How to Claim the Foreign Earned Income Exclusion in 2025

- What Is the FEIE—and Why It Matters in 2025

- How to Qualify: Two Tests, One Goal

- Understanding Foreign Earned Income

- FEIE Limits: How Much Can You Exclude?

- Filing Requirements: Claiming FEIE on Form 2555

- Prorating the FEIE: Mid-Year Moves and Partial Qualification

- Missed the 330-Day Mark by April? Use Form 2350

- Bonus Tax Savings: Housing Exclusion and Foreign Tax Credit

- Common FEIE Mistakes That Cost You

- Special Considerations

- Who Should Consider the FEIE in 2025?

- Take Action Now

- Let Greenback Help You Maximize the FEIE

- Have questions about the FEIE or your specific expat tax situation?

If you’re working abroad in 2025, the Foreign Earned Income Exclusion (FEIE) could reduce your U.S. tax bill by thousands of dollars—or eliminate it altogether.

To claim the FEIE in 2025: File Form 2555 with your tax return, qualify under either the Physical Presence Test (330 days abroad) or Bona Fide Residence Test (full-year foreign resident), and exclude up to $130,000 in foreign-earned income from US taxation. Married couples who both qualify can exclude up to $260,000.

To maximize your savings: Combine the FEIE strategically with the Foreign Tax Credit on different income types, claim the Foreign Housing Exclusion for expensive cities, and ensure you meet all qualification requirements to avoid costly mistakes.

This guide shows you exactly how to claim the FEIE, avoid common mistakes, and maximize your savings.

What Is the FEIE—and Why It Matters in 2025

U.S. citizens are taxed on their worldwide income, even when they live abroad.

The FEIE is a tax benefit that helps expats avoid double taxation. If you qualify, you can exclude much of your foreign income from your U.S. return.

2025 FEIE Limit

The maximum exclusion is $130,000 for tax year 2025 (filed in 2026), up from $126,500 for tax year 2024 (filed in 2025).

For example, if you earn $150,000 in 2025 while living overseas and qualify for the FEIE, you’ll only be taxed on $20,000.

You can claim the Foreign Earned Income Exclusion if you meet these three requirements:

- You have foreign-earned income

- Your tax home is in a foreign country

- Pass one of two tests:

- Physical Presence Test (330 full days abroad in a 12-month period)

- Bona Fide Residence Test (full calendar year + intent to stay abroad)

Let’s break down exactly what each of these means.

How to Qualify: Two Tests, One Goal

You need to pass one of two tests to claim the FEIE. Choose the one that fits your situation.

1. The Physical Presence Test

This test is straightforward: You must be physically present in foreign countries for at least 330 full days during any 12-month period.

Key points:

- The 330 days don’t need to be consecutive

- The 12-month period can start any day (not just January 1)

- Brief US trips are allowed (watch that day count!)

- International waters and flight time don’t count

Perfect for: Digital nomads, short-term assignments, or if you’re new to living abroad.

Example: Sarah moved to Spain on March 15, 2024. By March 14, 2025, she spent 340 days abroad with two short trips home. She qualifies!

2. The Bona Fide Residence Test

This test looks at your intent to live abroad permanently, not just your physical presence.

You’ll need to show:

- You’re a bona fide resident of a foreign country for an entire tax year

- You’ve established a permanent home abroad

- You have no immediate plans to return to the US

Evidence includes:

- Long-term lease or home ownership

- Local bank accounts and credit cards

- Foreign driver’s license

- Kids enrolled in local schools

- Integration into the community

Perfect for: Permanent expats who’ve truly made another country home.

Which Test Should You Use?

Often, your situation chooses for you:

- New to living abroad? You’ll likely need the Physical Presence Test first

- On a defined assignment (1-2 years)? Physical Presence Test

- Moved abroad indefinitely? Bona Fide Residence Test may work better

- Country-hopping nomad? Physical Presence Test is your friend

Understanding Foreign Earned Income

Not all income qualifies for the FEIE. Here’s what counts and what doesn’t:

What Qualifies as Foreign-Earned Income

- Wages and salaries from working abroad

- Professional fees for services performed overseas

- Self-employment income earned in foreign countries

- Bonuses and commissions for foreign work

What Doesn’t Qualify

- Investment income (dividends, interest, capital gains)

- Rental income

- Pension or retirement distributions

- Social Security benefits

- US government employee wages

- Income earned in international waters or airspace

It doesn’t matter who pays you. Working for a US company while living in France? That income is foreign-earned. Working remotely from Miami Beach for a German company? That’s US income and doesn’t qualify.

