IRS Streamlined Filing Procedures Explained: Catch Up Penalty-Free

- Who Qualifies for Streamlined Filing?

- What Is Considered Willful vs. Non-Willful Conduct?

- How Does Streamlined Filing Work? The Four-Step Process

- What Is the Difference Between SFOP and SDOP?

- What If I Owe Taxes from the Streamlined Period?

- What Forms Are Required for Streamlined Filing?

- What Happens After I Submit My Streamlined Filing?

- What If I Don't Qualify for Streamlined Filing?

- Why Time Matters with Streamlined Filing

- Get Back on Track with Greenback's Streamlined Filing Package

- Frequently Asked Questions About Streamlined Filing

- Related Resources

The IRS Streamlined Filing Compliance Procedures allow Americans abroad who are behind on their U.S. taxes to catch up by filing three years of tax returns and six years of FBARs with no penalties, provided the non-compliance was non-willful. For expats who have been living outside the U.S. for at least 330 days in one of the three most recent tax years, the Streamlined Foreign Offshore Procedures carry a 0% penalty. U.S. residents who use the domestic version pay a 5% miscellaneous offshore penalty.

According to the IRS, you must certify on Form 14653 that your failure to file was not willful (you didn’t intentionally avoid your obligations). You must also come forward before the IRS contacts you. The program requires:

- Three years of delinquent tax returns: the most recent years for which the filing deadline has passed

- Six years of delinquent FBARs: if you were required to file them

- Form 14653: certifying that your conduct was non-willful

- All required information returns: Form 8938, 3520, 5471, and others, if they apply

Here’s who qualifies for the streamlined procedures, what the process looks like, and how our Streamlined Filing Package handles every step.

Behind on your US taxes and feeling overwhelmed? Streamlined may be your solution.

Who Qualifies for Streamlined Filing?

To use the Streamlined Foreign Offshore Procedures, you need to meet three requirements:

Criteria 1: Non-Residency Requirement

You must have lived outside the United States for at least 330 full days during one of the last three tax years. This is the same physical presence test used for the Foreign Earned Income Exclusion, so many expats already meet this requirement naturally.

Criteria 2: Non-Willful Conduct

This applies when the failure to file or report occurred due to negligence, oversight, mistake, or a good-faith misunderstanding of the rules. The IRS defines “non-willful” as conduct that wasn’t intentional or reckless. If you genuinely didn’t know you needed to file U.S. taxes from abroad, or if you thought your employer’s tax withholding meant you were done with taxes, that’s typically non-willful.

Criteria 3: No IRS Contact

You can’t already be under audit or criminal investigation. The streamlined procedures are for taxpayers who come forward voluntarily before the IRS initiates contact. If you’ve received an audit notice, you’ll need to work with your examiner on alternative resolution options.

If you meet all three criteria, you can use this program regardless of how many years you’ve missed. Whether it’s been 5 years or 15 years since you last filed, streamlined filing covers everything.

What Is Considered Willful vs. Non-Willful Conduct?

The distinction between willful and non-willful failure matters because it determines your eligibility for penalty-free compliance. Most expats fall into the non-willful category, but it helps to see the difference clearly.

Non-Willful Conduct Includes:

- You moved abroad and genuinely believed you no longer had U.S. filing obligations

- You thought your employer withholding local taxes meant you were squared away

- You filed taxes, but didn’t know about FBAR requirements for foreign bank accounts

- Your tax preparer never asked about foreign accounts or income

- You inherited foreign accounts and didn’t realize they needed reporting

- You misunderstood which foreign accounts counted toward the $10,000 FBAR threshold

Willful Conduct Includes:

- You knew about the filing requirements but chose not to comply

- You deliberately hid foreign accounts or income from the IRS

- You filed tax returns, but intentionally left off foreign income

- You took active steps to conceal assets, such as using nominee accounts

- You checked “No” on Schedule B when asked about foreign accounts, knowing you had them

The IRS examines several factors when determining whether an individual is willful. Did you previously file U.S. tax returns but then stop? That raises questions. Did you answer “No” to the Schedule B question about foreign accounts when you had them? That’s a red flag. The key is whether you were aware of your obligations and chose to ignore them, or if you genuinely did not know about them.

If you’re uncertain about whether your situation qualifies as non-willful, a consultation with an expat tax professional can clarify your options before you submit anything to the IRS.

