Child Tax Credit for Expats: How to Claim Up to $2,200 Per Child

- Can U.S. Expats Claim the Child Tax Credit?

- How Much Is the Child Tax Credit Worth in 2026?

- How the Foreign Earned Income Exclusion (FEIE) Affects Your Child Tax Credit

- How the Foreign Tax Credit (FTC) Preserves Your Refund

- Understanding the Additional Child Tax Credit (Refundable Portion)

- Step-by-Step: How to Claim the Child Tax Credit as an Expat

- Common Scenarios: FEIE vs. FTC for Expat Families

- What If I Missed Claiming the Child Tax Credit in Previous Years?

- How OBBA Changed the Child Tax Credit for Expats

- Tips for Maximizing Your Child Tax Credit as an Expat

- When You Need Professional Help

- Final Thoughts: Peace of Mind for Expat Parents

- Related Resources

- Frequently Asked Questions

The Child Tax Credit is one of the most valuable benefits for Americans raising children abroad. According to the IRS, the maximum credit increased to $2,200 per qualifying child for the 2025 tax year, with up to $1,700 refundable even if you owe no U.S. income tax.

You could qualify for this full credit even while living outside the U.S. And if you structure your return correctly, you may receive up to $1,700 per child as a direct refund to your bank account.

However, claiming the Child Tax Credit as an American abroad requires careful planning around two critical decisions: whether to use the Foreign Earned Income Exclusion or the Foreign Tax Credit, and how much earned income you report. These choices directly determine whether you can access the refundable portion worth up to $1,700 per child.

In this guide, you’ll learn exactly who qualifies for the Child Tax Credit, how the refundable portion works for expats, why your choice between FEIE and FTC matters so much, and how to claim this credit step-by-step on your return.

Can U.S. Expats Claim the Child Tax Credit?

Yes, U.S. citizens and green card holders living abroad can claim the Child Tax Credit if they meet all eligibility requirements. Your physical location doesn’t disqualify you from this benefit.

The One Big Beautiful Bill Act (OBBA), passed in July 2025, made important changes to the Child Tax Credit while preserving eligibility for Americans abroad. The credit increased from $2,000 to $2,200 per qualifying child, and new Social Security Number requirements took effect.

Eligibility Requirements for the Child Tax Credit

To claim the Child Tax Credit for the 2025 tax year, both you and your child must meet these IRS requirements:

Child Requirements:

- Under age 17 by December 31, 2025

- U.S. citizen, U.S. national, or U.S. resident alien

- Has a valid Social Security Number (SSN) issued before the tax filing deadline

- Lives with you for more than half the year (temporary absences for school count)

- You claim the child as a dependent on your return

- Child cannot provide more than half of their own financial support

- Must be your son, daughter, stepchild, eligible foster child, brother, sister, stepbrother, stepsister, half-brother, half-sister, or a descendant of one of these (grandchild, niece, or nephew)

Parent Requirements (New for 2025):

- At least one parent must have a valid SSN (if filing jointly, only one spouse needs an SSN)

- You cannot file as Married Filing Separately (this filing status now disqualifies you from the Child Tax Credit)

Use the IRS Interactive Tax Assistant to see if you’re eligible to claim the CTC, ACTC or ODC.

These requirements apply whether you file from Toronto or Tokyo. The key difference for expats lies in how you structure your return to maximize both the nonrefundable and refundable portions of the credit.

What If My Child Was Born Abroad?

Children born outside the U.S. to American parents are U.S. citizens and fully qualify for the Child Tax Credit. However, you must obtain their SSN through a U.S. embassy or consulate before filing your return. An ITIN (Individual Taxpayer Identification Number) will not qualify your child for this credit.

Start the SSN application process as soon as possible after your child’s birth. Processing times at U.S. embassies vary, and you’ll need this number before you can claim your child on your tax return.

Not sure if you can claim the Child Tax Credit while living overseas?

How Much Is the Child Tax Credit Worth in 2026?

