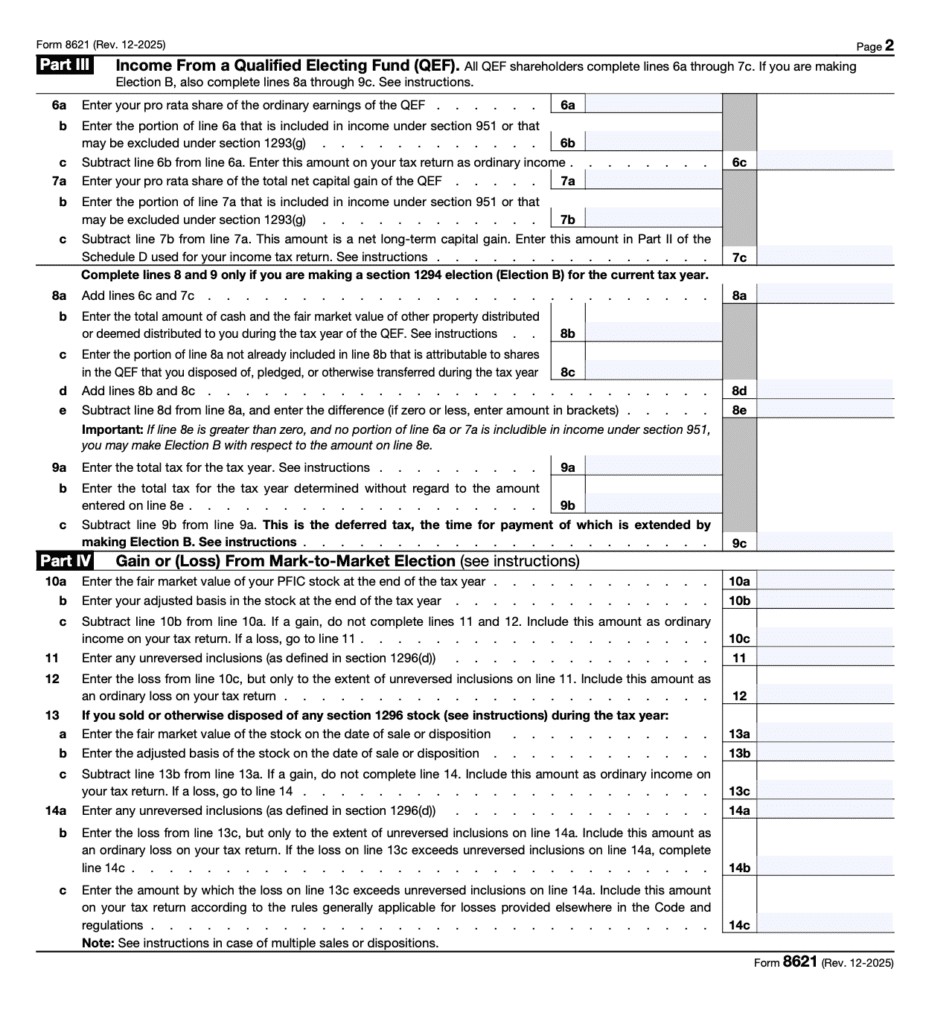

What Does Form 8621 Look Like?

Form 8621 is a multi-page IRS form (revised December 2025) divided into six parts. Each part serves a different purpose, and which parts you complete depends on your specific situation and the tax election you or your accountant chooses.

Structure of Form 8621

| Section | What It Covers | When You Complete It |

|---|---|---|

| Header | Your personal information, PFIC name, address, EIN or reference ID number, tax year, and share ownership details | Every filing |

| Part I | Summary of annual information (share class, fair market value at year-end, number of shares held) | Every filing when required under Section 1298(f) |

| Part II | Elections (QEF, Mark-to-Market, Deemed Sale, Deemed Dividend, and other elections) | Only when making or maintaining an election |

| Part III | Income from a Qualified Electing Fund (ordinary earnings and net capital gain) | Only if the QEF election is in effect |

| Part IV | Gain or loss from a Mark-to-Market election (year-end fair market value vs. adjusted basis) | Only if the MTM election is in effect |

