Form 8863 for Expats Explained: How to Claim Education Tax Credits

- What Information Do I Need Before Starting Form 8863?

- How Do I Complete Form 8863 Step by Step?

- The FEIE Income Trap on Form 8863

- Common Form 8863 Problems for Expats

- Where Does Form 8863 Go on My Tax Return?

- What If I Missed Claiming Education Credits in Prior Years?

- Frequently Asked Questions

- Related Resources

Form 8863 is the only way to claim the American Opportunity Tax Credit (AOTC) or Lifetime Learning Credit (LLC) on your federal tax return. Without this form, you cannot receive either credit, even if you qualify. According to the IRS, Form 8863 calculates your credit amount and transfers it to your Form 1040.

For expats, the form works the same as it does for domestic filers, but two common complications trip people up: the MAGI add-back when you use the Foreign Earned Income Exclusion, and missing documentation from foreign schools. Both are solvable if you know what to expect.

For a full breakdown of which education credit is right for your situation, eligibility rules, and qualifying expenses, see our guide on claiming education credits while studying abroad.

Not Sure If You Qualify for Education Credits?

Here’s how to complete Form 8863 correctly as an American living abroad.

What Information Do I Need Before Starting Form 8863?

Gather all of this before you open the form:

| What You Need | Where to Get It | Expat Notes |

|---|---|---|

| Student’s name and SSN | Social Security card | Must be issued before your filing deadline (including extensions) for the AOTC |

| School name, address, and EIN | Form 1098-T or the school’s registrar | Many foreign schools don’t have an EIN (see below) |

| Form 1098-T | Issued by the school, usually by Jan. 31 | Most foreign schools don’t issue this form |

| Total qualified expenses paid | Your payment records, receipts, bank statements | Convert foreign currency to USD using the rate on the date of payment |

| Your MAGI | Your Form 1040 + any FEIE excluded income added back | This is the step most expats miss (see below) |

| Whether you’ve claimed AOTC before | Prior year returns | AOTC is limited to 4 tax years per student |

How Do I Complete Form 8863 Step by Step?

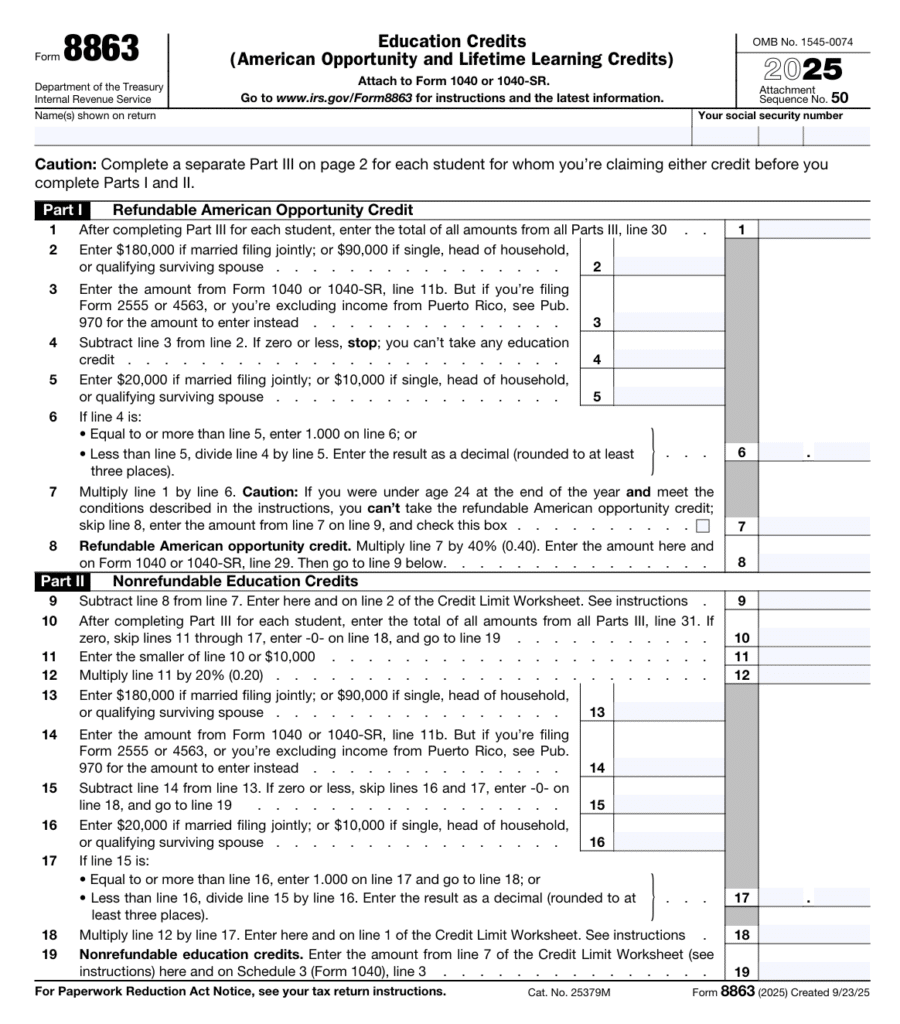

Form 8863 is two pages with three parts. Work through them in this order:

Start with Part III (Page 2): Student and School Information

Complete a separate Part III for each student. This is where most of the work happens.

