What Is Form 1065 and When Do Partnerships Need to File?

- What Is Form 1065?

- Does Every LLC Have to File Form 1065?

- Do I Need to File Form 1065 with No Income?

- Form 1065 vs Form 1040

- Partnership Income and Expat Tax Benefits

- Common Expat Partnership Situations

- Why Professional Partnership Filing Makes Sense

- Next Steps for Partnership Filing

- Related Resources

Form 1065 is an information return that partnerships file to report income, but partnerships themselves don’t pay federal income tax. Instead, all profits and losses pass through to individual partners via Schedule K-1. According to the IRS, every domestic partnership must file Form 1065 unless it has no income and no deductible expenses.

For Americans abroad, Form 1065 matters when you’re:

- Partner in a U.S. business while living overseas

- Operating a foreign partnership with U.S.-sourced income

- Member of a multi-member LLC taxed as a partnership

Do You Have a Partnership With U.S. Reporting Requirements?

Here’s what you need to know about Form 1065 and why partnership filing requires professional expertise.

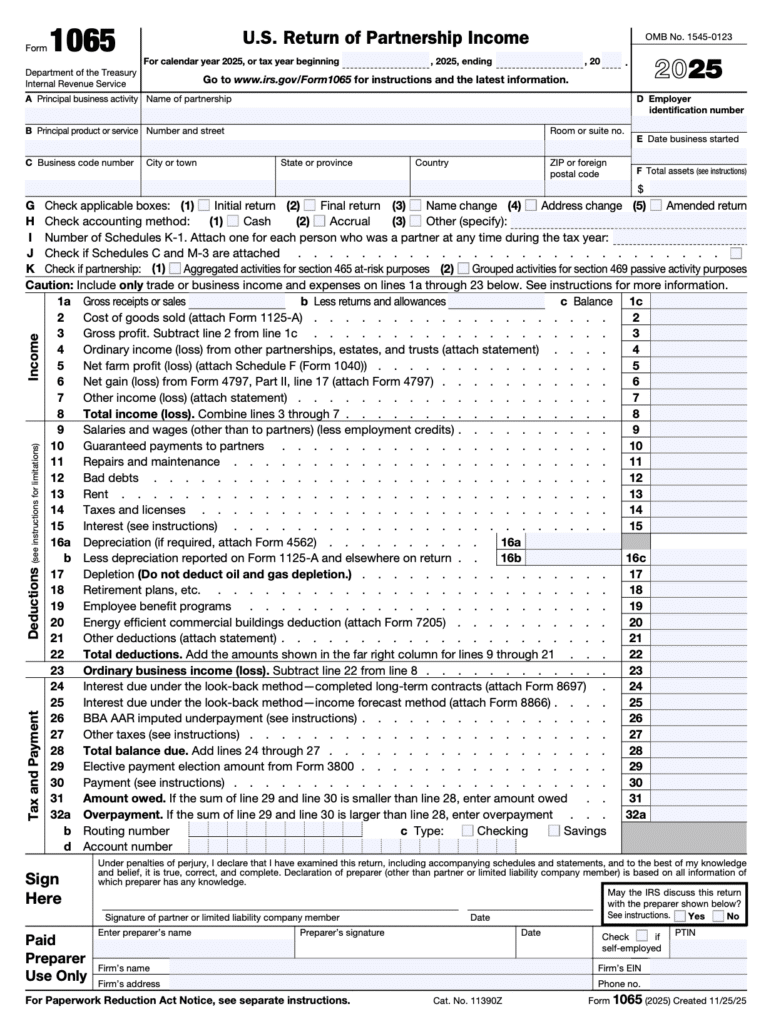

What Is Form 1065?

Form 1065 (U.S. Return of Partnership Income) reports income, gains, losses, deductions, and credits from partnership operations. The partnership files this return, but the entity itself doesn’t pay tax.

How it works: Partnership files Form 1065, prepares Schedule K-1 for each partner showing their share, and each partner reports K-1 income on their personal Form 1040. Partners pay tax individually based on their allocated share, even if they didn’t receive cash distributions.

Filing deadline: March 15, 2026, for calendar year 2025 partnerships (September 15 with extension).

Does Every LLC Have to File Form 1065?

Not every LLC files Form 1065. It depends on your LLC’s tax classification.

- Single-member LLCs: No Form 1065 required. Report income on Schedule C. If foreign, you may need Form 8858.