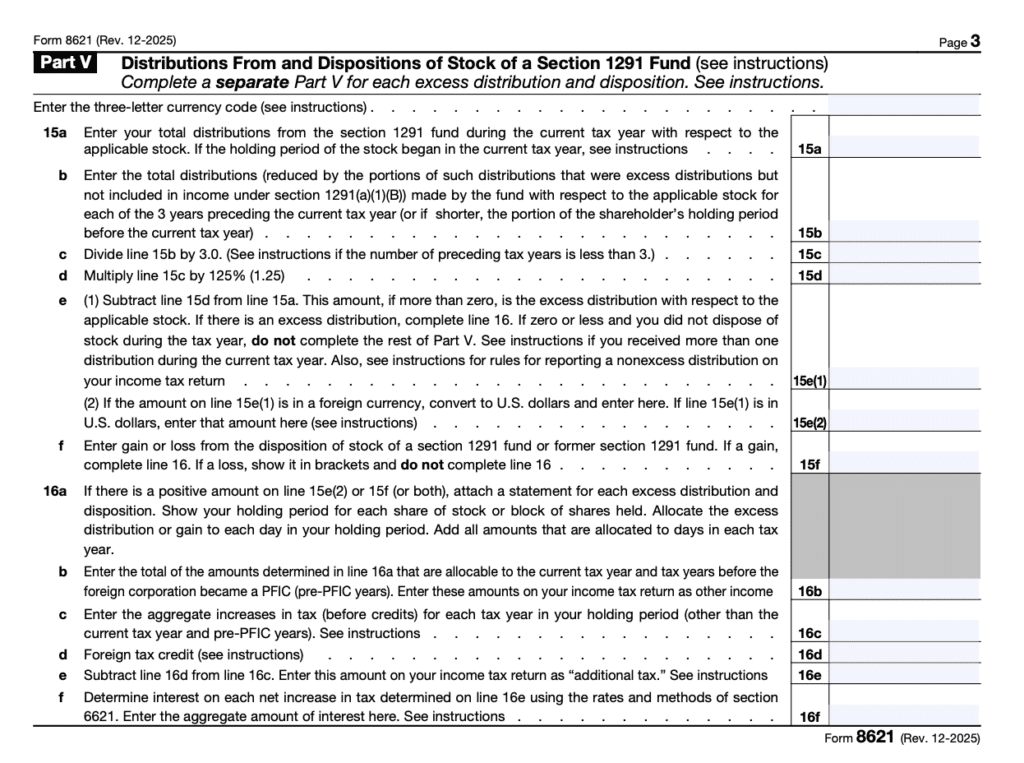

| Part V | Distributions from and dispositions of stock of a Section 1291 fund (the default “excess distribution” method) | When you receive distributions or sell shares without a QEF or MTM election |

| Part VI | Status of prior year Section 1294 elections and termination of elections | Only if you previously elected to defer tax on QEF income |

The December 2025 revision added a new requirement in Part V: filers must now enter a three-letter currency code above Line 15a to identify the currency in which distributions were received. This matters for expats who receive investment income in foreign currencies.

Why the Structure Makes DIY Filing Risky

The challenge is not simply filling in boxes. It is knowing which parts apply to your situation, which election produces the lowest tax bill over time, and how to coordinate the form with the rest of your expat return. The wrong election, or failing to make one at all, can lock you into the punitive default taxation method for years. And because each PFIC requires its own form, errors multiply across your portfolio.

For a detailed comparison of the three taxation methods (Excess Distribution, Mark-to-Market, and QEF), see our PFIC tax rules guide.

Form 8621 Errors Can Be Costly

Why Is Form 8621 So Difficult to File?

Form 8621 is widely considered one of the most complex forms in the entire U.S. tax code. Here is why it creates so many problems for expats who try to handle it on their own.

1. Each PFIC Requires a Separate Form

If you hold five foreign funds, you file five separate Form 8621s. Each one requires its own set of calculations, its own election decision, and its own basis tracking. A typical expat with a diversified foreign investment portfolio can easily spend more time on Form 8621 than on the rest of their return combined.

2. The Taxation Method Choice Is Permanent (or Nearly So)

The IRS offers three methods for taxing PFIC income, but the default method (Excess Distribution under Section 1291) is the most punitive. It spreads gains across all years of ownership, applies the highest tax rate for each year, and adds an interest charge on top. The alternative methods, Mark-to-Market and Qualified Electing Fund, must be elected on the form and have specific requirements and timing rules.

Making the wrong election, or missing the window to make one, can cost thousands of dollars. Changing an election after the election requires IRS approval or specific triggering events. This is not a decision you want to get wrong.

3. Currency Conversion Adds Complexity

Foreign investments generate income in foreign currencies. You must convert all amounts to U.S. dollars using IRS-approved exchange rates and maintain consistency in the method you use. The December 2025 revision now requires you to identify the currency on Part V, making this step mandatory rather than optional.