For the 2025 tax year (filed in 2026), the Child Tax Credit provides:

| Credit Component | Amount Per Child |

|---|---|

| Maximum total credit | $2,200 |

| Refundable portion (Additional Child Tax Credit) | Up to $1,700 |

| Minimum earned income required | $2,500 |

The $2,200 credit works in two parts:

- Nonrefundable portion: Reduces your U.S. tax liability dollar-for-dollar down to zero

- Refundable portion: Can generate a direct refund of up to $1,700 per child even if you owe no taxes

This distinction matters tremendously for expats. Many Americans living abroad use the Foreign Earned Income Exclusion to eliminate their U.S. tax liability completely. While this is excellent for reducing taxes, it also means you may not have tax liability to offset with the nonrefundable portion. This is where the refundable Additional Child Tax Credit becomes valuable.

Income Limits and Phaseout Rules

The Child Tax Credit begins phasing out once your modified adjusted gross income (MAGI) exceeds:

- $200,000 for single filers, head of household, or married filing separately

- $400,000 for married filing jointly

The credit reduces by $50 for every $1,000 (or fraction thereof) of income over these thresholds.

Example calculation: Sarah is a single filer earning $230,000 in Germany with two qualifying children.

Her income exceeds the threshold by $30,000 ($230,000 – $200,000). $30,000 ÷ $1,000 = 30 increments 30 × $50 = $1,500 total reduction

Instead of receiving $4,400 (2 children × $2,200), Sarah receives $2,900 ($4,400 – $1,500).

Calculating Your Modified Adjusted Gross Income (MAGI)

For the Child Tax Credit, your MAGI equals your adjusted gross income (AGI) from your tax return, plus:

- Excluded foreign earned income (Form 2555)

- Excluded foreign housing costs

- Excluded income for bona fide residents of American Samoa and Puerto Rico

Even if you exclude foreign income using the FEIE, you must add it back when calculating whether you exceed the phaseout thresholds.

How the Foreign Earned Income Exclusion (FEIE) Affects Your Child Tax Credit

Here’s where many expats get surprised: Using the Foreign Earned Income Exclusion can eliminate your ability to claim the refundable portion of the Child Tax Credit.

Why FEIE Blocks the Refundable Credit

The Foreign Earned Income Exclusion allows you to exclude up to $130,000 of foreign earned income from U.S. taxation for the 2025 tax year. When you exclude this income:

- Your U.S. taxable income decreases (often to zero)

- Your U.S. tax liability decreases (often to zero)

- You have less (or no) tax liability to offset with the nonrefundable portion of the Child Tax Credit

- Most importantly: The IRS rule states that if you claim FEIE on Form 2555, you cannot claim the refundable Additional Child Tax Credit

The IRS is clear on this: You cannot exclude foreign earned income and then claim a refund through the Additional Child Tax Credit. This trade-off forces expats to choose between two valuable benefits.

Example: Lost refund opportunity Mark and Lisa live in Dubai (no income tax) with two children. Mark earns $95,000 annually.

Using FEIE:

- Excludes all $95,000 from U.S. taxation

- Owes $0 in U.S. taxes (excellent!)

- Cannot claim the $3,400 refundable portion (2 children × $1,700)

- Total tax benefit: $95,000 exclusion

Using Foreign Tax Credit:

- Reports all $95,000 as taxable income

- Would owe approximately $9,800 in U.S. taxes

- Has no foreign taxes to credit (Dubai has no income tax)

- Can claim nonrefundable Child Tax Credit: $4,400 reduces tax owed to $5,400

- Cannot claim refundable portion because still owes taxes

- Total benefit: $4,400 credit

In Mark and Lisa’s case, FEIE is clearly better because they’re in a zero-tax country and can’t benefit from the Foreign Tax Credit anyway.

How the Foreign Tax Credit (FTC) Preserves Your Refund

The Foreign Tax Credit provides a dollar-for-dollar credit for foreign income taxes you’ve already paid. Unlike FEIE, using FTC allows you to maintain eligibility for the refundable Additional Child Tax Credit.

Why FTC Works Better for Families in High-Tax Countries

When you use Form 1116 to claim Foreign Tax Credit:

- You report all worldwide income as taxable

- You calculate your U.S. tax liability on that income

- You apply your foreign tax credit to offset U.S. taxes

- You remain eligible for the full Child Tax Credit, including the refundable portion

Example: Maximizing both benefits Jennifer lives in Germany with one child. She earns $85,000 and pays €24,000 (approximately $26,000) in German taxes.