How Does Streamlined Filing Work? The Four-Step Process

The streamlined filing process is more manageable than most expats expect. Here’s exactly what you need to do:

Step 1: File Three Years of Tax Returns

You must prepare and file three years of delinquent or amended federal tax returns using Form 1040. These should be the most recent three tax years for which the filing deadline (including extensions) has passed.

For a 2026 submission, you would typically file returns for tax years 2023, 2024, and 2025. Each return must report all worldwide income, both foreign and domestic, and should include appropriate forms for claiming exclusions or credits:

- Form 2555 to claim the Foreign Earned Income Exclusion (up to $130,000 for the 2025 tax year)

- Form 1116 to claim the Foreign Tax Credit for taxes paid to foreign governments

- Form 8938 for foreign financial assets if you exceed FATCA thresholds

- Form 5471 if you own 10% or more of a foreign corporation

- Form 8621 for PFIC investments

- Any other required information returns

Each return should be marked at the top in red ink: “Streamlined Foreign Offshore.”

Step 2: File Six Years of FBARs

If you had $10,000 or more in combined foreign financial accounts at any time during any of the last six years, you must file six years of FBARs (FinCEN Form 114).

FBARs include more than just bank accounts. You must report:

- Foreign checking and savings accounts

- Foreign investment and brokerage accounts

- Foreign pension and retirement accounts

- Foreign life insurance policies with cash value

- Accounts where you have signatory authority, even if you don’t own them

FBARs must be filed electronically through FinCEN’s BSA E-Filing System, not through the IRS. If you’ve missed multiple years, you’ll file separate FBARs for each year, reporting the maximum values during each calendar year.

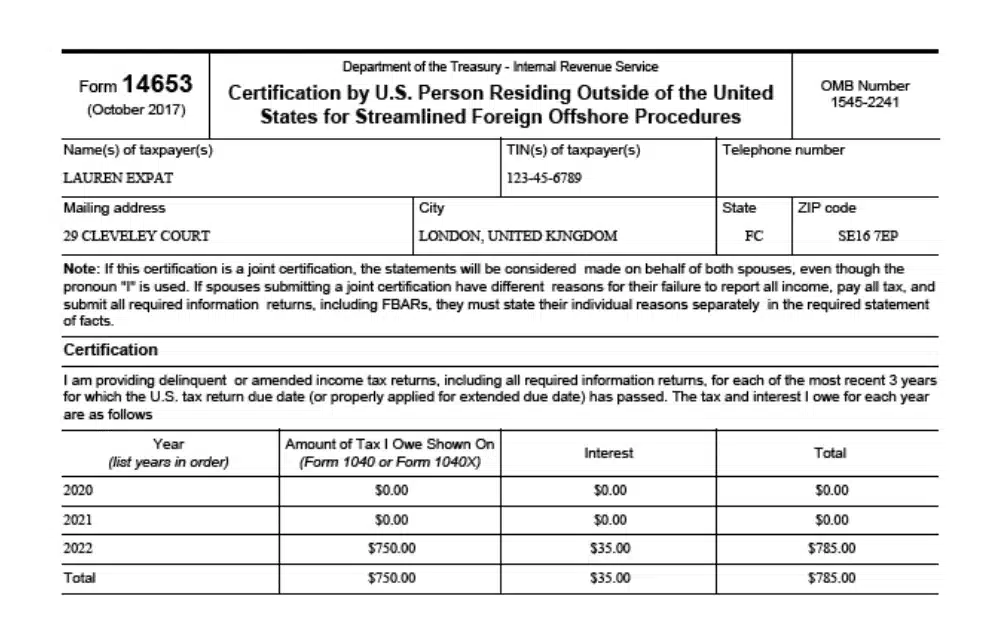

Step 3: Submit Certification of Non-Willfulness (Form 14653)

This is the most critical part of your streamlined submission. Form 14653 requires you to certify under penalties of perjury that your failure to file was non-willful.

The form asks you to provide a detailed narrative explaining:

- Why you didn’t file your tax returns or FBARs

- What you believed about your U.S. tax obligations

- Why your conduct was not willful

- Steps you took (if any) to understand your obligations

Be truthful and specific. The IRS reviews these certifications carefully. False or misleading statements can result in denial of streamlined treatment, potential criminal charges, and much harsher penalties.

Step 4: Pay Outstanding Taxes and Interest

While streamlined filing eliminates penalties, you still must pay any taxes you owe for the three years, plus interest calculated from the original due dates.

