Form 1040-NR: Tax Filing Guide for Nonresident Aliens

- Who Must File Form 1040-NR?

- What Income Do I Report on Form 1040-NR?

- Tax Treaties: Reducing or Eliminating U.S. Tax

- Filing Deadlines for Form 1040-NR

- Deductions and Credits Available on Form 1040-NR

- Do I Need an ITIN to File Form 1040-NR?

- Special Situations for Form 1040-NR Filers

- Common Mistakes When Filing Form 1040-NR

- How to File Form 1040-NR

- Where to File Form 1040-NR

- Get Expert Help with Form 1040-NR

- Related Resources

Each year, thousands of nonresident aliens working in the United States have taxes automatically withheld at a flat 30% rate from their U.S.-source income. What many don’t realize is that filing Form 1040-NR can result in substantial refunds by claiming proper deductions, credits, or tax treaty benefits that reduce their actual tax liability.

Form 1040-NR (U.S. Nonresident Alien Income Tax Return) is the tax form specifically designed for individuals who are not U.S. citizens, don’t hold green cards, and don’t meet the substantial presence test. Understanding whether you need to file Form 1040-NR rather than the standard Form 1040 is crucial, as filing the wrong form can lead to overpaying taxes or incurring IRS penalties.

Here’s everything nonresident aliens need to know about Form 1040-NR for the 2026 filing season.

Key Takeaways

- Form 1040-NR is required for nonresident aliens with U.S.-source income or those engaged in U.S. trade or business.

- You only report U.S.-source income on Form 1040-NR, not worldwide income.

- Tax treaties with over 60 countries can reduce or eliminate U.S. tax on certain income types.

- Filing deadlines are April 15, 2026 (if wages are subject to withholding) or June 15, 2026 (if no withholding).

- Most nonresident aliens cannot claim the standard deduction, but they may be eligible for business expense deductions and certain credits.

Who Must File Form 1040-NR?

Not sure if you need to file Form 1040-NR or the standard Form 1040? We have a detailed comparison guide that breaks down the differences based on your residency status.

You must file Form 1040-NR if you’re a nonresident alien and:

Engaged in U.S. Trade or Business: You conducted business in the United States during the tax year, regardless of whether you had any income from that business. This applies even if your business resulted in a loss.

U.S.-Source Income Not Fully Taxed at Source: You have U.S.-source income on which tax wasn’t fully withheld. Common examples include:

- Wages from U.S. employment

- Rental income from U.S. real estate

- Dividends or interest from U.S. investments

- Capital gains from the sale of U.S. property

- Business income from U.S. operations

Claiming Refunds, Deductions, or Credits: You want to claim a refund of taxes that were over-withheld, or you want to claim deductions or credits available to nonresident aliens. Many nonresident aliens overpay U.S. taxes and are entitled to refunds, but never file to claim them.

Who Qualifies as a Nonresident Alien?

You’re a nonresident alien if you’re not a U.S. citizen and don’t meet either:

- Green Card Test: You’re a lawful permanent resident at any time during the tax year

- Substantial Presence Test: You’re physically present in the U.S. for 183 days or more using the three-year weighted formula

For a complete explanation of these tests and how to calculate them, see our guide on resident alien vs. nonresident alien status.

See If You Need to File Form 1040-NR

What Income Do I Report on Form 1040-NR?

The key difference between Form 1040-NR and Form 1040 is that nonresident aliens only report U.S.-source income. Your foreign income earned outside the United States is not reportable or taxable on your U.S. return.

Types of U.S.-Source Income

Effectively Connected Income (ECI): Income from actively conducting business in the United States is taxed at graduated rates (10% to 37%), the same rates that apply to U.S. citizens. This includes:

- Wages from U.S. employment

- Business profits from U.S. operations

- Rental income from U.S. real estate (if you elect to treat it as ECI)

Fixed, Determinable, Annual, or Periodical Income (FDAP): Passive investment income is generally taxed at a flat 30% rate (or lower treaty rate):

- Dividends from U.S. corporations

- Interest from U.S. payers

- Royalties

- Certain gambling winnings

The distinction between ECI and FDAP matters significantly because it determines your tax rate and what deductions you can claim.