FEIE Limits: How Much Can You Exclude?

The FEIE amount increases annually for inflation:

| Tax Year | Filed In | Maximum Exclusion |

| 2025 | 2026 | $130,000 |

| 2024 | 2025 | $126,500 |

| 2023 | 2024 | $120,000 |

Married couples alert: If both spouses qualify, each can claim their own FEIE. That’s up to $260,000 in excluded income for 2025!

Prorating Your Exclusion

Moved abroad mid-year? You’ll need to prorate your exclusion:

Formula: (FEIE Limit) × (Qualifying Days Abroad ÷ Days in Year) = Your Maximum Exclusion

Example: Tom moved to Japan on May 1, 2024. He has 245 qualifying days in 2024. $126,500 × (245 ÷ 365) = $84,897 maximum exclusion for 2024

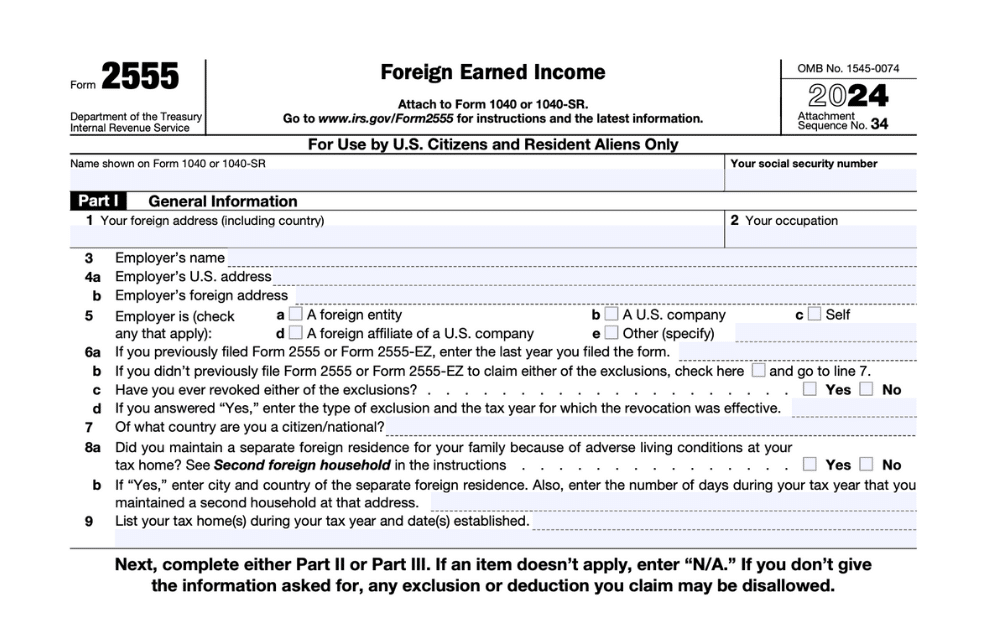

Filing Requirements: Claiming FEIE on Form 2555

To claim the FEIE, attach Form 2555 to your U.S. tax return (Form 1040).

You’ll need:

- Dates of all international travel

- Documentation of foreign income

- Proof of qualifying under your chosen test

- Previous year’s Form 2555 (if applicable)

Filing Tips

- File electronically if possible—it speeds up processing

- Double-check your qualifying test period (especially if you moved mid-year)

Keep meticulous records! Track every day abroad, save boarding passes, and document your foreign ties. The IRS may ask for proof.

Prorating the FEIE: Mid-Year Moves and Partial Qualification

If you qualify for only part of 2025, you can still claim the FEIE—but you’ll need to prorate it.

Example: Tom moved to Japan on May 1, 2025. He qualified under the Physical Presence Test by April 30, 2026, and spent 245 days abroad in 2025.

Calculation: $130,000 × (245 ÷ 365) = $87,260 FEIE limit for 2025

Missed the 330-Day Mark by April? Use Form 2350

If you’re still working toward 330 full days abroad, file Form 2350 to request an extension.