Here’s the reassurance: most expats don’t owe substantial amounts after applying the Foreign Earned Income Exclusion or Foreign Tax Credit. If you lived in a country with higher taxes than the U.S. and paid local taxes on your income, the Foreign Tax Credit often eliminates your U.S. tax liability entirely.

Interest rates are set by the IRS and compound daily; however, paying promptly when you file prevents additional interest from accruing.

What Is the Difference Between SFOP and SDOP?

| SFOP (Foreign Offshore) | SDOP (Domestic Offshore) | |

|---|---|---|

| Who qualifies | Expats who lived outside the U.S. for 330+ days in one of the last 3 tax years | U.S. residents who failed to report foreign accounts/income |

| Penalty | 0% | 5% of the highest aggregate value of unreported foreign financial assets |

| Certification form | Form 14653 | Form 14654 |

| Tax returns required | 3 most recent years | 3 most recent years |

| FBARs required | 6 most recent years | 6 most recent years |

What If I Owe Taxes from the Streamlined Period?

Don’t let potential tax liability stop you from coming into compliance. Here’s what typically happens:

Example 1: Digital Nomad with No Tax Home

Sarah lived in Thailand, Bali, and Portugal over the last three years, working remotely for various clients. She had no idea she needed to file U.S. taxes and never filed FBARs for her $45,000 in combined foreign accounts. Her annual total income was $95,000.

After working with a Greenback accountant, Sarah:

- Applied the Foreign Earned Income Exclusion to exclude $95,000 per year

- Owed $0 in federal income tax for all three years

- Still needed to pay self-employment tax on her freelance income (approximately $13,000 per year)

- Paid interest on the unpaid self-employment tax

- Avoided all late-filing and FBAR penalties through streamlined filing

Example 2: Corporate Expat in High-Tax Country

James worked for a multinational company in Germany for the last five years. He earned $180,000 annually and paid substantial German income taxes (approximately $60,000 per year). He filed German taxes but never realized he had U.S. tax obligations and needed to file U.S. returns.

After filing through streamlined procedures, James:

- Reported all income on his U.S. returns

- Claimed the Foreign Tax Credit for his German taxes paid

- Owed $0 in U.S. federal income tax for all three years

- Paid minimal interest (only because his refundable credits weren’t claimed earlier)

- Avoided all penalties

Example 3: Expat in Low-Tax Country with Investment Income

Maria lived in the UAE (which has no personal income tax) and earned $140,000 annually plus $25,000 in U.S.-source dividend income. She didn’t file for seven years.

After streamlined filing, Maria:

- Excluded $130,000 of her earned income using the Foreign Earned Income Exclusion

- Paid U.S. tax on the $10,000 of earned income above the exclusion threshold

- Paid U.S. tax on her $25,000 of U.S. source dividend income

- Owed approximately $4,500 per year in federal taxes

- Paid interest on these unpaid taxes

- Still saved tens of thousands in penalties by using streamlined filing

What Forms Are Required for Streamlined Filing?

Your streamlined submission package must include all required forms and documentation:

Core Tax Forms:

- Form 1040 for each of the three years (marked “Streamlined Foreign Offshore”)

- Form 2555 if claiming the Foreign Earned Income Exclusion

- Form 1116 if claiming the Foreign Tax Credit

- Schedule C if you had self-employment income

- Schedule SE for self-employment tax calculations

Foreign Asset Reporting:

- FinCEN Form 114 (FBAR) for six years if accounts exceeded $10,000

- Form 8938 if you meet FATCA thresholds (varies by filing status and location)

Business Entity Forms (if applicable):

- Form 5471 if you own 10% or more of a foreign corporation

- Form 8865 if you own a foreign partnership

- Form 8858 for disregarded foreign entities

- Form 3520 for foreign trusts, gifts, or inheritances over $100,000

- Form 8621 for PFIC investments

Certification:

- Form 14653 (Certification by U.S. Person Residing Outside of the United States)

Accuracy matters tremendously. Missing forms or incorrect information can trigger IRS inquiries, processing delays, or even denial of streamlined treatment.

What Happens After I Submit My Streamlined Filing?

After you submit your complete streamlined package (tax returns to the IRS, FBARs to FinCEN, and certification), the IRS begins processing your submission.

Processing Timeline: The IRS typically takes 3 to 6 months to process streamlined filings, though complex cases or high-volume periods can extend this timeframe. The IRS doesn’t send acknowledgment letters confirming receipt, so your submission confirmation is your only record of filing.