4. Basis Tracking Across Years Is Critical

Your cost basis in PFIC shares changes each year, depending on the election method you use. QEF elections increase your basis by the income you report annually. Mark-to-Market elections adjust your basis to the year-end fair market value. If you switch methods, change brokers, or lose records, reconstructing your basis can be extraordinarily difficult.

5. The Form Interacts with Your Entire Expat Return

Form 8621 does not exist in isolation. The income it generates flows into your Form 1040, affects your eligibility for the Foreign Tax Credit (Form 1116), and may create additional tax reported on Schedule 2. If you also have FBAR obligations or FATCA reporting requirements (Form 8938), your PFIC holdings must be reported on those forms as well.

Getting Form 8621 wrong does not just affect one line on your return. It can cascade through every connected calculation.

What Happens If I Do Not File Form 8621?

Failing to file Form 8621 does not carry a direct monetary penalty the way missing an FBAR does. But the consequences are serious in other ways.

- The statute of limitations stays open indefinitely: Normally, the IRS has three years from the date you file your return to audit it. If you fail to file Form 8621, that clock never starts. The IRS can audit your return for that year at any time, even decades later.

- The IRS can determine your PFIC tax without your input: If the IRS discovers unreported PFIC holdings, it will apply the default excess distribution method, which typically produces the highest possible tax bill plus interest charges.

- Accuracy-related penalties may apply: If the IRS determines that your PFIC income was underreported, you could face a 20% accuracy-related penalty on the underpayment.

- It can disqualify you from amnesty programs: If you are behind on multiple years of PFIC reporting and want to use the Streamlined Filing Compliance Procedures to catch up, having incomplete Form 8621 filings can complicate or delay the process.

- Related forms may also be affected: PFIC holdings above certain thresholds must also be reported on Form 8938 (FATCA) and the FBAR. Failing to file Form 8621 often signals that these other forms were also missed, compounding the compliance risk.

What Other Forms Do I Need Alongside Form 8621?

PFIC reporting rarely exists in isolation. Depending on the value and type of your foreign investments, you may also need:

| Form | When Required | Penalty for Non-Filing |

|---|---|---|

| FBAR (FinCEN Form 114) | Foreign accounts totaling $10,000+ at any point during the year | Up to $16,536 per form (non-willful) |

| Form 8938 (FATCA) | Foreign financial assets above $200,000/$400,000 (abroad) at year-end | $10,000 per year, up to $60,000 |

| Form 1116 | Claiming Foreign Tax Credit for taxes paid on PFIC income | No penalty, but you lose the credit |

| Form 8858 | Foreign disregarded entity holding PFIC investments | $10,000 per form |

| Form 5471 | 10%+ ownership in a foreign corporation that owns PFICs | $10,000 per form |

Your Greenback accountant identifies all required forms as part of your return preparation, so nothing falls through the cracks.

What If I Am Behind on Form 8621 Filings?

If you have owned PFICs for years without filing Form 8621, you are not alone. Many Americans abroad discover their PFIC obligations well after they have built up a foreign investment portfolio. The IRS provides pathways to get compliant.

- Streamlined Filing Compliance Procedures: If your failure to file was non-willful (you did not know about the requirement), you may qualify for the Streamlined Filing Procedures. This program requires filing the last 3 years of tax returns and 6 years of FBARs, with Form 8621 for all years in which PFICs were held. For expats living abroad, all late-filing penalties are waived.

- Amended returns: If you filed tax returns but omitted Form 8621, you can file amended returns (Form 1040-X) with the missing forms attached. This closes the open statute of limitations for those years.

- Late QEF elections: If you should have made a QEF election in a prior year, the IRS allows late elections under certain circumstances. This can retroactively reduce your tax liability compared to the default excess distribution method.

Getting caught up on PFIC reporting is significantly easier with professional help, as the accountant can evaluate which election method yields the best outcome across all prior years, not just the current one.

Do I Need to File Form 8621 Every Year?

Yes. If you own shares in a PFIC at any point during the tax year, you must file Form 8621 annually as part of your U.S. tax return under the Section 1298(f) reporting requirement. This applies even in years when you receive no distributions, sell no shares, and the investment generates no taxable income. The annual filing obligation continues for every year you hold the PFIC, and a separate form is required for each PFIC in your portfolio every year.

The only exception is the de minimis threshold: if the total year-end value of all your PFIC holdings is under $25,000 ($50,000 for married filing jointly) and you did not receive any distributions or dispose of any shares, you can report all PFICs on a single Form 8621 instead of filing separate forms for each one. You still must file, but the reporting is simplified.