Key Deadlines

- April 15, 2026: Regular tax deadline

- June 15, 2026: Automatic extension for expats

- Before June 15: Submit Form 2350 to delay filing until you qualify

Bonus Tax Savings: Housing Exclusion and Foreign Tax Credit

Many expats can reduce their taxes even further with these:

Foreign Housing Exclusion/Deduction (on Form 2555)

Exclude additional amounts for qualifying housing expenses:

- Rent and utilities (except TV/internet)

- Property insurance

- Rental furniture

- Repairs and maintenance

The base amount is 16% of the FEIE ($20,800 for 2025), with higher limits for expensive cities.

Foreign Tax Credit vs. FEIE

If you’re paying higher foreign taxes, this credit may offer a better deal than the FEIE, especially on passive income.

Many expats combine the FEIE with the Foreign Tax Credit to maximize savings, especially when paying taxes to high-tax countries like Germany or France. But you can’t double dip on the same income if you choose to use both FEIE and Foreign Tax Credit—combining them strategically on different income types maximizes your tax savings.

Common FEIE Mistakes That Cost You

- Not filing a tax return at all (even if you owe $0)

- Forgetting to prorate if you moved mid-year

- Claiming FEIE and FTC on the same income

- Missing the 5-year revocation rule (if you stop using the FEIE)

- Poor travel documentation—track every day abroad

1. “I Don’t Need to File If I’m Under the Limit”

Wrong! You must file a US tax return and Form 2555 to claim the exclusion. No filing = no FEIE.

2. Forgetting to Prorate

Moved abroad July 1? You can’t claim the full $130,000. Calculate carefully or leave money on the table.

3. Missing the Revocation Trap

Once you claim the FEIE, you’re locked in for five years if you revoke it. Changing tax strategies requires careful planning.

4. Losing Other Tax Benefits

The FEIE can affect:

- IRA contribution eligibility

- Child Tax Credit refundability

- Other tax credits and deductions

5. Poor Record Keeping

“I think I was abroad 330 days” won’t cut it. Document everything!

Special Considerations

Digital Nomads

Country-hopping? The FEIE can work brilliantly:

- Use the Physical Presence Test

- Avoid establishing tax residency anywhere

- Keep careful day counts

- Consider “slow travel” to simplify tracking

Self-Employed Expats

Good news: Your business income qualifies! But remember:

- You’ll still owe self-employment tax (unless a totalization agreement applies)

- Consider the Foreign Housing Deduction

- Business expenses remain deductible

Late Filers

Behind on taxes? Don’t panic. The Streamlined Filing Procedures offer penalty-free catch-up options. But move fast—if the IRS contacts you first, this door closes.

Who Should Consider the FEIE in 2025?

- Remote workers living overseas

- Digital nomads bouncing between countries

- Families on foreign assignments

- Self-employed expats (though you’ll still owe SE tax)

If your income is earned from foreign work and you’re abroad most of the year, the FEIE could be your biggest tax break.

Take Action Now

Already Living Abroad?

- Confirm your qualifying test (Physical Presence or Bona Fide)

- Track days and gather documentation

- Prepare Form 2555 or hire a professional

Still Working Toward Qualification?

- Consider filing Form 2350 for extra time

- Review your calendar and plan for the 330-day requirement

Behind on Filing?

- Explore the Streamlined Filing Procedures—a penalty-free way to catch up on prior years

Let Greenback Help You Maximize the FEIE

At Greenback, we specialize in helping Americans abroad file taxes accurately and save money.

Greenback is an American company founded in 2009 by US expats for expats. We focused exclusively on expat taxes and always have. Many of our CPAs and Enrolled Agents are expats themselves, and because they live in 14 time zones, they experience firsthand the challenges of living abroad. They have the knowledge and patience to help you navigate the complicated U.S. tax system and your local rules.

We’ll help you:

- Choose the best strategy (FEIE, FTC, or both)

- Prepare and file Form 2555

- Avoid common pitfalls and IRS red flags

Have questions about the FEIE or your specific expat tax situation?

Contact us, and one of our Customer Champions will be happy to help. If you need very specific advice on your unique tax situation, you can also get a consultation with one of our expat tax experts.

Start your 2025 expat return with confidence. Get started with Greenback today.

Disclaimer: This article is for informational purposes only and does not constitute tax advice. Tax laws are complex and subject to change. Always consult with a qualified tax professional regarding your specific situation.