- Lines 20-21: Enter the student’s name and SSN exactly as they appear on your Form 1040.

- Lines 22a-22d: Enter school information. If the student attended two schools, use columns (a) and (b).

- School EIN: This is where expats often hit a wall. If your foreign school doesn’t have a U.S. EIN, contact the registrar or financial aid office. Schools participating in U.S. federal student aid programs often have one. If the school truly doesn’t have an EIN, you can still claim the LLC (which doesn’t require it), but the AOTC does require the school’s EIN.

- Line 22e: Check whether you received Form 1098-T. If not (as is common in foreign schools), check “No.” You can still claim credits with alternative documentation: official tuition receipts, enrollment verification letters, and payment records.

- Lines 23-24: Answer whether the AOTC has been claimed for this student for 4 or more prior years, and whether the student completed the first 4 years of postsecondary education. These determine AOTC eligibility.

- Line 25: Check that the student meets the half-time enrollment requirement (AOTC only).

- Line 27: Enter adjusted qualified education expenses for the AOTC calculation. The form computes 100% of the first $2,000 plus 25% of the next $2,000 on Lines 27-30.

- Line 31: Enter adjusted qualified education expenses for the LLC calculation (up to $10,000).

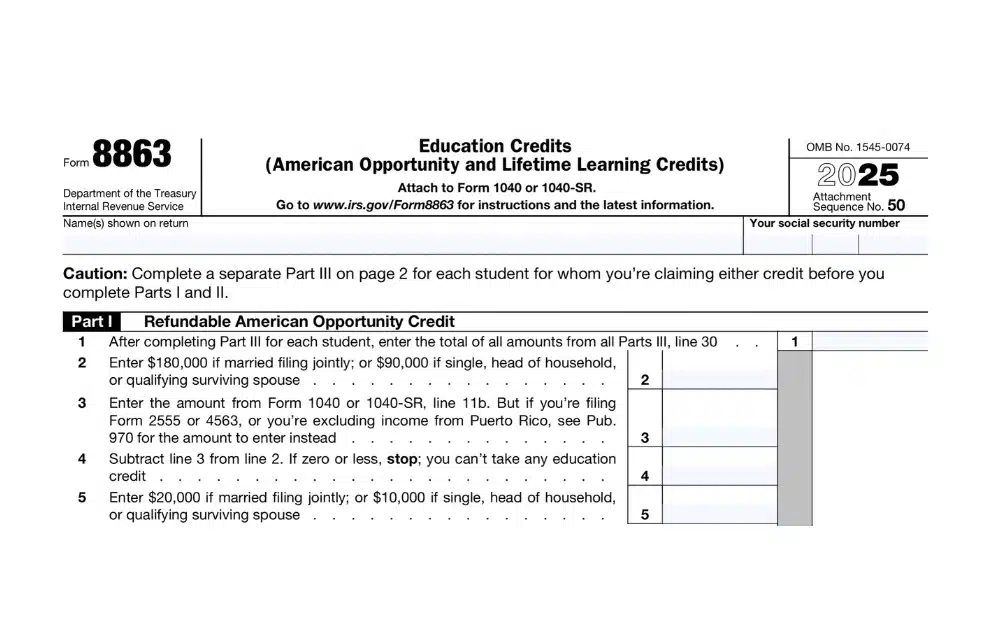

Then Part I (Page 1): Refundable American Opportunity Credit

- Line 1: Enter the total of all tentative AOTC amounts from Part III, Line 30 (for all students).

- Lines 2-4: These lines calculate the income phase-out. Enter your MAGI on Line 3.

Important for expats using the FEIE: Line 3 requires your Modified Adjusted Gross Income. If you filed Form 2555 to exclude foreign income, you must add the excluded amount back to your AGI for this line. Your Form 1040 may show $0 AGI, but your MAGI for Form 8863 includes excluded income.

| If your filing status is… | Full credit if MAGI is… | Phased out at… | No credit above… |

|---|---|---|---|

| Single, head of household | $80,000 or less | $80,001 to $89,999 | $90,000 |

| Married filing jointly | $160,000 or less | $160,001 to $179,999 | $180,000 |

- Line 7: Your tentative credit after the phase-out reduction.

- Line 8: The refundable portion. Multiply Line 7 by 40%. This is the amount you can receive as a refund, even if you owe $0 in taxes (up to $1,000 per student). This goes to Form 1040, Line 29.

- Line 9: The nonrefundable portion (Line 7 minus Line 8). This goes to the Credit Limit Worksheet.

Then Part II (Page 1): Nonrefundable Education Credits

- Line 10: Enter the total LLC amounts from Part III, Line 31 (for all students). Multiply by 20% (up to $2,000 max).

- Lines 11-18: These lines combine the nonrefundable AOTC portion (Line 9) with the LLC (Line 10), apply the MAGI phase-out, and calculate the Credit Limit Worksheet to determine how much you can claim against your actual tax liability.