Using FTC:

- Reports $85,000 as taxable income

- U.S. tax liability: approximately $10,500

- Applies $26,000 Foreign Tax Credit

- U.S. tax liability after FTC: $0 (with $15,500 in excess credits to carry forward)

- Child Tax Credit: $2,200 nonrefundable (but no tax to offset)

- Additional Child Tax Credit (refundable): $1,700 direct refund

- Total benefit: Zero U.S. taxes owed PLUS $1,700 refund

Jennifer ends up in the same place tax-wise (owing zero) but receives an additional $1,700 refund by using FTC instead of FEIE.

When FTC Makes More Sense Than FEIE

Consider using Foreign Tax Credit instead of FEIE if:

- You live in a high-tax country (Germany, France, UK, Scandinavia, Canada, Australia)

- You have qualifying children under age 17

- Your foreign tax rate equals or exceeds your U.S. tax rate

- Your earned income exceeds $2,500 (the threshold for the refundable credit)

The strategic advantage: FTC can reduce your U.S. tax liability to zero while preserving eligibility for the $1,700 refundable credit per child.

Once you revoke the FEIE, you cannot use it again for five years without IRS permission. This makes the decision significant, especially for families planning to move between high-tax and low-tax countries. Consult with an expat tax professional before making this change.

Understanding the Additional Child Tax Credit (Refundable Portion)

The Additional Child Tax Credit (ACTC) is the refundable portion of the Child Tax Credit. This means you can receive it as a direct refund even if you owe no U.S. income tax.

How the Refundable Credit Calculates

The refundable amount equals 15% of your earned income above $2,500, up to a maximum of $1,700 per qualifying child.

Formula: (Earned Income – $2,500) × 15% = Refundable Credit (capped at $1,700 per child)

Example calculations:

- Scenario 1: Lower income Earned income: $15,000 ($15,000 – $2,500) × 15% = $1,875 Maximum refundable with one child: $1,700 Result: $1,700 refund

- Scenario 2: Higher income Earned income: $75,000 ($75,000 – $2,500) × 15% = $10,875 Maximum refundable with two children: $3,400 (2 × $1,700) Result: $3,400 refund

- Scenario 3: Below threshold Earned income: $2,000 ($2,000 – $2,500) = negative number Result: $0 refund (doesn’t qualify because earned income is below $2,500)

Three or More Children: Alternative Calculation

Families with three or more qualifying children may use an alternative calculation based on their Social Security and Medicare taxes paid. This can result in a higher refundable amount. The calculation appears on Schedule 8812, and your tax software or preparer should automatically use whichever method provides the greater benefit.

What Counts as Earned Income

For the Additional Child Tax Credit, earned income includes:

- Wages and salaries (W-2 income)

- Tips

- Self-employment income (after expenses)

- Other compensation for personal services

Earned income does NOT include:

- Interest and dividends

- Pension distributions

- Social Security benefits

- Rental income

- Capital gains

- Unemployment compensation

Use the IRS Interactive Tax Assistant to see if you’re eligible to claim the CTC, ACTC or ODC.

If you’re self-employed abroad, your net profit after business expenses counts as earned income for this calculation. Even freelancers and consultants working from anywhere can qualify if they meet the $2,500 minimum.

Step-by-Step: How to Claim the Child Tax Credit as an Expat

Filing for the Child Tax Credit requires specific forms and strategic decisions. Here’s exactly what you need to do:

Step 1: Decide Between FEIE and FTC

This is your most important strategic decision. Your choice affects not just your current-year taxes but potentially the next five years if you revoke FEIE.

Choose FEIE if:

- You live in a low-tax or no-tax country (UAE, Singapore, Panama, Costa Rica)

- You earn less than $130,000

- You don’t have qualifying children under 17

- You prefer simplicity and don’t mind forgoing the refundable credit

Choose FTC if:

- You live in a high-tax country (most European countries, Canada, Japan, Australia)

- You have qualifying children and want to access the refundable portion

- Your foreign tax rate exceeds your U.S. tax rate

- You earn income above the FEIE limit

If you’re unsure which strategy saves you more money, an expat tax professional can run both scenarios and show you the actual dollar difference.

Step 2: File Form 1040

All U.S. citizens must file Form 1040 regardless of where they live. This is true even if you’ll owe no taxes after applying exclusions and credits.