Tax Treaties: Reducing or Eliminating U.S. Tax

The United States has income tax treaties with over 60 countries that can significantly reduce or eliminate U.S. tax on certain types of income for nonresident aliens. These treaties exist precisely to prevent double taxation.

Common Treaty Benefits

Tax treaties may provide:

- Reduced withholding rates on dividends, interest, and royalties (often 15% or even 0% instead of the standard 30%)

- Exemptions for certain income types, such as pensions, Social Security payments, or student scholarships

- Special provisions for students, teachers, and researchers that exempt compensation from taxation

- Reduced or eliminated tax on business profits unless you have a permanent establishment in the U.S.

How to Claim Treaty Benefits

To claim tax treaty benefits, you must:

- File Form 8833 if you’re claiming treaty benefits that override or modify U.S. tax law provisions

- Attach supporting documentation explaining which treaty article applies

- Report the nature and amount of exempt income on your Form 1040-NR

Learn more about claiming tax treaty benefits with Form 8833.

Treaty Countries

Check the IRS’s complete list of U.S. tax treaty countries to see if your home country has a treaty with the United States.

Filing Deadlines for Form 1040-NR

Your Form 1040-NR filing deadline depends on whether you have wages subject to U.S. withholding:

If You Have Wages Subject to Withholding

April 15, 2026 – Same deadline as U.S. citizens and residents

This applies if:

- You’re an employee receiving wages with U.S. income tax withholding

- You have an office or place of business in the United States

If You Don’t Have Withholding

June 15, 2026 – Automatic two-month extension

This applies if:

- You’re not an employee receiving wages

- You don’t have an office or place of business in the United States

- You’re self-employed without U.S. withholding

Extension to October 15, 2026

If you need more time, you can request an extension to October 15, 2026, by filing Form 4868 by your original deadline.

Extensions give you more time to file, not more time to pay. Any taxes owed are still due by April 15, 2026 (or June 15 if you qualify for the automatic extension).

Deductions and Credits Available on Form 1040-NR

As a nonresident alien, your access to deductions and credits is more limited than U.S. residents, but some important benefits remain available.

What You CAN Claim

Business Expense Deductions: If you’re engaged in a U.S. trade or business, you can deduct ordinary and necessary business expenses against your effectively connected income:

- Travel expenses

- Office supplies and equipment

- Professional fees

- Home office deduction (if you qualify)

- Depreciation on business assets

Itemized Deductions (Limited): Nonresident aliens who elect to itemize can claim:

- State and local income taxes

- Casualty and theft losses

- Charitable contributions to U.S. organizations

- Miscellaneous deductions related to U.S.-source income

Certain Tax Credits

- Child and dependent care credit (if you meet specific requirements)

- Education credits (for U.S. students on certain visas with proper elections)

What You CANNOT Claim

Standard Deduction: Most nonresident aliens cannot claim the standard deduction. The major exceptions are:

- Students and business apprentices from India under the U.S.-India tax treaty

- Students from certain countries (Barbados, Jamaica) who make specific elections

Many Common Credits

- Earned Income Tax Credit (EITC)

- Premium Tax Credit for health insurance

- Most other refundable credits are available to residents

For more details about available deductions, see our guide on U.S. expat tax deductions and credits.

Get Guidance for Your Nonresident Tax Situation

Do I Need an ITIN to File Form 1040-NR?

If you don’t have a Social Security Number (SSN) and aren’t eligible to get one, you’ll need an Individual Taxpayer Identification Number (ITIN) to file Form 1040-NR.

How to Get an ITIN

Apply for an ITIN by submitting Form W-7 along with your tax return and required documentation. You have three options:

- Mail original documents to the IRS (passport will be returned within 60-90 days)

- Visit a Taxpayer Assistance Center for in-person verification

- Work with a Certified Acceptance Agent who can verify your documents without you mailing your passport

Learn more about ITIN application costs and procedures.