If you sell all your PFIC shares during the year, you file Form 8621 one final time to report the disposition. After that, the annual filing obligation for that specific PFIC ends.

What Is the Difference Between FBAR and Form 8621?

The FBAR (FinCEN Form 114) and Form 8621 serve different purposes and are filed with different agencies, but many expats need both.

| FBAR | Form 8621 | |

|---|---|---|

| What it reports | Foreign financial accounts (bank accounts, investment accounts, pensions) | Ownership in Passive Foreign Investment Companies (PFICs) |

| Filed with | FinCEN (Treasury Department) | IRS (attached to your Form 1040) |

| Threshold | $10,000 aggregate across all foreign accounts at any point during the year | $25,000/$50,000 year-end PFIC value (but must file with any distribution or sale) |

| What triggers it | Having foreign accounts, regardless of what is in them | Owning shares in foreign mutual funds, ETFs, REITs, or similar pooled investments |

| Penalty for non-filing | Up to $16,536 per form (non-willful) | No direct penalty, but the statute of limitations stays open indefinitely |

| Filing deadline | April 15, automatic extension to October 15 | Filed with your tax return (April 15 / June 15 for expats / October 15 with extension) |

The key distinction: FBAR reports where your money is held (the accounts), while Form 8621 reports what you own (the PFIC investments inside those accounts). A single foreign brokerage account holding five foreign mutual funds could trigger one FBAR filing and five separate Form 8621 filings.

For a full breakdown of FBAR vs. FATCA reporting, see our guide on FBAR vs. FATCA: Which Foreign Account Reporting Do I Need?

How Greenback Handles Form 8621

PFIC reporting is one of the most specialized areas of expat tax preparation. At Greenback, Form 8621 is a form our CPAs and Enrolled Agents prepare regularly for clients in 190+ countries. Here is what that looks like in practice.

- Identifying PFICs in your portfolio: Your accountant reviews your foreign investment statements to determine which holdings are PFICs and which are not. Many expats assume all foreign investments trigger Form 8621, but individual foreign stocks, U.S.-registered funds held abroad, and most qualified foreign pensions do not. Getting this classification right avoids unnecessary filings and fees.

- Choosing the right taxation method: For each PFIC, your accountant evaluates whether the Qualified Electing Fund election, Mark-to-Market election, or the default Section 1291 treatment produces the lowest tax over time. This analysis considers your holding period, the type of fund, whether the fund provides a PFIC Annual Information Statement, and your overall tax situation.

- Preparing each Form 8621 accurately: Every PFIC gets its own form with the correct parts completed, proper currency conversions, and accurate basis calculations. Your accountant coordinates these forms with the rest of your expat return so that the numbers on Form 8621 align with your Form 1040, Form 1116, FBAR, and Form 8938.

- Catching up on missed years: If you are behind on PFIC reporting, your accountant determines the best compliance path, whether that is Streamlined Filing Procedures, amended returns, or late elections, and prepares all required forms for prior years.

Greenback charges $300 per Form 8621 with distributions and $200 without distributions. See our full pricing for additional tax forms.

No matter how late, messy, or complex your PFIC situation may be, we can help. You will have peace of mind, knowing that your taxes were done right.

If you are ready to be matched with a Greenback accountant, click the get started button below. For questions about Form 8621 or PFIC reporting, contact us, and one of our Customer Champions will be happy to help. If you have foreign investments and are not sure whether they qualify as PFICs, learn more about how we help expats with complex investments.

Get Form 8621 Filed Correctly

This article is for informational purposes only and does not constitute tax, legal, or accounting advice. PFIC rules are highly complex and fact-specific. For guidance on your specific investments, contact Greenback to speak with an expat tax specialist.

Related Resources

- PFIC Tax Rules: What Expats Need to Know About Foreign Funds

- FBAR: What It Is, Who Must File, and How to Report Foreign Accounts

- What Is FATCA? Foreign Account Tax Compliance Act Explained

- Streamlined Filing for U.S. Expats: Your Penalty-Free Path to Compliance

- Form 1040 for U.S. Expats: Filing Made Simple

- Foreign Tax Credit Guide for Expats

- Do I Need Form 1040 Schedule 2?

- Amending Your U.S. Tax Return with Form 1040-X

- Form 8858: Information Return for Foreign Disregarded Entities

- Form 5471: Information Return for U.S. Persons with Foreign Corporations