On Form 1040, you’ll report your worldwide income before applying any exclusions or credits. This includes:

- Foreign wages and salary

- Self-employment income

- Rental income

- Investment income

- Any other income from any source

Step 3: Complete the Appropriate Forms for Your Strategy

If using FEIE:

- Complete Form 2555 to claim the Foreign Earned Income Exclusion

- Attach Form 2555 to your Form 1040

- Note: This disqualifies you from the refundable portion of the Child Tax Credit

If using FTC:

- Complete Form 1116 to claim the Foreign Tax Credit

- Attach Form 1116 to your Form 1040

- This preserves your eligibility for the refundable Additional Child Tax Credit

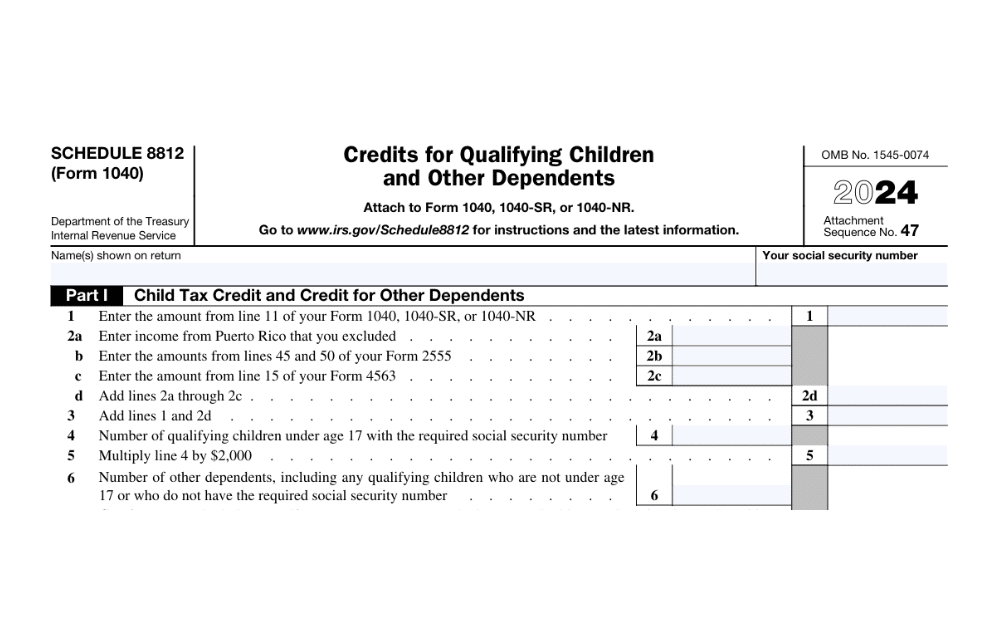

Step 4: Complete Schedule 8812

Schedule 8812 (Credits for Qualifying Children and Other Dependents) is where you calculate both the nonrefundable and refundable portions of the Child Tax Credit.

You’ll need to provide:

- Each child’s name, Social Security Number, and relationship to you

- The number of qualifying children

- Your modified adjusted gross income (including any excluded foreign income added back)

- Your earned income amount

The schedule walks through:

- Calculating your total Child Tax Credit based on the number of qualifying children

- Applying income phaseout reductions if your MAGI exceeds the threshold

- Determining how much of the credit can offset your tax liability (nonrefundable portion)

- Calculating the refundable portion based on your earned income

Even if you used FEIE and excluded all your income, you still complete Schedule 8812. You may be able to claim the nonrefundable portion if you have any U.S. tax liability from other income sources.

Step 5: Report on Schedule 1 (If Applicable)

If you claimed the Foreign Earned Income Exclusion, your excluded income will appear as a negative number on Schedule 1, Line 8d. This reduces your adjusted gross income on your Form 1040.

Step 6: File by the Deadline

Expats receive an automatic two-month extension to file, moving the deadline from April 15 to June 15, 2026 for 2025 tax year returns. However:

- Any taxes owed are still due April 15, 2026

- Interest begins accruing on unpaid balances after April 15

- You can extend further to October 15, 2026 by filing Form 4868

Common Scenarios: FEIE vs. FTC for Expat Families

Real-world examples help illustrate which strategy works best for different situations.