Special Situations for Form 1040-NR Filers

Dual-Status Tax Years

If you change from nonresident to resident alien status (or vice versa) during the tax year, you’ll file as a dual-status alien. This typically happens when:

- You arrive in the U.S. and receive a green card mid-year

- You meet the substantial presence test partway through the year

- You depart the U.S. and lose resident status

For dual-status filing, you’ll need to file both Form 1040 and Form 1040-NR for different parts of the year. See our complete guide on filing as a dual-status alien.

Students and Scholars on F, J, M, or Q Visas

If you’re in the U.S. on a student or exchange visitor visa, you’re considered an “exempt individual” for the substantial presence test, meaning your days don’t count toward U.S. residency for tax purposes.

- First five years for students on F, J, M, or Q visas: You remain a nonresident alien and file Form 1040-NR even if physically present for more than 183 days.

- First two years for teachers and researchers on J or Q visas: Same treatment as students.

You must file Form 8843 annually to document your exempt status, even if you have no income and aren’t required to file a tax return.

H-1B Visa Holders

Unlike students, H-1B visa holders are not exempt individuals. Your days count immediately toward the substantial presence test from day one. If you’ve been in the U.S. on an H-1B for more than part of a year, you likely meet the test and should file Form 1040, not Form 1040-NR.

See our dedicated guide on H-1B tax filing requirements.

Nonresident Spouse Elections

If you’re a nonresident alien married to a U.S. citizen or resident alien, you can elect to be treated as a resident alien for tax purposes. This allows you to file jointly and claim the standard deduction.

To make this election:

- Both spouses must agree to report worldwide income

- You must obtain an ITIN for your foreign spouse

- File Form 1040 (not Form 1040-NR) with a statement of election

This election can result in significant tax savings, but it also means worldwide income reporting. Calculate both scenarios before deciding.

Departing the United States

If you’re leaving the U.S. after an extended stay, you may need to file Form 1040-C (Departing Alien Income Tax Return) before you leave. This is separate from your annual Form 1040-NR and ensures you’ve settled all tax obligations before departing.

Common Mistakes When Filing Form 1040-NR

Filing the Wrong Form

The most costly mistake is filing Form 1040 when you should file Form 1040-NR (or vice versa). If you’re unsure about your residency status, use our Form 1040 vs. Form 1040-NR comparison guide.

Not Claiming Treaty Benefits

Many nonresident aliens overpay U.S. taxes by not claiming available tax treaty benefits. Review your home country’s treaty with the United States to ensure you’re not leaving money on the table.

Missing the Standard Deduction Limitation

Nonresident aliens who claim the standard deduction when they don’t qualify face IRS adjustments and potential penalties. Know which deductions you can and cannot claim.

Not Filing When Required

Some nonresident aliens assume they don’t need to file because taxes were withheld. However, filing is required if you’re engaged in U.S. trade or business, and filing often results in refunds of over-withheld taxes.

Forgetting Form 8843

Students and scholars who fail to file Form 8843 documenting their exempt status can lose their exemption from the substantial presence test and face unexpected tax liabilities.

How to File Form 1040-NR

Filing Form 1040-NR requires careful attention to your income sources and residency status. Here’s a step-by-step guide to completing the form correctly.

Step 1: Gather Your Documents

Before you begin, collect all necessary documentation:

- Income documents: W-2 forms, 1099 forms (1099-DIV, 1099-INT, 1099-MISC), K-1 statements from partnerships

- Proof of residency status: Passport, visa documentation, entry/exit records

- Tax treaty documentation: If claiming treaty benefits, research your home country’s treaty with the U.S.