- Multi-member LLCs: Default to partnership taxation and must file Form 1065.

- Corporate elections: If you elect C corporation status (Form 8832), file Form 1120 instead. S corporation elections require Form 1120-S.

For expats, income from a single-member LLC on Schedule C may qualify for the Foreign Earned Income Exclusion. In a multi-member LLC, partnership income flows through a K-1, and different protections apply.

Do I Need to File Form 1065 with No Income?

According to the IRS, you can skip Form 1065 if your partnership had no income and no deductible expenses.

However, most partnerships have expenses: state fees, bank fees, professional services, insurance, or startup costs. Any deductible expense requires filing.

Penalty for not filing: $245 per month (maximum 12 months) × number of partners. A two-partner LLC faces potential penalties of $5,880.

Best practice: File Form 1065 annually, even with minimal activity, to maintain clear records and prevent IRS inquiries.

Form 1065 vs Form 1040

Form 1065 is the partnership’s information return. Form 1040 is your individual tax return, where you pay taxes on partnership income.

The process: Partnership files Form 1065 (due March 15), issues K-1s to partners, and partners report K-1 income on Form 1040 (due June 15 for expats with automatic extension, or October 15 with filed extension).

Your K-1 income integrates with other income on Form 1040, where you apply expat protections like the Foreign Earned Income Exclusion (up to $130,000 for 2025) or Foreign Tax Credit.

Partnership Income and Expat Tax Benefits

Partnership income is treated as active or passive income. The Foreign Earned Income Exclusion applies only to earned income from active participation, as reported on Form 2555. Investment income, rental income, and passive distributions typically don’t qualify.

The Foreign Tax Credit often works better for partnerships in high-tax countries. You claim dollar-for-dollar credits for foreign taxes paid using Form 1116.

Learn more about choosing strategies in our FEIE vs FTC comparison.

Common Expat Partnership Situations

U.S. partnership, expat partner: Partnership files Form 1065, you receive a K-1 and report income on your expat return. Some income may qualify for FEIE if you’re actively involved.

Foreign partnership, U.S. partner: May need to file Form 1065 if the partnership has U.S.-sourced income. You may also need Form 8865 to report foreign partnership interests.

Multi-country operations: Income sourcing rules become complex, requiring professional analysis for tax optimization.

Why Professional Partnership Filing Makes Sense

Partnership returns require expertise because of:

- Accurate K-1 preparation showing proper allocation of income, losses, deductions, and credits

- Income sourcing analysis determining U.S. vs foreign-source income

- Basis tracking for each partner’s capital account

- Foreign reporting coordination potentially requiring Forms 8865, 5471, or other international returns

- State filing requirements vary by location

For Americans abroad, professional filing ensures coordination between your partnership return and individual expat strategy. Greenback’s small business tax services include Form 1065 preparation, accurate K-1 generation, and coordination with your expat return.

If you’re starting a business overseas, we can help evaluate whether a partnership structure makes sense.

Next Steps for Partnership Filing

Form 1065 compliance while living abroad requires coordination between partnership and individual filing. Professional guidance ensures you navigate pass-through taxation, international sourcing rules, and expat protections correctly.

No matter how late, messy, or complex your partnership return may be, we can help. Greenback’s CPAs and Enrolled Agents have expertise in both partnership taxation and expat compliance.

If you’re ready to be matched with a Greenback accountant, get started today. For questions about partnership filing, contact our Customer Champions.

You’ll have peace of mind, knowing that your taxes were done right.

File Your Partnership Return the Right Way

This article is for informational purposes only and should not be considered tax advice. Tax laws change frequently, and individual circumstances vary. Please consult with a qualified tax professional for advice specific to your situation.

Related Resources

- Form 1040: What It Is and How to File Your U.S. Tax Return

- Foreign Earned Income Exclusion: How to Claim It in 2026

- Foreign Tax Credit: How to Reduce U.S. Taxes on Foreign Income

- Form 2555: How to Claim the Foreign Earned Income Exclusion

- Form 1116: How to Claim the Foreign Tax Credit

- Form 8865: Reporting Foreign Partnerships

- Form 8858: Reporting Foreign Disregarded Entities

- Small Business Tax Services for Americans Abroad

- Starting a Business Overseas: Tax Considerations

- FEIE vs FTC: Which Tax Benefit Should You Use?