Scenario 1: Digital Nomad in Southeast Asia

Profile: James lives in Thailand with his wife and two children (ages 5 and 8). He works remotely for a U.S. company earning $110,000. Thailand taxes him at approximately 15% ($16,500).

Option A: Using FEIE

- Excludes $110,000 from U.S. taxation

- U.S. tax liability: $0

- Cannot claim refundable Child Tax Credit: $0

- Thailand taxes paid: $16,500

- Total taxes paid: $16,500 (Thailand only)

Option B: Using FTC

- Reports $110,000 as taxable to U.S.

- U.S. tax liability before credits: approximately $14,800

- Foreign Tax Credit: $16,500 applied (eliminates U.S. taxes)

- Child Tax Credit nonrefundable: Not needed (already at $0)

- Child Tax Credit refundable: $3,400 (2 children × $1,700)

- Total taxes paid: $16,500 (Thailand only), PLUS $3,400 refund

Winner: FTC saves James $3,400 through the refundable credit. His total tax burden stays the same, but he receives a direct refund.

Scenario 2: Teacher in the Middle East

Profile: Rachel teaches at an international school in Qatar (no income tax) with one child (age 4). She earns $72,000.

Option A: Using FEIE

- Excludes $72,000 from U.S. taxation

- U.S. tax liability: $0

- Qatar taxes paid: $0

- Child Tax Credit: Cannot claim refundable portion

- Total taxes paid: $0

Option B: Using FTC

- Reports $72,000 as taxable

- U.S. tax liability: approximately $6,200

- Foreign Tax Credit: $0 (no Qatar taxes to credit)

- Child Tax Credit nonrefundable: $2,200 reduces tax owed to $4,000

- Still owes $4,000, so cannot claim refundable portion

- Total taxes paid: $4,000 to U.S.

Winner: FEIE is clearly better for Rachel. With no foreign taxes to credit, FTC provides no benefit and she’d owe $4,000 in U.S. taxes.

Key takeaway: FTC only works better than FEIE if your foreign tax rate is high enough that the Foreign Tax Credit, combined with the Child Tax Credit, reduces your U.S. taxes to zero AND leaves you eligible for the refund.

Scenario 3: Self-Employed Consultant in Germany

Profile: David is a freelance consultant in Berlin with one child (age 12). He earns $95,000 and pays €29,000 (approximately $32,000) in German taxes.

Option A: Using FEIE

- Excludes $95,000 from income tax

- Still owes 15.3% self-employment tax: $14,535

- Cannot claim refundable Child Tax Credit

- Total taxes paid: $14,535 (U.S. self-employment only) + €29,000 (German taxes)

Option B: Using FTC

- Reports $95,000 as taxable

- U.S. income tax before credits: approximately $11,500

- U.S. self-employment tax: $14,535

- Total U.S. taxes before credits: $26,035

- Foreign Tax Credit: $32,000 applied (eliminates all U.S. taxes)

- Child Tax Credit refundable: $1,700

- Total taxes paid: €29,000 (German taxes only), PLUS $1,700 refund

Winner: FTC saves David his entire U.S. tax bill PLUS generates a $1,700 refund. The high German tax rate more than covers his U.S. liability.

Self-employment tax applies to self-employed income regardless of FEIE. The Foreign Tax Credit can potentially offset both income tax and self-employment tax, making it especially valuable for self-employed expats in high-tax countries.

What If I Missed Claiming the Child Tax Credit in Previous Years?

Good news: You can file amended tax returns to claim the Child Tax Credit for up to three years after the filing deadline.

If you qualified for the Child Tax Credit in 2022, 2023, or 2024 but didn’t claim it, you can use Form 1040-X (Amended U.S. Individual Income Tax Return) to claim these credits retroactively.

This is particularly common for expats who:

- Used FEIE without realizing FTC might generate a refund

- Didn’t know they qualified for the refundable portion

- Obtained their child’s SSN after filing the original return

- Weren’t aware they needed to file at all because they owed no taxes

How to Amend for Missed Credits

- Obtain copies of your original returns for the years you want to amend

- Prepare amended Form 1040-X for each year

- Include Schedule 8812 showing your Child Tax Credit calculation

- If switching from FEIE to FTC, include Form 1116 and any required revocation statements

- Attach all supporting documentation

- Mail your amended returns to the appropriate IRS address (e-filing is not available for amended returns)

Switching from FEIE to FTC is permanent for five years unless you obtain IRS permission. Make sure this strategy benefits you for the long term before filing amended returns that revoke your FEIE election.