- Deduction records: Receipts for business expenses, charitable contributions, state/local taxes paid

- ITIN documentation: If you need to apply for an ITIN, prepare Form W-7 and supporting documents

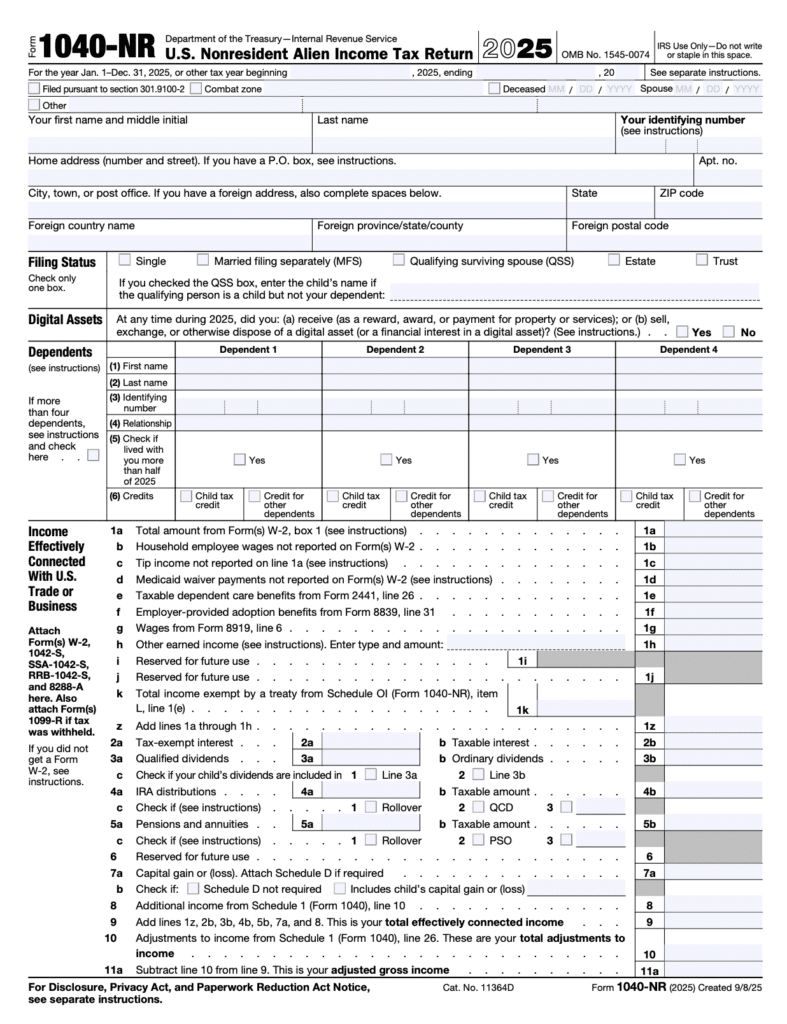

Step 2: Determine Your Filing Status

Form 1040-NR has limited filing status options:

- Single

- Married Filing Separately (most common for nonresident aliens)

- Qualifying Surviving Spouse (rare, only if you made the nonresident spouse election in a prior year)

Note: Nonresident aliens generally cannot file as “Married Filing Jointly” or “Head of Household” unless they make a special election to be treated as a resident.

Step 3: Report Your Income

Page 1 – Income Section:

Complete only the lines that apply to your U.S.-source income:

- Line 1a-1z: Wages, salaries, tips (from Form W-2)

- Line 2a-2b: Tax-exempt interest and taxable interest (from Form 1099-INT)

- Line 3a-3b: Qualified dividends and ordinary dividends (from Form 1099-DIV)

- Line 4a-4d: IRA distributions (if applicable)

- Line 5a-5d: Pensions and annuities (if applicable)

- Line 8: Other income (business income, rental income, royalties)

Only report income from U.S. sources. Do not report foreign income earned outside the United States.

Step 4: Calculate Deductions

Page 2 – Deductions Section:

Nonresident aliens typically use itemized deductions since most cannot claim the standard deduction.

- Schedule A (itemized deductions): Include state/local taxes, charitable contributions to U.S. organizations, and casualty losses

- Business expenses: If you have effectively connected income, complete Schedule C for business income and expenses

Calculate your total itemized deductions and enter on Line 12.