No Closing Agreement: Unlike other voluntary disclosure programs, streamlined filing doesn’t culminate in a closing agreement with the IRS. Your returns are simply processed like any other filing.

Potential for Audit: While streamlined submissions aren’t automatically flagged for audit, they can be selected for examination under the IRS’s normal audit selection processes. If your submission is accurate, complete, and truthful, audit risk is minimal. The IRS may verify information against data received from foreign banks through FATCA reporting.

What Counts as Completion: You’ve successfully completed streamlined filing when:

- All three tax returns have been processed

- All six FBARs have been filed with FinCEN

- Any taxes and interest owed have been paid

- No penalty assessments have been made for the streamlined period

What If I Don’t Qualify for Streamlined Filing?

If you don’t meet the eligibility requirements for streamlined filing, you still have options to become compliant:

1. Delinquent FBAR Submission Procedures

If you’re current on your tax returns but missed filing FBARs, you might qualify for the simpler Delinquent FBAR Submission Procedures. This program requires:

- All tax returns have been filed and are correct

- All income from foreign accounts was reported correctly and taxed

- Your failure to file FBARs was non-willful

If you qualify, file all missing FBARs and include a statement explaining your non-willful conduct. No penalties apply.

2. Voluntary Disclosure Program (VDP)

If your failure to file was willful, the Voluntary Disclosure Program provides a pathway to compliance while reducing the risk of criminal prosecution. The VDP involves:

- Higher penalties than streamlined filing

- Full disclosure of previously unreported income and assets

- Cooperation with the IRS examination

- No guarantee of criminal immunity, but reduced prosecution risk

3. Reasonable Cause Penalty Abatement

If you filed late tax returns within the last 1-2 years and have a good compliance history, you might request penalty relief based on reasonable cause. This requires demonstrating that you exercised ordinary care and prudence, but still failed to meet the requirements.

4. Standard Late Filing (Not Recommended Alone)

Simply filing past-due returns without using any IRS program is called a “quiet disclosure” and carries significant risk. The IRS views quiet disclosures as attempts to conceal past non-compliance. If the IRS discovers your late filing before you disclose it properly, you may face full FBAR penalties (up to $16,536 per form for non-willful violations, or $165,353 or 50% of account balances for willful violations) and possible criminal charges.

Why Time Matters with Streamlined Filing

The Streamlined Filing Compliance Procedures have been available since 2012, but the IRS has periodically discussed eliminating or modifying the program. If you’re eligible, don’t delay:

- The Program Could Change: The IRS has indicated that streamlined procedures could be modified or eliminated in future years. Once the program closes, penalty-free catch-up options become much more limited.

- Interest Keeps Growing: Every month you wait means additional interest accruing on any unpaid taxes. Interest compounds daily from the original due date.

- Foreign Bank Reporting Keeps Improving: With FATCA agreements in place with countries worldwide, foreign financial institutions report account information directly to the IRS. The IRS’s ability to identify non-filers continues to improve.

- Peace of Mind: Living with unfiled taxes creates constant stress. Every news story about IRS enforcement, every border crossing, every major financial decision carries that nagging worry. Streamlined filing ends that anxiety.

Get Back on Track with Greenback’s Streamlined Filing Package

Catching up on missed tax returns shouldn’t be overwhelming. Greenback Expat Tax Services has helped over 23,000 expats get current with U.S. tax compliance, including hundreds of successful streamlined filing submissions.

Our flat-fee Streamlined Filing Package ($1,750) includes:

- Preparation of three years of delinquent federal tax returns

- Filing of six years of FBARs (up to 5 accounts per form)

- Assistance with Form 14653 certification

- Expert guidance on maximizing exclusions and credits

- Direct access to a dedicated expat tax accountant

- Confidence that your filing is accurate and complete

For general questions about streamlined filing or working with Greenback, contact our Customer Champions. Ready to catch up on your expat taxes? Click the get started button below.

Catch up on your U.S. taxes without penalties

Frequently Asked Questions About Streamlined Filing

Yes. As of the IRS’s most recent update, the Streamlined Filing Compliance Procedures remain an active compliance option. The program has no announced end date, but the IRS can modify or discontinue it at any time. The One Big Beautiful Bill Act (OBBB) does not change the streamlined program itself, though it may affect tax calculations within your returns (such as higher standard deductions and updated FEIE amounts).