Greenback has helped hundreds of expat families recover thousands of dollars in missed Child Tax Credits. If you’re unsure whether amending would benefit you, we can review your previous returns and calculate the potential refund.

How OBBA Changed the Child Tax Credit for Expats

The One Big Beautiful Bill Act (OBBA), signed into law on July 4, 2025, made several significant changes to the Child Tax Credit:

Key Changes Under OBBA

- Increased maximum credit: From $2,000 to $2,200 per qualifying child

- Inflation indexing: Starting in 2026, the maximum credit will adjust annually for inflation

- SSN requirement for parents: At least one parent must now have a work-eligible SSN (new rule for 2025)

- Permanent provisions: The enhanced credit amount and income thresholds are now permanent, rather than set to expire

What Stayed the Same

- Income phaseout thresholds ($200,000/$400,000)

- Refundable portion cap ($1,700)

- Earned income requirement ($2,500)

- Age limit (under 17)

- Residency requirements

These changes benefit expat families by providing a slightly higher credit and ensuring the enhanced provisions won’t expire, giving families long-term tax planning certainty.

Tips for Maximizing Your Child Tax Credit as an Expat

1. Run Both FEIE and FTC Scenarios

Before filing, calculate your taxes both ways. Many expats are surprised to find that switching from FEIE to FTC actually saves money when the refundable Child Tax Credit is factored in.

2. Time Your Move Strategically

If you’re planning to move to a high-tax country and have young children, consider whether switching from FEIE to FTC makes sense. The five-year restriction on re-electing FEIE means this decision has long-term implications.

3. Keep Your Child’s SSN Application Moving

If you have a newborn abroad, start the SSN application immediately. Processing delays at embassies can take months, and you cannot claim your child without this number.

4. Maintain Documentation

Keep records proving your child lived with you for more than half the year. This is especially important for expats with children in boarding school or who travel frequently.

5. Coordinate with Your Spouse

If you’re married filing jointly and both work abroad, make sure you’re using the same strategy (FEIE or FTC) consistently across both incomes for maximum benefit.

6. Consider State Tax Implications

Some U.S. states may still consider you a resident even while living abroad. State tax rules vary significantly. If you maintain state tax residency, factor state taxes into your FEIE vs. FTC decision.

7. Track Your Earned Income Carefully

If you’re close to the $2,500 earned income threshold for the refundable portion, consider whether additional work or timing of payments might push you over the threshold before year-end.

8. Review Annually

Your optimal strategy can change as your income changes, your children age, or you move to different countries. What worked best last year might not be optimal this year.

When You Need Professional Help

Deciding between FEIE and FTC while maximizing the Child Tax Credit involves complex calculations and long-term strategic planning. Consider getting professional help if:

- You earn more than $100,000 and live in a high-tax country

- You have three or more qualifying children

- You’re considering switching from FEIE to FTC

- You’ve moved countries during the tax year

- You’re self-employed and dealing with both income tax and self-employment tax

- You have multiple income sources (employment, rental, investment income)

- You’re behind on previous years’ filings and want to claim missed credits

Greenback Tax Services specializes in helping American expats file correctly and claim every credit they’re entitled to. Our expat tax professionals can:

- Calculate both FEIE and FTC scenarios to show you which saves more money

- Prepare all required forms including Schedule 8812, Form 2555, or Form 1116

- File amended returns to claim missed Child Tax Credits from previous years

- Advise on the long-term implications of switching between FEIE and FTC

- Ensure you’re claiming the maximum refund you’re legally entitled to

Final Thoughts: Peace of Mind for Expat Parents

The Child Tax Credit represents significant value for American families abroad, up to $2,200 per child with $1,700 potentially refundable. But accessing this benefit requires careful planning around how you structure your return.

The key takeaway: Your choice between the Foreign Earned Income Exclusion and Foreign Tax Credit doesn’t just affect your current-year taxes. It determines whether you can claim up to $1,700 per child as a direct refund. For families with multiple children in high-tax countries, this decision can mean thousands of dollars in additional refunds each year.