Step 5: Determine Your Tax Liability

Form 1040-NR calculates tax differently for:

- Effectively Connected Income (ECI): Taxed at graduated rates (10% to 37%). Use the tax tables in the Form 1040-NR instructions.

- FDAP Income: Taxed at a flat 30% rate (or lower treaty rate). Report separately on page 4 of Form 1040-NR.

Step 6: Claim Credits

If you qualify for any tax credits (such as the child and dependent care credit), complete the appropriate forms and schedules:

- Form 2441 for child and dependent care credit

- Form 8863 for education credits (if eligible)

Enter total credits on Line 20.

Step 7: Calculate Payment or Refund

Subtract your total tax from payments and credits:

- Line 25: Federal income tax withheld (from W-2 and 1099 forms)

- Line 31: Total payments

- Line 37: Amount you owe (if tax exceeds payments)

- Line 38: Amount to be refunded (if payments exceed tax)

Step 8: Attach Required Forms and Schedules

Make sure to attach:

- All W-2 and 1099 forms

- Form 8833 if claiming tax treaty benefits

- Form 8843 if you’re a student or scholar documenting exempt status

- Schedule OI (Other Information) – required for all Form 1040-NR filers

- Form W-7 if applying for an ITIN (attach to front of return)

- Any other supporting schedules (Schedule A, Schedule C, etc.)

Step 9: Sign and Date

Both you and your spouse (if filing married filing separately with a resident spouse election) must sign and date the return. If someone prepared your return, they must also sign.

Step 10: File by the Deadline

Mail your completed Form 1040-NR to the appropriate IRS address by your filing deadline (April 15 or June 15, 2026).

Form 1040-NR cannot be e-filed. You must print and mail your return to the IRS.

Where to File Form 1040-NR

If you owe taxes or are enclosing a payment:

Department of the Treasury

Internal Revenue Service

Austin, TX 73301-0215 USA

If you’re claiming a refund or not enclosing payment:

Department of the Treasury

Internal Revenue Service

Austin, TX 73301-0215 USA

For the most current mailing addresses, check the Form 1040-NR instructions on the IRS website.

Get Expert Help with Form 1040-NR

Correctly filing Form 1040-NR requires understanding complex residency rules, tax treaty provisions, and income sourcing regulations. Making mistakes can result in overpaying taxes or facing IRS penalties.

Greenback specializes in helping foreign nationals navigate U.S. tax obligations, whether you’re a nonresident alien filing Form 1040-NR, a new resident alien transitioning to Form 1040, or dealing with dual-status tax years.

Our CPAs and Enrolled Agents understand the unique challenges nonresident aliens face and can help you:

- Determine your correct residency status

- Claim all available tax treaty benefits

- Calculate effectively connected income vs. FDAP income

- File Form 1040-NR accurately and on time

- Apply for ITINs through our Certified Acceptance Agent services

No matter how complex your U.S. tax situation may be, we can help. You’ll have peace of mind knowing that your taxes were done right.

If you’re ready to be matched with a Greenback accountant, click the Get Started button below. For general questions on US expat taxes or working with Greenback, contact our Customer Champions.

File Your Form 1040-NR With Confidence

This article provides general information about Form 1040-NR filing requirements for nonresident aliens as of the 2025 tax year (filed in 2026). Tax laws change frequently, and individual situations vary. This content should not be considered specific tax advice. Always consult with a qualified tax professional regarding your unique situation.

Related Resources

- Form 1040 vs. Form 1040-NR: Which Should I File?

- Resident Alien vs. Nonresident Alien Tax Differences

- Dual-Status Alien Filing Guide

- Form 8833: Claiming Tax Treaty Benefits

- ITIN Application Guide and Costs

- Filing Joint Taxes with a Foreign Spouse

- New Resident Alien Tax Guide

- Form 1040-C: Departing Alien Tax Return

- H-1B Tax Compliance Guide

- U.S. Taxes for Foreigners: Complete Guide