Streamlined submissions are not automatically audited. According to the IRS, returns filed under the program are processed like any other return and may be selected for audit through the standard audit selection process. In practice, well-prepared, good-faith filings with a complete and detailed Form 14653 certification are rarely flagged. However, the IRS does verify submissions against information received from banks, financial advisors, and other sources, so accuracy is critical.

Most expats owe far less than they expect. If your income was under $130,000 (2025 FEIE limit) and you lived in a foreign country, the Foreign Earned Income Exclusion can reduce your federal income tax to $0 for the covered years. If you lived in a high-tax country, the Foreign Tax Credit may eliminate your U.S. tax entirely. You will owe interest on any unpaid tax, but penalties are waived for expats abroad (0% penalty under SFOP). U.S. residents using the domestic version (SDOP) pay a 5% miscellaneous offshore penalty.

Non-willful means your failure to file was due to negligence, inadvertence, mistake, or a good-faith misunderstanding of the requirements. It was not intentional. Common non-willful explanations include: you didn’t know U.S. citizens must file taxes while living abroad, you thought your employer’s foreign tax withholding covered your U.S. obligations, you received incorrect advice from a tax professional, or you were unaware of FBAR requirements. You certify non-willfulness on Form 14653 (SFOP) or Form 14654 (SDOP) with a detailed narrative explaining your specific circumstances. Be honest, thorough, and specific.

Yes. You can retroactively claim the FEIE (up to $130,000 for 2025), the Foreign Tax Credit, and the Foreign Housing Exclusion on the returns you file through the streamlined program. This often reduces or eliminates the tax owed for the covered years, meaning many expats owe only interest (and sometimes nothing at all).

You file the three most recent tax years for which the filing deadline (including extensions) has passed. For a submission in 2026, this typically means tax years 2023, 2024, and 2025 (if the 2025 deadline has passed). For FBARs, you file the six most recent years, typically 2020 through 2025. The exact years depend on when you submit and whether you filed any extensions.

You only need to file three years of tax returns and six years of FBARs, even if you’ve been non-compliant for much longer. The IRS does not require you to go back further under the streamlined program. This is one of the most valuable aspects of the program: whether you’ve missed 5 years or 20 years, the filing requirement is the same.

Yes, but the filing becomes more complex. You’ll need to include the appropriate information returns (Form 5471 for foreign corporations, Form 3520/3520-A for foreign trusts, Form 8865 for foreign partnerships) for the covered years. Missing these forms carries penalties of $10,000+ per form, which the streamlined program can help avoid. Professional guidance is strongly recommended for these situations.

If the IRS concludes that your non-compliance was willful (intentional), your submission will be processed outside the streamlined program under standard examination procedures. This could result in full FBAR penalties (up to $16,536 per form for non-willful violations, or the greater of $165,353 or 50% of account balances for willful violations), accuracy-related penalties, and potentially a criminal investigation. If you have any concern that your conduct could be considered willful, consult a tax attorney before filing.

A quiet disclosure means filing past-due returns and FBARs without using a formal IRS program (like streamlined or voluntary disclosure). The IRS has specifically warned against this approach. Quiet disclosures can be viewed as attempts to avoid detection and may increase your risk of penalties, audits, or criminal investigations compared to a transparent, streamlined submission.

1. For SFOP (foreign): No. The IRS does not typically send a confirmation letter because no penalty is assessed. If you don’t hear anything within 6 to 12 months, that generally means your filing was processed without issue.

2. For SDOP (domestic): The IRS typically sends a confirmation letter after processing the 5% penalty payment.

In both cases, no news is good news. If the IRS needs additional information, it will contact you by mail.

There is no published deadline. The program has been available since 2014 (expanded from the 2012 version) and remains active. However, the IRS can modify or close the program at any time without advance notice. The most important deadline is personal: you must come forward before the IRS contacts you. Once the IRS initiates a civil examination or criminal investigation, you lose eligibility.

This article is for informational purposes only and does not constitute tax advice. Every expat’s situation is unique, and tax laws are subject to frequent changes. For advice tailored to your specific circumstances, consult a qualified tax professional specializing in international taxation.

Related Resources

- Form 14653: The Streamlined Certification Statement

- Delinquent FBAR Submission Procedures

- Voluntary Disclosure Program

- FBAR Penalties Explained

- FBAR Filing Requirements

- Filing Late U.S. Expat Taxes

- How We Help Late Filers

- Foreign Earned Income Exclusion

- Foreign Tax Credit Guide

- U.S. Expat Taxes: The Complete Guide

Featured In