You don’t need to figure this out alone. Whether you’re filing for the first time as an expat parent, considering switching from FEIE to FTC, or wondering if you missed claiming credits in previous years, Greenback is here to help.

Ready to claim what you’re owed and file with confidence? If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on US expat taxes or working with Greenback, contact our Customer Champions.

Ready to claim every credit you’re entitled to?

The information provided in this article is for general guidance only and should not be considered legal or tax advice. Tax laws change frequently, and individual circumstances vary. Always consult with a qualified tax professional before making decisions about your tax situation.

Related Resources

Essential Reading for Expat Parents

- Foreign Earned Income Exclusion: Complete Guide for 2026

- Foreign Tax Credit Guide for U.S. Expats

- FEIE vs. FTC: Which Tax Strategy Saves You More Money?

- Form 2555 Instructions: Filing for the Foreign Earned Income Exclusion

- Form 8812: How Expats Claim the Child Tax Credit

- Form 1040 for U.S. Expats: Complete Filing Guide

- Schedule 8812: Credits for Qualifying Children and Other Dependents

- Amended Tax Returns: How to Claim Missed Credits

- Streamlined Filing Procedures: Catching Up on Late Returns

- U.S. Expat Tax Deadlines and Extensions

Frequently Asked Questions

Can I claim the Child Tax Credit if my spouse isn’t a U.S. citizen?

Yes, as long as at least one spouse has a valid Social Security Number and you file a joint return. Your spouse does not need to be a U.S. citizen. If your spouse doesn’t have an SSN, they’ll need to obtain an ITIN (Individual Taxpayer Identification Number) before you can file jointly.

What if my child doesn’t have a Social Security Number yet?

You cannot claim the Child Tax Credit until your child has a valid SSN. However, you may qualify for the Credit for Other Dependents ($500) if your child has an ITIN instead. Start the SSN application process as early as possible through your local U.S. embassy or consulate.

Do temporary absences affect the “lived with you” requirement?

No. Temporary absences for school, medical care, vacation, or military service count as time lived with you. This is particularly relevant for expat families whose children attend boarding school or return to the U.S. for summer programs.

Can divorced or separated parents both claim the Child Tax Credit?

No. Only one parent can claim the Child Tax Credit for each child per year. Generally, the custodial parent (the one the child lived with for more than half the year) claims the credit. However, the custodial parent can allow the noncustodial parent to claim the credit by providing a signed Form 8332 (Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent).

What if I became an expat mid-year?

You can still claim the full Child Tax Credit as long as your child lived with you for more than half the year and meets all other requirements. Your tax home location doesn’t affect the credit amount, though it affects which forms you file (Form 2555 for FEIE, potentially prorated for partial-year qualification).

Does the Child Tax Credit affect my FBAR filing?

No. The Child Tax Credit is unrelated to your FBAR (Foreign Bank Account Report) filing requirement. You must still file FinCEN Form 114 if your foreign accounts exceed $10,000 at any point during the year, regardless of any tax credits you claim.

Can I claim the Child Tax Credit for my stepchild or adopted child?

Yes. Stepchildren and legally adopted children are qualifying children for the Child Tax Credit as long as they meet all other requirements (age, residency, SSN, etc.). Foster children also qualify if placed with you by an authorized placement agency or by court order.

What happens to the Child Tax Credit after my child turns 17?

Once your child turns 17, they no longer qualify for the Child Tax Credit. However, they may qualify for the Credit for Other Dependents ($500) if they’re still your dependent. This credit has different rules and is nonrefundable.

Can I claim the Child Tax Credit if my child was born late in the year?

Yes. Your child only needs to be under age 17 on December 31 of the tax year. A child born anytime during 2025 qualifies for the full credit on your 2025 return, provided they have an SSN by the filing deadline.

What if I’m behind on filing previous years’ returns?

If you haven’t filed U.S. tax returns for previous years, you may qualify for the IRS Streamlined Filing Procedures. This program allows you to catch up on late returns with reduced penalties. You can claim the Child Tax Credit for those years when you file the late returns, as long as you file within the statute of limitations (generally three years from the original due date).

Can I e-file my return with the Child Tax Credit?

Yes. Most expat tax situations, including those claiming the Child Tax Credit, can be e-filed. E-filing is faster, more secure, and you’ll receive your refund quicker (typically within 21 days if claiming the refundable portion).