- Line 19: Your total nonrefundable education credit. This goes to Schedule 3 (Form 1040), Line 3.

The FEIE Income Trap on Form 8863

This is the most common mistake expats make with this form. The income phase-out on Lines 3-4 (Part I) and Lines 14-15 (Part II) uses MAGI, which includes FEIE excluded income added back.

Example: You earn $92,000 in London and exclude all of it using the FEIE. Your Form 1040 shows $0 AGI. But for Form 8863, Line 3, your MAGI = $0 + $92,000 = $92,000. As a single filer, you exceed the $90,000 cutoff and cannot claim either credit.

If both spouses use the FEIE, add back both exclusion amounts.

If you’re near the threshold, compare whether the Foreign Tax Credit produces a better overall result than the FEIE. The FTC doesn’t trigger the MAGI add-back, which may preserve your eligibility for education credits. See our FEIE vs. FTC comparison.

Common Form 8863 Problems for Expats

Foreign School Has No EIN

Contact the school’s registrar or financial aid office first. Many qualifying foreign institutions have obtained an EIN through their participation in U.S. student aid programs. If the school truly doesn’t have one, you can still claim the LLC. The AOTC requires the school’s EIN on the form.

No Form 1098-T Received

Most foreign schools don’t issue this form. The IRS allows you to claim credits without it if you can substantiate expenses through alternative documentation: official tuition invoices, enrollment verification, and payment receipts. Keep these records for at least three years.

Currency Conversion

Convert all foreign-currency expenses to U.S. dollars using the exchange rate on the date you paid the expense. Use IRS-approved exchange rates or a consistent commercial source. Document the rate and source for each conversion.

Multiple Students at Different Schools

Complete a separate Part III for each student. Use additional copies of Page 2 as needed. All students’ amounts flow into Parts I and II on Page 1.

Where Does Form 8863 Go on My Tax Return?

| Amount | Goes To |

|---|---|

| Refundable AOTC (Part I, Line 8) | Form 1040, Line 29 |

| Nonrefundable credits (Part II, Line 19) | Schedule 3 (Form 1040), Line 3 |

Form 8863 must be attached to your Form 1040. It cannot be filed separately. If you’re an expat using the automatic June 15 extension (or October 15 with Form 4868), Form 8863 follows the same deadline.

Timing rule: You can claim expenses paid in 2025 for academic periods that begin in 2025 or the first three months of 2026. A December 2025 tuition payment for a spring 2026 semester qualifies on your 2025 return.

What If I Missed Claiming Education Credits in Prior Years?

If you filed returns but didn’t include Form 8863, you can file an amended return (Form 1040-X) within three years of the original due date. Attach the completed Form 8863 to the amendment.

If you haven’t filed at all, the Streamlined Filing Procedures let you catch up on three years of returns and claim missed credits without penalties (assuming your failure to file was non-willful).

Frequently Asked Questions

Not necessarily. While the IRS generally requires a 1098-T, most foreign schools don’t issue one. You can claim credits with alternative documentation (official receipts, enrollment records, payment proof) if you follow the exception procedures in the Form 8863 instructions. The AOTC does require the school’s EIN regardless.

Form 8863 requires you to add back any income excluded under the FEIE (Form 2555) or income excluded under Sections 931 or 933. This add-back is calculated on Lines 3-4 (Part I) and Lines 14-15 (Part II).

Yes, but not for the same student. You can claim the AOTC for one student and the LLC for another on the same return. Complete a separate Part III for each student, then flow the amounts into Part I (AOTC) or Part II (LLC) accordingly.

That’s exactly how it’s designed to work. Up to 40% of the AOTC (maximum $1,000 per student) is refundable, meaning you receive it as a direct refund even if you owe $0 in taxes. This is especially valuable for expats who use the FEIE and have no remaining tax liability.

At least three years after filing the return. Keep tuition receipts, enrollment verification, currency conversion documentation, and any correspondence with schools about EINs.

Yes, Form 8863 can be e-filed with your Form 1040. There are no special paper-filing requirements for this form.

At Greenback, we handle Form 8863 alongside the FEIE, Foreign Tax Credit, and other expat-specific benefits to make sure you claim every dollar you’re entitled to. If you’re unsure whether the MAGI add-back disqualifies you or if you need help gathering documentation from a foreign school, we can sort it out.

If you’re ready to be matched with a Greenback accountant, click the get started button below. For general questions on expat taxes or working with Greenback, contact our Customer Champions.

Claim Your Education Credits the Right Way

This article is for informational purposes only and should not be considered tax advice. For the latest guidance, see IRS Publication 970 and the Form 8863 instructions. Always consult with a qualified tax professional regarding your specific situation.

Related Resources

- Education Credits for Americans Studying Abroad

- FEIE vs. FTC: Which Strategy Saves You More?

- U.S. Taxes for Families with Children Studying Abroad

- Continuing Education Tax Deductions Abroad

- Foreign Earned Income Exclusion

- Foreign Tax Credit Guide

- IRS Foreign Exchange Rates

- Amended Tax Returns for Expats

- Streamlined Filing Procedures

- U.S. Expat Tax Deductions and Credits